This month’s edition kicks off with the news that Goldman Sachs has acquired Folio Institutional and its $11 billion RIA custody platform for 450 (mostly small) registered investment advisers, raising the question of whether Goldman is making a play to compete for small RIA custody opportunities as Morgan Stanley acquires E*Trade Advisor Services and Schwab acquires TD Ameritrade, or whether Goldman will repurpose Folio to capture large wirehouse breakaway teams, or simply use it as a custodial platform for its own RIAs (Ayco and United Capital), or turn it into a robo-adviser solution paired with Marcus, or use Folio’s fractional share trading capabilities to build a direct indexing solution. Or perhaps all of the above!?

From there, the latest highlights also include a number of other interesting adviser technology announcements, including:

Read the analysis about these announcements in this month’s column, and a discussion of more trends in adviser technology, with special AdviserTech consulting guests Craig Iskowitz and Kyle Van Pelt, covering news including Aurora Capital acquiring FMG Suite to build a “Hubspot for financial advisers” as interest grows in adviser digital marketing, Vise.ai launches a new robo-tech-turned-TAMP solution for advisers, Envestnet launches a next-generation client portal that includes not just performance reporting and news but also client to-dos, Fidelity rolls out a new Virtual AI assistant not for clients but to support adviser back-office servicing, and Morningstar doubles down on its bet on a more ESG-centric future by fully acquiring Sustainalytics (after buying an initial 40% stake back in 2017).

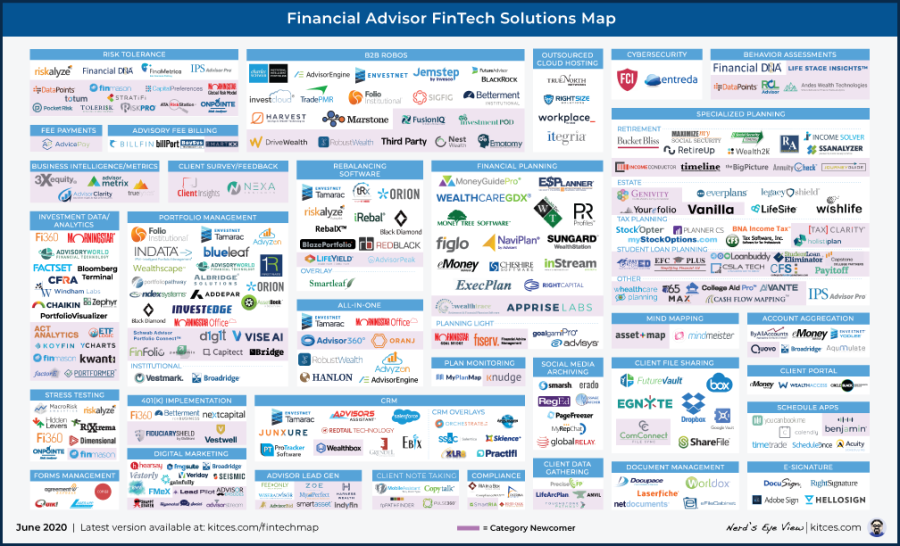

Be sure to read to the end, where we have provided an update to our popular new Financial Advisor FinTech Solutions Map!

I hope you’re continuing to find this column on financial adviser technology to be helpful! Please share your comments at the end and let me know what you think!

*And for #AdviserTech companies who want to submit their tech announcements for consideration in future issues, please submit to TechNews@kitces.com!

Goldman Sachs acquires Folio Institutional for so many potential reasons no one is actually sure which is why. The big industry news this month was the announcement that Goldman Sachs was acquiring brokerage and clearing (and RIA custodian) firm Folio Institutional for what was rumored to be $250 million, marking a cool $1 billion of total investments Goldman Sachs has made in wealth management in barely over a year since its $750 million acquisition of United Capital last year. As an RIA custodian, Folio was a relatively small ‘niche’ player with an estimated $11 billion of AUM across 450 RIAs, most of which were very small RIAs (with only 17 RIAs at >$100 million of AUM and the other 400+ still under the $100 million threshold). Initial speculation was that the Folio acquisition would position Goldman to expand the existing Folio RIA custody business and compete for small RIAs that may be looking for a new home as Schwab moves forward with its acquisition of TD Ameritrade. Yet the reality is that Goldman’s acquisition of United Capital last year was itself a $25 billion AUM platform, and Ayco was reportedly at nearly $35 billion of AUM last year as well, which means that if all Goldman did was use Folio’s platform to consolidate its existing AUM from its own wealth management businesses, it might multiply the assets on Folio more than 5X and earn a healthy return on investment simply by vertically integrating its own RIA custody and clearing business to earn the underlying economics! Alternatively, to the extent that Goldman Sachs is a known Wall Street brand, there is also speculation that Goldman might be looking to get into the RIA custody business not for small RIAs or its own existing RIA assets, but to compete for wirehouse breakaways that want to go independent but are still looking for Wall-Street-level private wealth management capabilities (from banking to international brokerage, alternative investments to IPOs and more), where Folio Institutional as a back-end and United Capital’s FinLifeCX as a front end could be a compelling offering coupled with the Goldman brand (especially since wirehouse brokers would perhaps be more likely to use Goldman’s products, allowing their RIA custody solution to also be a distribution channel for Goldman asset management products). At the same time, AdvisorHub reports that Goldman actually isn’t even placing Folio within its wealth management division, but instead its global markets division, where Goldman might leverage Folio’s retail business (e.g., Folio Investments and FolioFn) and its retail trading volume to fuel its own institutional trading desks. However, Goldman doesn’t only have to leverage retail trading for its institutional trading desk. The firm has also been increasingly pivoting toward retail investing as a business line unto itself, first with its Marcus banking solution and now there are indications that it plans to launch a robo-adviser next year, where Folio Institutional may become the infrastructure to power its down-market small-client solution (especially given that Folio was an early pioneer into fractional share trading, which is viewed as essential to facilitate small clients and especially new investors who don’t have the dollars to buy whole share units of high-flying stocks). And Folio’s fractional share trading capabilities also introduce the possibility that the real prize for Goldman is to compete with Schwab and others positioning for a future of direct indexing as the next big thing that will replace mutual funds and ETFs (for which the technology to manage fractional share trading is absolutely essential to ensure exact ownership of the underlying components of the index). All of which goes to show that Goldman has an incredible number of opportunities with Folio – from small RIAs to wirehouse breakaways to its own RIA assets to retail client assets to proprietary trading to the future of direct indexing. The only question is which one(s) are Goldman’s actual goal to pursue?

Franklin Templeton acquires AdvisorEngine’s robo onboarding, but is Junxure CRM back-office automation the real gem? The early success (and high-profile venture capital rounds) for early-stage robo-advisers like Betterment, Wealthfront and FutureAdvisor from 2012 to 2014 created a subsequent wave of robo-adviser competitors that quickly discovered the real reason financial advisers struggle to serve small clients isn’t the cost to onboard and service the clients but the acquisition cost to get them (especially at scale) in the first place. When coupled with the competing entrance of incumbents like Schwab’s Intelligent Portfolios and Vanguard’s Personal Advisor Services in 2015, many robo-advisers pivoted away from the prohibitively high-acquisition-cost direct-to-consumer channel to become B2B “robo-adviser-for-advisers” solutions instead, only to find that while advisory firms did have a pain point with onboarding, they largely expected their already “free” custodians to fix the problem by improving their technology, and weren’t necessarily willing to pay an additional cost themselves to solve the problem. Which led some, like Harvest (née Trizic), to pivot into “adjacent” channels like bank and trust companies (that were more willing to pay for onboarding tools that could link directly to their existing bank systems), others like Oranj to remove the pricing challenge by giving their software away for free in the hopes of monetizing their offering through model marketplaces where asset managers pay for distribution, while still others like AdvisorEngine (née Vanare|Nest Egg) tried to expand their feature set to become more holistic platforms to justify charging a middleware fee, acquiring Wealthminder for financial planning light software, Kredible for adviser marketing, and most notably Junxure for full-scale adviser CRM capabilities for an estimated $24 million. Except in practice, it appeared at the time that AdvisorEngine acquired Junxure not so much just to expand its CRM capabilities, but to obtain Junxure users that might be cross-sold the AdvisorEngine platform, going so far as to highlight in the acquisition not just Junxure’s user count (a typical software metric) but the AUM of the Junxure users (important for AdvisorEngine’s basis point model) — a problematic mismatch highlighted at the time, as AdvisorEngine was investment-centric software that lacked full-scale financial planning features (a cultural misfit for the disproportionately financial-planning-centric Junxure users). Now, two years later, it appears that the grand experiment of converting Junxure users into AdvisorEngine assets (and more generally, convincing advisers to pay basis points for technology) has failed, and WisdomTree is offloading AdvisorEngine (and Junxure) to Franklin Templeton for an unreported sum (but prior indications from WisdomTree that it anticipated an up-to-$30 million write-down on its $58 million stake suggests that AdvisorEngine may have been sold for little more than the value it paid for Junxure alone in the first place). The fact that AdvisorEngine was acquired by an asset manager isn’t entirely surprising and fits with the ongoing trend of asset managers acquiring robo-adviser-for-advisers platforms as a distribution channel, from BlackRock acquiring FutureAdvisor in 2015, to Invesco buying JemStep, Principal acquiring RobustWealth and of course, WisdomTree having previously acquiring AdvisorEngine itself. However, Franklin Templeton indicates that the AdvisorEngine deal may not just be about acquiring robo front-end tools (to support product distribution), but about the potential to offer a deeper back-end solution built primarily around Junxure, and following more in the footsteps of the recent FTV Capital acquisition of Docupace. Of course, in the end, Franklin Templeton is still in the asset management business and not the tech business — so ostensibly, at some point, the company still hopes to more deeply entrench itself and its brand with advisers for the potential of improving its own (recently waning) fund distribution. And to the extent that WisdomTree didn’t succeed with AdvisorEngine’s front-end tools to support distribution, it’s not clear that Franklin Templeton’s focus on back-end Junxure capabilities will be more effective at generating adviser engagement with Franklin’s funds. Nonetheless, the foray by an asset manager beyond just robo-adviser front-end technology and into the realm of financial adviser back-office efficiency software would represent a significant shift in both the focus of AdvisorEngine and the competitive forces of adviser CRM, though it’s still unclear whether Franklin Templeton has a clear vision, especially as an investment firm, to re-establish the waning market share of an especially financial-planning-centric adviser CRM.

TradingFront pursues small RIAs with Interactive Brokers partnership but is it really just an RIA custodial tech fee? One of the fundamental challenges of robo-advisers that pivoted to become ‘robo-advisers-for-advisers’ is that, while advisory firms have long needed and desired better onboarding technology for clients, in practice, most weren’t willing to pay for what they expected their broker-dealers or RIA custodial platforms to provide directly in the first place. And for those who were willing to pay for the technology, in practice, many just created their own tools instead, as RIA asset manager Alpha Architects did by rolling out its own robo tools in 2016 (not as a passive investment vehicle, but to facilitate the onboarding and trading of its active investment management strategies for its clients) on top of its Interactive Brokers RIA custodial platform. Yet the challenge is that it’s difficult for any one advisory firm to build (and then sustain the required continuous improvements to) technology entirely on its own, which ultimately led Alpha Architect to spin off its technology into a separate company – dubbed TradingFront – and make it available to other RIAs, and eventually sell the company itself in 2018 to UP Fintech (an online brokerage platform for Chinese investors also known as Tiger Brokers, which itself is backed by Interactive Brokers). And now, TradingFront has been repackaged into a full ‘front end’ for Interactive Brokers itself, which the company is positioning as an all-in-one platform for small to midsize RIAs that simply want a fully integrated RIA-custody-plus-tech platform that works out of the box. The core of the TradingFront platform is robo onboarding (including customizable risk tolerance questionnaires), plus performance reporting (with held-away account aggregation via Plaid), and rebalancing, and the associated adviser and client portals to manage them, also with a “very basic” CRM. TradingFront pricing is $100/month for the platform for up to either 100 accounts or $10 million of AUM, after which advisory firms can choose either $18/account/year (after the first 100) or 8 bps (after the first $10 million of AUM). Notably, though, TradingFront will also participate in some of the underlying economics of Interactive Brokers’ custody and clearing platform itself, such as commissions on trading (raising questions of whether RIAs using the platform will even be able to use Interactive Brokers’ recently announced zero-commission platform for RIAs). Still, though, for smaller to midsize RIAs that have historically had somewhat limited choices for RIA custody (especially for those firms with less than $10 million of AUM) and that don’t necessarily have the skillset or bandwidth to pull together their own tech stack one component at a time, some cost must be incurred for the advisory firm’s tech stack, and TradingFront’s $18/account cost structure for performance reporting, rebalancing and onboarding tools is still drastically lower than competitors like Orion, Black Diamond and Tamarac (even with a smaller layer of RIA custodian transaction costs for client trades). On the other hand, with competing RIA custodians also building their own on-platform tools — from Fidelity’s Wealthscape to Schwab’s PortfolioConnect and TD Ameritrade’s popular iRebal — often already available for free, it’s not entirely clear which RIAs would necessarily be interested in paying up for the TradingFront/Interactive Brokers all-in-one solution, especially since most RIAs won’t necessarily be interested in leveraging Interactive Brokers’ core competency around options and futures trading. Though with the RIA custodian business model under pressure itself — with first the collapse of trading commissions on most platforms, now followed by near-zero yields on previously lucrative cash sweeps — arguably the better way to look at the TradingFront/Interactive Brokers tie-up is not that advisers can purchase TradingFront as a technology overlay for Interactive Brokers, but that Interactive Brokers (similar to Altruist) is testing the willingness of advisory firms to pay a “technology fee’ to use its RIA custodial platform (especially since, as a subsidiary of Interactive Brokers itself, TradingFront ostensibly will remain focused on Interactive Brokers for the foreseeable future). Which means if TradingFront is successful in persuading RIAs to pay its technology fee as a part of using Interactive Brokers, it may set the precedent for other RIA custodians to begin assessing their own technology fees. With the caveat that, as the core technology to run an advisory firm becomes table stakes unto itself, it’s still not clear what segment of advisers the TradingFront-plus-Interactive-Brokers offering is differentiated enough to attract in the first place.

AI-driven Vise raises $14.5 million Series A led by Sequoia Capital, but is it adviser tech or simply another TAMP? There are currently 33 portfolio management platforms targeting the RIA market with full technology stacks and end-to-end workflow solutions. And that doesn’t include the 40-plus turnkey asset management platforms (TAMPs) where RIAs can outsource part or all of their investment management so they can focus on the business of growing their business. Vise.ai thinks it’s built a better mousetrap by leveraging “artificial intelligence” to build smarter, more customized portfolios, and monitor them in real time, with all-stars lining up for its latest funding round, led by Sequoia Capital (investors in Dropbox, Instagram, PayPal), and with participation from Steve Chen (co-founder of YouTube) and Jon Xu (co-founder of FutureAdvisor). Yet while the chairman of Vise, Shaun Maguire, thinks that it has the potential to become the “central nervous system of the wealth management industry,” once you look past the AI hype, it’s not clear that there’s anything new that advisers do not already have access to. The firm’s AI capabilities are focused on market analysis and investment selections, which suggests their AI isn’t actually about business efficiency for advisers but just a proprietary investment process that happens to be distributed through its technology, for which it will live or die by its ability to produce a better track record than BlackRock, Vanguard, UBS, State Street or other top asset managers (or not)? Notably, Vise.ai does imply that it uses machine learning to customize portfolios for clients as well, but it’s not clear how it can possibly have enough data on clients to do so. And in practice, the rise of direct indexing suggests that the future of portfolio customization for clients may be more about clients expressing their own preferences in their portfolios with an adviser’s help (not what an AI algorithm thinks they’ll want to invest in). When it comes to the core systems that Vise offers, there is little difference when it comes to its risk assessment, security restrictions, tax-loss harvesting and other client-side customizations — important offerings for sure, but again, not necessarily distinct from the “full-stack platform spanning the entire lifecycle of the adviser-client relationship” (as Vise.ai touts on its website) already in use by virtually every investment-centric RIA. And for those RIAs that do choose to outsource investment management, choosing from TAMPs like Envestnet, AssetMark, Brinker or others to receive high-quality portfolios, already customized to every client, that are monitored 24/7, allowing the advisers to focus on growing their business — again, it remains unclear where or how Vise will effectively differentiate (short of its investment performance results themselves). Which ultimately raises the question of how Vise (and its new $14.5 million war chest) will effectively penetrate the adviser channel in the first place. There are almost 17,000 SEC-registered RIAs in the US, but 80% of the assets are controlled by the top 20% of the firms. If Vise is going to increase its valuation enough to provide the ROI these new investors expect, it must grab some market share from this small target segment, which every other WealthTech vendor is already going after as well, with substantively similar technology and/or their own proprietary investment process that claims to generate superior investment returns. The wealth management industry is in the middle of a perfect storm, with investors pushing for more personalization, advisers looking for scalable technology to help them differentiate, and the industry rushing toward zero-commission trades (which further enable client portfolio customization without the friction of trading costs). The good news is that this confluence is creating opportunities for startups like Vise.ai to prove that their mousetrap can outperform decades of institutional investment experience. But as a starting point, they’ll need to figure out if they’re competing as a technology solution or a TAMP in the first place, and how they will genuinely differentiate in a crowded marketplace.

AdvicePay rolls out ‘Offices’ for enterprises as HTK and LPL adopt fee-for-service advice models. For most individual RIAs, the process of getting paid for financial advice is relatively straightforward: The advisory fee is swept from an investment account, the payment is transferred to the advisory firm’s bank account, and the dollars are remitted to the adviser-as-owner. In the context of broker-dealers, though, the process is somewhat more complicated, as commissions are paid to the broker-dealer as an entity which must then track the correct allocations of commissions across all its registered representatives to ensure the right reps get the right payments. And even in the context of a corporate RIA the process of advisory fees is more complicated as the firm collects fees from multiple clients across multiple advisers and must ensure that the right fees are passed through to the correct advisers. When it comes to financial planning fees, though, the process immediately gets far more complicated, as the enterprise cannot simply collect the commissions and/or advisory fees directly, calculate the appropriate allocations to their reps and remit accordingly. Instead, the client must be invoiced for the fee by the adviser, the check for the fee must be collected by the adviser, the check must be transferred to the home office for deposit, the compliance team must verify the services were rendered for the payment received, the deposited check must be cashed and cleared and reconciled by the finance team — and then some numbers of weeks later, the cash from the cleared check in the corporate account can be allocated and remitted back to the adviser. The end result is an extremely manual and labor-intensive multistep process, with multiple parties involved, each of which has its own role in the process (from the adviser delivering services to the administrative staff invoicing and collecting, compliance overseeing, the accounts-receivable team processing the check, the finance team reconciling it, all before the adviser can even be compensated) — all of which is hard to justify for the enterprise that only makes a very small slice off what is typically a $1,000 – $2,000 check at most (i.e., the broker-dealer’s cut might only be $50 to $100, which doesn’t even cover the administrative costs of processing the financial planning fee!). In this context, AdvicePay — which offers a payment processing platform to simplify and more heavily automate the collection of financial planning fees — announced this month a new Offices feature, which splits up the various functions of financial planning fee collection into the distinct roles that each party plays, allowing end advisers to customize their logos (but only with home office approval), office managers to create invoices (that queue up to compliance to reconcile with plan completion), and fee collections that will still go to the home office (as required, as advisers aren’t permitted to take custody of the client fees directly). In turn, AdvicePay also announced this month several new enterprise customers using the new Offices feature, including Penn Mutual’s insurance broker-dealer HTK and the largest independent broker-dealer, LPL, with nearly 17,000 advisers. From the industry perspective, though, the real significance of AdvicePay Offices, and the rollout of AdvicePay into LPL (along with its adoption last year by the Ladenburg network of broker-dealers and the Cetera network of broker-dealers) is a broader shift toward alternative (non-commission and non-AUM) fee-for-service business models for financial planning advice, from monthly subscription fees to annual retainers and more one-time planning fees as well, as it turns out that technology making it easier to accelerate and automate the collection of financial planning fees (especially recurring financial planning fees) is itself increasing interest in advisory firms to adopt new business models, just as the rise of the independent RIA custodian (and its ability to expedite the collection of advisory fees from investment accounts) in the 1990s accelerated the growth of the RIA AUM model. A trend that, with broker-dealers already trying to reinvent their own business models in a less-product-centric future and increasingly pivot toward more advice-centric business models, appears to be accelerating further as the coronavirus pandemic puts even more pressure on transactionally based advisers (whose one-time sales transactions slowed dramatically in the pandemic shutdown) to shift toward more stable recurring-revenue models (from AUM fees, to the fee-for-service recurring subscription and retainer fees that AdvicePay enables).

Smarsh buys Entreda as a future with more remote work increases the stakes for device management cybersecurity. For most advisory firms, “compliance technology” has primarily been about either managing required compliance workflows, from reviewing employee securities transactions and best execution reports to vendor due diligence (e.g., RIA In A Box or SmartRIA), and of course archiving advertising and employee communications (e.g., Smarsh or MessageWatcher). While “cybersecurity” was (and has increasingly become) a core compliance obligation, even firms that have the scale to deploy resources often do so through their technology team, whose job is to support employees and encourage cybersecurity best practices (e.g., keep your software patched) and teach how to avoid social engineering hacks (e.g., KnowBe4). But in recent years, technology solutions to manage cybersecurity have become a niche unto themselves in financial services, with providers like FCI and Entreda that proactively monitor all employee devices — from desktops to laptops to smartphones — to ensurethat they are properly patched, run proper anti-virus software, maintain secure encryption and follow cybersecurity best practices. And with the emergence of the coronavirus pandemic, and a surge of work-from-home activity, remote device management for cybersecurity purposes has taken on greater importance than ever. Which helps to explain why Smarsh, which provides compliance archiving solutions, announced the acquisition of Entreda and its cybersecurity device management platform (Unify). On its face, the deal makes sense simply for the opportunity of a more unified RegTech solution for financial services firms, as well as some market share synergies given that Entreda was primarily in small to midsize broker-dealers and RIAs, while Smarsh also served larger insurance companies and banks, which means a significant opportunity for cross-selling between the two firms. However, it’s also notable that Smarsh itself is owned by K1 Investment Management, which also recently exited adviser marketing platform FMG Suite, and appears to be redeploying its capital into adviser RegTech instead — an apparent bet that when it comes to financial advisory firms, the pandemic will result in a permanent uptick in the need for cybersecurity device management solutions, and more flexible remote work policies for advisory firms (with all the offsite desktops, laptops and smartphones that entails) may linger long after the pandemic shelter-in-place orders lift.

Aurora Capital private equity acquires FMG Suite to become the Hubspot of financial advisers? In an industry where, year after year, advisers report that their #1 source of new business is referrals from existing clients, websites are typically viewed as a “must check the box” minimal requirement, and not an actual focus for marketing (much less as a hub for a broader digital marketing effort). As a result, for most of the past 20 years, the providers of adviser website solutions tended to offer mass-produced, one-to-man’ solutions with a set of basic stock website templates that advisers (or whole enterprises of advisers) could stand up quickly but without much engagement, and with little to no focus on actually using the website to generate leads (which, again, was presumed to be unnecessary!). However, recent research on financial adviser marketing shows that digital marketing strategies, including a focus on Search Engine Optimization (SEO) to attract more prospects to the adviser’s website through local search, is actually one of the most cost-effective marketing strategies for advisers. That is leading adviser website providers to increasingly expand toward a wider range of digital marketing automation tools. Yet the irony is that while marketing automation solutions (that typically sit on topof websites) have become a wildly popular category of technology for small businesses in general, with mega players like Hubspot and MailChimp, there is remarkably little in the way of marketing automation tools for financial advisers in particular (who have unique compliance restrictions and requirements due to the regulated nature of the business). Recent entrants in the category have included startup Snappy Kraken, and the recent Twenty Over Ten launch of LeadPilot. But in practice, one of the biggest players in this space — primarily in the independent broker-dealer channel — is FMG Suite, which in 2011 began as an adviser website provider, in 2013 expanded into social media support and in 2016 began to offer more full-scale automated marketing solutions. Later in 2016, FMG Suite took outside capital from K1 Investment Management to further accelerate its growth, leading to a buying binge as FMG Suite expanded its market share in adviser websites by acquiring Advisor Launchpad, adding in deeper digital marketing capabilities with the acquisition of Peter Montoya’s Marketing Pro and Platinum Advisor Strategies, and even legacy CRM provider Advisors Assistant. Which effectively means that FMG Suite has acquired most of the key components necessary to replicate the equivalent of Hubspot for financial advisers, or more generally a full end-to-end suite of marketing automation tools for the compliance-heavy advisory industry. And now, after powering its acceleration for the past 3 years, K1 has announced that it is exiting its position, to Aurora Capital, which aims to take FMG Suite to the next level of integration and market penetration (and ostensibly help FMG Suite expand further into the P&C insurance channel, where Aurora has deep exposure from its ownership of Zywave). Which, if FMG Suite continues its playbook from K1, will likely involve additional acquisitions as FMG Suite further rolls up the components and market share it needs to expand further. So stay tuned for further FMG Suite acquisition announcements in 2021?

Envestnet announces ‘Connect’ as client portals move from performance reporting and file vault to a client collaboration hub. One of the longest standing challenges for financial advisers trying to leverage client portals is that, in practice, most clients don’t actually use them. In part, this is simply due to the fact that client portals have historically been a mechanism to deliver performance reporting information (as the physical quarterly statements of old became digitized), even as advisers encourage their clients to delegate portfolio management to the adviser and stop paying attention to short-term performance in the first place (effectively offering clients a portal and then discouraging them from using it!). In turn, many client portal providers began to expand the capabilities of their client portal into becoming a more holistic “client vault” as a means of making the portal more relevant — except again, most clients already have their own means of managing their files and paperwork (often with consumer tools like Dropbox), and the ubiquity of email (and secure-email extensions like ShareFile) has made collaborative file-sharing with clients increasingly feasible without the client-portal-as-vault approach. But now, Envestnet has announced the coming of a new client portal offering, dubbed Connect, that will still have financial performance reporting capabilities but is also aiming to expand beyond them with everything from contextually relevant articles and videos for clients (in partnership with AdvisorStream) to financial calendaring capabilities and even client to-do lists on their financial planning tasks (akin to recent adviser startup Knudge), and integrations to both Envestnet’s MoneyGuidePro financial planning software and also Edmond Walters’ Apprise Labs (Walters was reportedly a co-creator of Connect). Ultimately, though, the question remains what, exactly, clients will look to their client portal for in the first place? To the extent that the financial media already douses consumers (including and especially the clients of financial advisers) with content from all directions, it’s not clear that the client portal can be an effective news hub for the adviser-client relationship (at least relative to simply sending clients such articles via email directly), and integrations to long-term financial planning projections may not help given that in practice the numbers don’t necessarily move very much from day to day, month to month, or even year to year (given that they are long-term projections!). However, the introduction of client to-dos and the potential for a client service calendar represent a different kind of client portal relationship, one attached more directly to the tasks and activities genuinely relevant to clients (and not just ‘information’ that clients can either receive elsewhere, or are discouraged from looking at so often in the first place). All of which raises the question of whether Envestnet Connect will end out simply being an enhanced client portal, a content and communications hub, or whether Envestnet’s test of more collaborative client activities (e.g., to-dos and a calendar of financial planning engagement opportunities) is where the client portal will evolve next.

Could Plaid’s “Money In Excel” become a budgeting tool for clients of financial planners? If you ask the average American what is their financial lifeblood that they spend the most time monitoring, the typical answer is not their long-term retirement plan or even their portfolio, but their cash flow that moves in and out of their bank account every month. After all, if households don’t have control of their monthly cash flow, they’ll never have the dollars to save and invest in the first place (or will deplete what they have). And from a practical perspective, our balance sheets and even our investment accounts don’t really change all that often in a material way, while our bank accounts fluctuate monthly and even daily as money comes in and goes out. Yet the irony is that most financial planning software and client portals focus first and foremost on (updated) retirement projections and investment returns — or more generally, the client’s balance sheet — and not the client’s household cash flow. Which on the one hand, helps to explain why clients log into their bank accounts far more often than the client portals their advisers provide. It also helps to highlight what continues to be a huge gap for budgeting — or more generally, cash flow tracking – software for financial advisers, leading some advisory firms to adopt consumer solutions like Tiller Money or YNAB. But now account aggregation provider Plaid has announced a partnership with Microsoft, dubbed “Money In Excel,” that will allow any consumer (or the client of any adviser) to link their bank accounts directly to their own spreadsheets and begin to track their own continuously updated household cash flow themselves. In addition, Money In Excel will provide templates for tracking monthly spending, and recurring expenses, with basic expense categorization provided directly from Plaid’s data feed. Of course, tools like Mint.com already provide a similar service for consumers, but being locked into a third-party service means one’s data is often not portable (or at least, not in a usable way), and limits the ability to modify or adapt the interface. Money in Excel is in the end simply Excel, a spreadsheet that can subsequently be adapted in any way the user wishes, with data that the users themselves fully own and control. In the financial planning context, then, Money In Excel may become an appealing alternative for financial advisers looking to help clients get a handle on their own cash flow (who don’t already use financial planning software like eMoneyAdvisor that has at least some of these capabilities), especially since the client can share their Money In Excel spreadsheet directly with their adviser (unlike Mint.com or other online consumer budgeting solutions). And while Money In Excel won’t be free, at a cost of just $6.99/month (as a part of the new Microsoft 365 Personal account, or $9.99/month bundled into a Microsoft 365 Family account), it is inexpensive enough that advisory firms might just choose to purchase it for their clients as a part of their own financial planning client experience. Of course, the irony is that historically, financial advisers have already tended to use spreadsheets to solve any problem that industry software wasn’t built to solve. But with Money In Excel, the spreadsheet approach with clients may shift from a fallback solution to become the primarysolution (at least, until the industry itself fills the void with better adviser tools for budgeting and helping clients track their own household cash flow!).

Morningstar doubles down on its bet on a more ESG-centric (direct indexing?) future by buying out the remainder of Sustainalytics. In 2015, Facebook founder Mark Zuckerberg and his wife Priscilla Chan made waves by announcing the Chan Zuckerberg Initiative, a vehicle intended as a means of moving their substantial wealth into charitable nonprofit endeavors. It was deliberately not structured as a charitable foundation but as an LLC that would have more flexibility to engage in the kinds of socially driven initiatives they wanted to pursue. At the time, it was heralded as a sign of a coming tidal wave of interest — particularly among millennials — in the broad category of environmental, social and governance investing. And in fact in the time since, ESG has certainly proved to be more than a fad, and its interest and success has continued to grow as institutional clients, such as endowments and pensions, have issued ESG mandates. Now the retail investor tidal wave is following, led by the millennials that are coming into wealth. It is no secret that millennials will pay more for products and services that align with their values, and there’s no reason to believe that this won’t continue with their most important money decisions: where to allocate investment wealth. In addition, the narrative that ESG investing means sacrificing performance is steadily being revealed to be a myth as well, as ESG investments perform more than adequately to help the millennial generation achieve their goals. In this context, it wasn’t surprising that in 2015, Morningstar announced a relationship with Sustainalytics, which provides investment data and analytics on ESG-related factors. In 2017, Morningstar acquired a 40% stake in Sustainalytics, and now, Morningstar has announced that it is acquiring the remaining 60% of Sustainalytics. Strategically, acquiring Sustainalytics appears to be a hedge on the future for Morningstar, not just on the direction of investing in general but the way that investing occurs. As in practice, it’s very hard to invest with alignment to values if you’re only investing in, mostly, black box funds that are at best out of the investor’s control. Accordingly, Morningstar already tried to adapt its calling card — the 5-star fund rating system — into a 5 Globe system to rate funds on their sustainability. Yet if the world moves increasingly rapidly toward a values-aligned future — in which direct indexing may become the leading vehicle of choice because of its ability to more deeply customize a portfolio precisely to the investor’s ESG specifications — then Morningstar’s bread-and-butter business of simply rating funds (whether on performance or on sustainability) is fundamentally threatened. In other words, today the value is helping allocators understand which products are meeting the ESG mandates. But tomorrow it may become quantifying the alignment of values to the investor’s custom-crafted portfolio. After all, that vision for the future is fraught with challenges in practice, because values are extremely personal. One investor may believe that Nike is a socially responsible company for its work with Colin Kaepernick and other similar initiatives; another investor may believe that Nike is NOT socially responsible because of its alleged use of sweatshop labor overseas. Now extrapolate those challenges across the universe of equities, and it quickly becomes a complex problem! Nonetheless, it is a problem that could and should certainly be solved, and to the extent that direct indexing may be the future, its value may be inextricably linked to the implementation of values-aligned portfolios. It seems that Morningstar believes in this future as well and is making an increasingly big bet on it. Can it deploy the technology to make it a reality?

Fidelity rolls out new AI Virtual Assistant to support WealthScape back-office workflows. For nearly a decade now, Artificial Intelligence has been hailed as one of the Next Big Things in business, including among financial services (e.g., robo-advisers). Yet in practice, the front-office roles of interacting with clients, including and especially on their complex and ever-changing financial planning needs, has proven remarkably resistant to any intrusion from robots and artificial intelligence. Instead, it’s the back-office work of financial services – the highly standardized, process-driven, repeatable tasks – that are increasingly exposed to robo automation. Which is not only leading to new investments into financial technology to support more back-office process automation — from FTV Capital recently taking a stake in Docupace to expand document management into back office process automation to this month’s announcement of Franklin Templeton investing into AdvisorEngine and its Junxure CRM back-office automation potential — but also to the use of artificial intelligence to provide support for those back-office processes. For instance, last year advisory firm Wela launched Benjamin, intended to be a kind of virtual AI-driven assistant to guide back-office team members on key operations functions (e.g., the status of transfers, daily net asset flows of the advisory firm, etc.). And now, Fidelity itself has announced the launch of a new AI-driven WealthScape Virtual Assistant, intended to provide support for advisers using Fidelity’s back-office WealthScape platform (and use AI to learn from the questions that advisers ask to better anticipate the educational information and support that advisers may need to preemptively address questions that arise when engaging in common WealthScape workflows and processes). In other words, Fidelity’s use of AI isn’t meant to replace any of the advice function of the advisory firm, nor even its staff support functions, but instead to learn what its users need in order to make its own back-office technology easier and more usable so advisers will never need to call for support in the first place, as a form of AI-driven help desk (a la Capacity). Which makes sense in the current environment, as call volumes to platforms like Fidelity’s have exploded upwards (making any level of technology automation/enhancements a positive ROI), and more generally given that the whole point of back-office technology is to support advisory firms to the point that the technology just works, and there’s no human interaction needed in the first place — not to eliminate humans from the advice process, but to shrink the back office and increasingly focus more and more of the resources of advisory firms on the client-facing human interactions instead.

New Product Watch: Will PlanTechHub Become the next big financial planning software by actually showing the value of financial planning? Financial planning software has gone through several major innovations over the decades, from the early product-centric pioneers like Financial Profiles in the 1980s, to the spreadsheet-style intensive cash flow projections of NaviPlan in the 1990s, the rise of goals-based financial planning software of the 2000s with MoneyGuidePro, and the emergence of account-aggregation-portal-based planning software from eMoney Advisor in the 2010s. The fact that planning software has moved in surprisingly consistent 10-year cycles, and the reality that current market share is largely dominated by a small number of players, have in turn raised the question of what the next big thing will be in financial planning software that comes to dominate the 2020s, and when it will finally appear. And now, the first prospective entrant has arrived: PlanTechHub, co-founded by Chad Blythe (former vice president of sales for MoneyGuidePro and NaviPlan, and former president of Advizr), chief technology officer Eric Harrell (a former senior software designer at MoneyGuidePro), and Richard Flaherty. At its core, the distinction of PlanTechHub is that it’s built to develop financial plans more quickly, not by being simpler planning software, but simply more iterative, so clients can begin with a more modular approach in a primary area of concern, and expand into additional modules to develop their comprehensive plan over time. Client data-gathering can be conducted directly into a client profile page, and advisers then quickly begin to build scenarios that clients might consider, with suggested actions (i.e., recommended action steps) that clients might evaluate, what-If considerations that clients must also bear in mind (factors that may be out of the client’s control but still need to be considered in the plan, such as what future inflation may turn out to be or what their life expectancy will be), and delve into workshops (where the adviser can delve further into a potential scenario, whiteboard-style, and change the details of the suggestions to evaluate the possibilities and trade-offs, without disrupting the original plan). What’s perhaps most unique about PlanTechHub, though, is the way it naturally frames the client’s original baseline, and how their financial situation will change if the adviser’s suggested actions are implemented, directly demonstrating the value of the adviser’s advice continuously within the planning software itself (and with a coming plan history module that will further enable advisers to show all the historical action steps that have been taken in the client’s plan as a demonstration of the cumulative value the adviser has provided throughout the adviser-client relationship!). The caveat, though, is that with most advisory firms already using existing financial planning software, it’s not clear whether PlanTechHub’s “show the value of the adviser’s recommendations” approach is a compelling enough differentiator to persuade advisers to go through the hassle of switching planning software (and/or whether, if popular enough, competitors will simply emulate the approach), in a realm where simpler financial planning software has long struggled to actually gain market adoption (as instead, advisers using planning software tend to go deeper instead). And in practice, figuring out the best way to show the incremental improvement of an adviser’s recommendations — which variously might increase wealth, or decrease wealth but increase lifestyle income, or might decrease lifestyle income but improve the probability of success — is itself a challenge to show in practice, without making the planning software output overly crowded and difficult for the client to follow. Nonetheless, with financial planning software being ripe for the next decade’s disruptive new entrant, and PlanTechHub coming out of the gate with an aggressive pricing of $550/adviser/year and now offering a 30-day free trial, at the least, it’s game on for competition in financial planning software, and for advisers, the welcome addition of a new entrant that’s actually focused on demonstrating the incremental value added with each new recommendation we provide to our clients!

-------------------------------------------------------------------------------------------------------------------

We’ve updated the latest version of our Financial Advisor FinTech Solutions Map with several new companies, including highlights of the “Category Newcomers” in each area to highlight new FinTech innovation!

So what do you think? Is Goldman’s end game with Folio a vertically integrated custodian for its own advisory services, a robo-adviser for consumers, or a play for small (or large breakaway) RIA custody business? Will fee-for-service financial planning models continued to gain traction as it becomes easier to collect financial planning fees with no more physical paper checks? Will financial advisers use Money In Excel to help with cash flow and budgeting for their own clients? Is PlanTechHub’s new value-of-advice-centric approach enough to make advisory firms switch from existing financial planning software providers?

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay, and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’s Eye View. You can follow him @MichaelKitces.

Disclosure: Michael Kitces is a co-founder of AdvicePay, which was mentioned in this article.

Special thanks to Kyle Van Pelt, who wrote the section on Morningstar Sustainalytics, and to Craig Iskowitz who wrote about Vise. You can connect with Kyle via LinkedIn (or follow him on Twitter at @KyleVanPelt), and with Craig on LinkedIn (or on Twitter at @craigiskowitz).

The 25-year industry veteran previously in charge of the Wall Street bank's advisor recruitment efforts is now fulfilling a similar role at a rival firm.

Former Northwestern Mutual advisors join firm for independence.

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound