The April edition of the latest in financial #AdviserTech kicks off with the big news that Wealthbox has raised a new $31 million Series B round to capitalize its efforts in moving further upmarket to challenge the hold of Redtail and especially Salesforce on the largest adviser enterprises. Adviser adoption of CRM systems is now so high, it’s a virtual certainty that current CRM systems can only grow by capturing market share away from competitors.

From the broader industry perspective, though, the real shift that’s underway is the transition of adviser CRM systems from their roots as the tool that captures client contact information and communication history to one that drives the advisory firm’s key workflows. As advisory firms provide increasingly broad and holistic advice to clients, it’s no longer feasible for the firm to run just from its RIA custodian or broker-dealer investment platform as the hub; instead, the adviser CRM system is becoming the hub, around which the rest of the firm’s systems and processes are built. That’s expanding the opportunity set for adviser CRM.

From there, the latest highlights also feature a number of other interesting adviser technology announcements, including:

• Summit Wealth Systems raises a $20 million Series A round as its founder Reed Colley, who previously founded Black Diamond, aims to build the next generation of performance reporting for clients.

• Advyzon launches a new TAMP offering for the adviser users of its portfolio management plus CRM system.

Read the analysis about these announcements in this month's column, and a discussion of more trends in adviser technology, including:

• Savvy Wealth raises $7.3 million to fund its own tech-based advisory firm in the hopes of out-competing advisory firms that are struggling to build their own tech.

• In the meantime, we’ve also launched a beta version of our new Kitces AdviserTech Directory, to make it even easier for advisers to look through the available adviser technology options to choose what’s right for them.

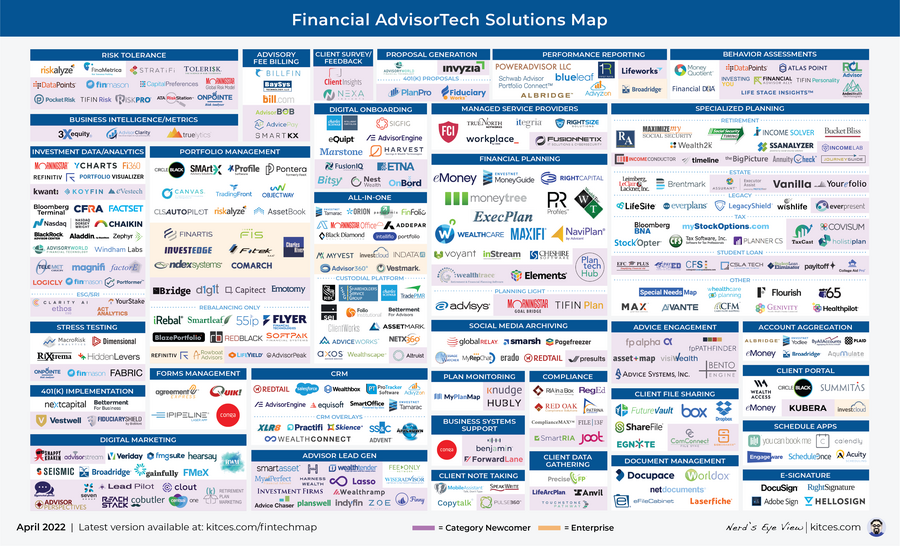

Be sure to read to the end, where we have provided an update to our popular Financial AdviserTech Solutions Map!

AdviserTech companies that want their tech announcements considered for future issues should submit to TechNews@kitces.com!

In the earliest days of the financial advice business, the only way advisers kept track of their clients’ contact information was to write it down in a book. And that book of client names to call upon to do ongoing business was so valuable, advisers upon retiring could sell their book of business to another adviser who needed people to call upon. The emergence of computers in the 1980s began to digitize the adviser’s physical book of business (client names) into a digital Rolodex of contact information, which captured not only names and phone numbers but a history of all communication with that contact, in what became known as customer relationship management software.

Through the 1990s, a number of CRM systems began to be adopted by the financial adviser industry — including ACT! and Goldmine — but the deeper nature of financial advice relationships, which go beyond just tracking contact information and the latest sales communication, increasingly necessitated adviser-specific CRM tools, leading to the birth of Junxure, ProTracker and Redtail CRM by the early 2000s. Where Redtail in particular managed to outdistance its competitors by building more quickly to the cloud, while others languished in server-based environments, and more successfully moving upmarket to adviser enterprises (in particular, independent broker-dealers), which housed the majority of the adviser seat-count opportunities.

Over the past decade, though, adviser CRM has been in the midst of another transition — from being a glorified Rolodex and contact management system into a full-fledged hub of the adviser’s business. Because as firms become more planning-centric and less tied to their broker-dealer or RIA custodian — because they need more than just the investment resources of those platforms — a stand-alone CRM system is becoming more crucial, not just for contacts, but as a workflow and process engine. This has not only further boosted the growth of Redtail as it built out workflow capabilities but has driven rapid growth for Salesforce. In particular, among the largest adviser enterprises with the most complex workflow needs for which Salesforce is arguably the most capable of customization, albeit at either a significant cost to build those customized workflows, or the need to use a third-party overlay like XLR8, Skience or AppCrown.

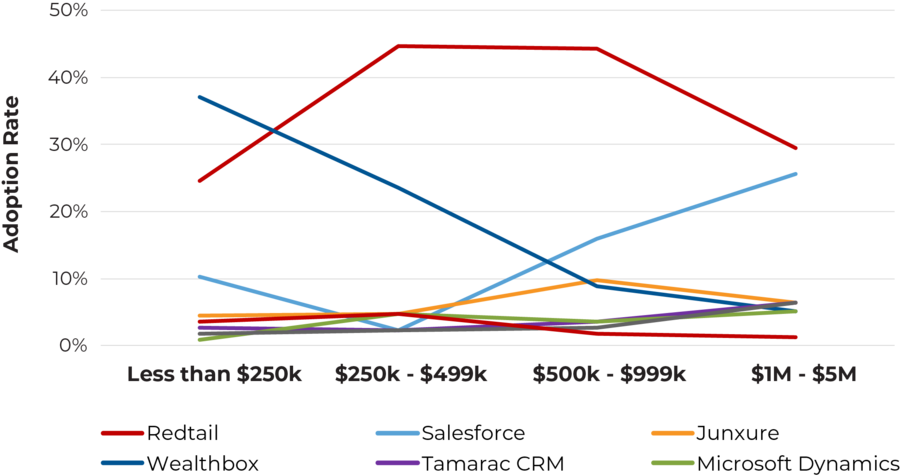

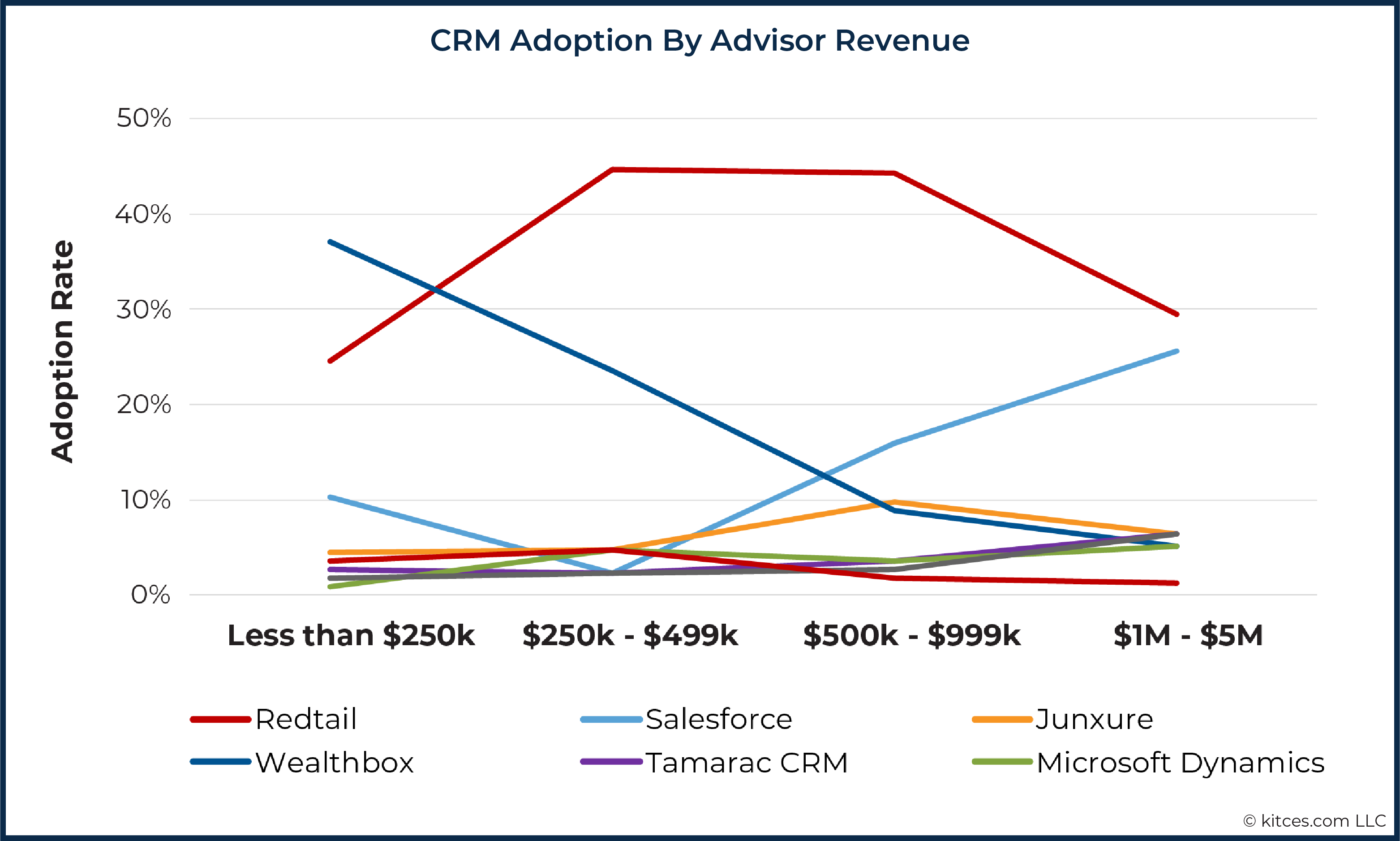

In this environment, Wealthbox first emerged as a new adviser CRM competitor in 2014. Having been built from the start in the cloud and not needing to rely on legacy technology, relative to its competitors that were originally built on 2000s architecture, Wealthbox’s offering had a more modern user interface patterned after a client feed approach similar to the Facebook feed, and began to capture market share where nearly all AdviserTech starts: with independent RIAs and the solo advisers of independent broker-dealers, selling one adviser at a time, because they have the most straightforward needs and the fastest sales cycles, while the latest Kitces AdviserTech Study shows that Redtail continues to thrive with midsize firms, and Salesforce is actively being bought among the largest practices.

But now that it’s cleared 14,000 users, Wealthbox in March announced a hefty $31 million Series B round to expand and accelerate its move upmarket into mega-RIAs, and especially into the midsize to large independent broker-dealer marketplace that still holds the majority of the adviser seat count and market opportunity. This is a uniquely capital-intensive endeavor, as the reality is that larger firms simply have greater enterprise demands, from more permissioning layers (to handle the various tiers of reps, teams, branches/offices, compliance and home office staff, each needing different levels of access to certain clients or types of client data), to more integrations (both to a wider range of providers, and to enterprises’ own internal/proprietary systems), to simply having more features to handle the greater complexity of enterprises that have larger multidepartment workflows.

The question, though, is where exactly Wealthbox will manage to gain market share. In practice, CRM has the highest adoption of any AdviserTech system, nearly 90% according to the latest Kitces AdviserTech study, and the bulk of those without CRM systems are simply too small or too new to need one, yet. Wealthbox is already winning a plurality of the new startup advisers. This means growth in the enterprise market will have to come almost entirely at the expense of competitors — e.g., Redtail and Salesforce, along with less popular but still present competitors like Microsoft Dynamics and Junxure — in an environment where only about 1-in-16 advisers changes CRM systems in any particular year. CRM system changes are the most arduous among the largest firms that have the most data and existing workflows that must be rebuilt/remapped into a new provider (i.e., the switching costs in internal process change and adviser retraining are quite high).

To some extent, Wealthbox’s increased ability, thanks to its Series B, to be present and competitive in the enterprise RFP process for CRM systems — for those that are looking to change — will give it opportunity to win incremental market share. Though as it stands right now, Wealthbox’s adviser satisfaction ratings in the Kitces AdviserTech study were competitive but not materially higher than those of its competitors. This makes it difficult to win a large share of the market on user experience alone.

In the end, Wealthbox’s ability to move upmarket and materially capture new market share is likely to be less a function of its existing feature set, and more about whether Wealthbox can innovate deeply enough when it comes to enterprise workflow capabilities, to have a workflow/process engine compelling enough for advisers and especially enterprises to be willing to absorb the switching costs and make a change in a highly competitive CRM environment. This, in turn, amps up the pressure on Redtail and Salesforce to bolster the depth and usability of their own workflow engines enough to reduce the desire and willingness of advisers to switch in the first place.

In the 1980s and 1990s, the primary business of financial advisers was selling mutual funds for a commission, and the technology of choice was Morningstar and its Principia Pro, which provided one-page performance summaries for each of those mutual funds so advisers could share with their clients how their selections were doing. In the long run, advisers face ongoing pressure to show that they’ve created favorable results for their clients in order to retain them.

In the 2000s, the rise of online brokerage firms and the emergence of no-transaction-fee platforms suddenly made it possible for consumers to analyze their own mutual funds online and buy them directly — without paying a commission to the adviser — forcing advisers to begin a business model shift to what ultimately became the assets under management model, where the value was not just picking mutual funds but creating a diversified asset-allocated portfolio. This, in turn, meant advisers needed a new kind of performance reporting system to show not how their individual funds were doing, but their entire asset-allocated diversified portfolio. The result was the rise of a number of portfolio performance reporting systems, including Orion, Black Diamond and Tamarac, which all emerged in the 2000s to become a staple of the adviser tech stack for any firm on the AUM model.

Yet in the nearly 20 years since, arguably very little has changed in performance reporting systems. Tools may have shifted from local servers to the cloud, with updates to their underlying calculation engines and the graphical design of their reports. But the core value proposition of performance reporting systems remains largely unaltered.

In that context, it’s notable that in March, Summit Wealth Systems announced the launch of a whopping $20 million Series A round as it emerges from private beta with a new next-generation performance reporting and portfolio management system.

Created by Black Diamond founder Reed Colley and former Advent executive Anthony Sperling, Summit is notably being positioned not simply as “performance reporting” or “portfolio management” software, but as a “Wealth Operating System” engine called “Abundance” — meant intentionally to move away from the traditional “Are We Okay?” scarcity mindset of clients, and toward one of abundance. Accordingly, Summit’s WealthOS claims it’s taking a more holistic balance sheet approach to reporting on affluent clients’ abundant assets and aims to tie client wealth more directly to their values with a broad range of third-party data sources for account aggregation.

In practice, Summit appears to be offering all the core functionality advisers have come to expect from such systems — including performance reporting, portfolio management, billing, a client portal and integrations to key third-party systems. Though Summit is also highlighting a unique data architecture that makes each adviser’s data independently available to them and fully segregated from other advisers as a private data warehouse that advisory firms don’t have to build themselves. This not only provides advisers more protections for data security and more control in how their data is used, but also greater independence from their custodians and platforms by better owning and controlling their data, and potentially makes it easier for advisers, at least at larger enterprises, to build more of their own tech stack on top of Summit.

Ultimately, though, Summit’s success will likely be determined not by its ability to provide the standard features that the other performance reporting and portfolio management tools offer, but by its ability to create a new approach to performance reporting or more generally, the full spectrum of the clients’ wealth data in the advisory firm’s Summit-based data warehouse that is substantively different and beyond the current generation of tools. For which a more holistic and values-based approach appears to be well-aligned to the broader financial adviser industry's shift toward more holistic and values-based advice. But can that be expressed in software in a manner compelling enough to get advisers to go through what is often a year-long project to make a switch to a new performance reporting system?

One of the biggest tensions in the world of AdviserTech today is drawing the line of where technology ends and asset management services begin. On one hand, asset managers are increasingly tech-ifying themselves in the hopes of both improving their margins, differentiating their offerings to advisers, and perhaps being able to access tech-style valuation multiples. On the other hand, technology firms are increasingly pivoting toward asset management in the hopes of being able to supercharge their revenue by pricing in basis points on assets, which can generate far more revenue than charging per-user, per-client or per-account software fees. And the ongoing convergence has blurred the lines between the two.

As a result, in today’s market, firms like AssetMark, historically a TAMP, increasingly compete with Orion, historically, a portfolio management software provider, both of which compete with the goliath known as Envestnet, the original platform-TAMP that used its technology to provide a marketplace of TAMP and SMA solutions to advisers. That led to a number of TAMPs consolidating into technology firms (such as Brinker selling to Orion and Adhesion selling to Vestmark), and a number of technology companies trying to roll out investment management offerings, most notably as model marketplaces offered by providers ranging from Oranj to Riskalyze.

The caveat, though, is that asset management itself is still first and foremost a distribution game. That means, in general, asset managers — whose roots are grounded in the distribution of investment management — that add in tech while keeping their investment management core have had far more success than technology firms trying to offer model marketplaces that require different strategies to distribute than just offering technology itself.

In this context, it is notable that in March, portfolio management tech provider Advyzon announced the launch of its own Advyzon Investment Management offering, a turnkey asset management provider solution for the advisers already using Advyzon.

From an investment management perspective, Advyzon’s TAMP is relatively typical, offering a series of different portfolio models (including active/passive diversified asset-allocated models, an ESG model, a tax-sensitive ETF model, an alternatives portfolio and a direct indexing offering), and the usual suite of TAMP services (trading and rebalancing, billing, reporting, and support on paperwork and as a custodial liaison), for which Advyzon is charging a TAMP-typical AUM fee of up to 0.35%.

What’s unique about Advyzon’s TAMP, though, is its positioning in the marketplace. Unlike some technology-turned-TAMP/marketplace providers (such as Oranj), Advyzon actually does have a sizable existing base of more than 1,000 advisory firms to which its TAMP solution can be distributed. And because of the all-in-one nature of Advyzon’s portfolio-management-plus-CRM (but not including financial planning) solution, the software has an especially strong connection to investment-centric advisers operating on the AUM model where a TAMP outsourcing solution is especially well-aligned. In other words, Advyzon has the right type of existing base of advisers to be viable for cross-selling TAMP services.

From the broader industry perspective, Advyzon’s shift to a TAMP offering is also notable in that ironically, the recent shift of TAMPs to become tech companies, and tech companies acquiring TAMPs means that advisers who already like and use Advyzon may struggle to find TAMPs that will work with them on Advyzon and instead would have likely required them to switch to another platform. This is significant challenge given that Advyzon scored higher than Orion, Black Diamond or Tamarac for portfolio management in the latest Kitces AdviserTech study. This means that the vertical integration of TAMPs and technology providers may have forced Advyzon to launch a competing TAMP for its advisers who wanted to outsource investment management while remaining with Advyzon.

Ultimately, a TAMP will still live or die by its ability to distribute its investment management solution to advisers, and distribution is always a challenge in a hyper-competitive environment for asset management. But founder Hailin Li’s Morningstar roots, as the original chief architect of Morningstar Office, have helped Advyzon recruit a deep bench of talent to lead its TAMP (including Brian Huckstep, former head of U.S. asset allocation at Morningstar, as CIO, and Meghan Holmes and Lee Andreatta, both formerly of Schwab Advisor Services, as COO and CEO, respectively), and Advyzon seems uniquely well-positioned to compete given the quality of its technology that has made its adviser users prefer an Advyzon TAMP to leaving Advyzon for another TAMP.

One of the greatest benefits of the growth of AdviserTech over the past decade has also become its biggest pain point: the sheer proliferation of the number of AdviserTech solutions. This has led to the paradoxical outcome that there have never been more technology solutions for advisers more capable of integrating to one another. Yet the overwhelming, exponential increase in the number of point-to-point integrations among them means that advisers are increasingly frustrated by the lack and depth of quality integrations that actually exist across their tech stack.

At one end of this spectrum, the integration challenge is leading more AdviserTech providers to expand toward all-in-one solutions that offer more of the core tech stack on a single platform, which only has to integrate deeply with itself to provide the desired experience. At the other end of the spectrum are advisory firms that are increasingly looking to build their own proprietary tech stacks to fully control their own adviser and client experiences to make them more efficient and seamlessly integrated.

Of course, the caveat is that most advisory firms were launched to be provide advice to clients, not to build technology, and relatively few firms have managed to fully bring technology in-house successfully. Instead, the firms that are aiming to be technology-first are being launched as technology firms — or at least, tech-enabled financial advice firms — from the start, such as Facet Wealth, which aimed from the beginning to build its own internal proprietary AdviserTech tools in the hopes of being able to scale itself to 250-plus client relationships per adviser with technology efficiencies.

Now, the latest newcomer to emulate the approach is Savvy Wealth, which in February announced a $7.3 million seed funding round to fund a Facet-Wealth-style vision of becoming an “all-in-one technology-powered financial services firm” — in other words, not only to be an all-in-one technology stack that advisers can buy, but to actually become the financial services firm that uses its own tech stack to deliver advice efficiently.

However, as the robo-advisers themselves discovered a decade ago, financial advice is not an “if you build it, they will come” offering, raising the question of how exactly Savvy Wealth intends to scale up the number of clients it has and the number of advisers serving them. Savvy’s capital announcement suggests that it may even look to acquire wealth management firms as a way to bulk up its client and adviser count.

Except that even if Savvy allocates two-thirds of its newfound capital — or about $5 million — for acquisitions, at a typical 2X-plus multiple for independent advisory firms, this only provides Savvy the capital to acquire roughly $250 million of AUM, far short of what it would need to truly scale up. In fact, Facet Wealth similarly pursued an acquisition-style strategy early on to grow its client base only to ultimately abandon it as the acquisition costs were prohibitive, especially when considering the staffing it takes to source and execute acquisition deals, along with integrating the acquisitions themselves after they close. As a number of RIA aggregators have found over the past decade, it’s especially difficult to rapidly execute a high volume of acquisitions where the selling firm is expected to be assimilated into the acquirer, simply given the independent-minded streak of most independent advisers.

Ultimately, then, the real question for Savvy is not whether it can build better tech, per se, but whether it can develop scalable marketing and business generation systems that can attract a critical mass of clients who are willing to switch to work with Savvy’s advisers and whether Savvy can hire or acquire enough skilled financial advisers to keep up with the demand if they’re able to find traction with clients in the first place. In the end, the biggest blocking point to scaling up financial advice businesses is not actually the scalability of technology efficiencies or lack thereof, but the scalability of marketing and whether it can bring client acquisition costs down low enough to be able to scale in the first place.

The RIA custody business is a scale business. So much so, in fact, that every major RIA custodian today didn’t even start out as an RIA custodian. Instead, it built its RIA custody business by leveraging the existing infrastructure and scale it already had from a related business: from Schwab and Fidelity, and previously TD Ameritrade, using their retail brokerage infrastructure to offer RIA custody, to Pershing and LPL and Raymond James using their broker-dealer custody/clearing platform as a basis to expand into RIA custody. The reality is that established RIAs, which themselves have high demands based on the depth of services and affluence of their own clientele, require and expect a lot in terms of both technology and service.

Up until a few years ago, the end result of this dynamic was a near oligopoly of Big Four RIA custody providers (Schwab, Fidelity, TD Ameritrade and Pershing), and a handful of second-tier RIA custodians that serve various niches of the adviser marketplace where they can remain competitive against the Big Three for their subset of adviser clientele. This became even more concentrated when in the fall of 2019 Schwab announced that it was going to acquire TD Ameritrade, a deal so large that it produced a lengthy Department of Justice investigation to ensure it didn’t necessitate antitrust intervention.

Ultimately, the DOJ antitrust concerns were dismissed, in large part due to the expectation that other financial services firms would be attracted into the marketplace to compete as RIA custodians to fill the competitive void left by TD Ameritrade’s acquisition. A number of TDA-custodied firms were signaling that they did not want to continue to be served by Charles Schwab, especially given that a material segment of RIAs at TDA had gone there specifically because they were once rejected by Schwab as being too small. This made it all the more notable when the storied Goldman Sachs announced within barely six months of the TD Ameritrade acquisition, in the spring of 2020, that it was acquiring Folio Institutional, one of the secondary RIA custodians that Goldman would use to expedite its own competitive launch into the RIA custody business.

Yet now, nearly two years later, RIABiz reports that the Goldman Sachs RIA custodian launch is indefinitely delayed. After it announced Steward Partners as an RIA custody launch partner last summer but missed several anticipated launch dates, it’s now not expected to even begin to onboard Steward clients until this fall. Goldman still won’t even publicly commit to a date, signaling that its own internal launch timeline is still uncertain and raising the possibility that the launch may not come until 2023. This is notable, as Schwab’s own timeline to complete its integration with TD Ameritrade is also slated for completion in mid-2023, such that Schwab may manage to complete its entire multiyear integration faster than Goldman could even buy its way to launch a full-fledged upstart competitor.

Ultimately, the fact is that even Goldman Sachs, with its capital to acquire and its existing depth of team and resources, is struggling to engage in a timely launch of an RIA custodial competitor after several years. This highlights the sheer challenge of what it actually takes to be competitive in the RIA custody business. In Goldman’s case, the delays are rumored to stem from the complexity of integrating Folio’s basket trading window approach into a more flexible intraday trading platform for larger RIAs. But whether it’s trading systems or reporting systems or data integrations or service teams (as large RIAs, in particular, have high expectations for the quality of their service teams), the table stakes of what it takes to be competitive in RIA custody have never been higher.

In the long run, Goldman should still manage to eventually launch its RIA custody competitor. This is likely to be especially competitive in the wirehouse breakaway segment, where advisers and their clients care about the brand of the platform, and the cachet of Goldman’s reputation in private wealth (on top of its bona fide capabilities for serving ultra-HNW international clientele) will still carry weight relative to retail brands like Schwab. Even if it’s long after the window in which Goldman might have capitalized by trying to draw away TD Ameritrade advisers unhappy with the merger, who will by Goldman’s launch have been integrated into Schwab or have already found an alternative.

Still, the fact that Goldman Sachs' acquisition of Folio Institutional for $250 million to jump-start its RIA custody launch is still leading to what may be a two-to-three-year launch path for a competitive offering highlights just how difficult it really is to compete. It also paints an even more daunting picture for other competing RIA custody upstarts that may be trying to enter the picture in the years to come. Unfortunately for the end RIAs and their clients, it means the RIA custody oligopoly doesn’t seem likely to break up anytime soon.

In the early days of the internet, the World Wide Web was primarily a finding machine for information, and the search engines that did the best job of parsing the tremendous breadth of online information to surface the most relevant information were most successful, such as Google. Within a decade, though, the internet shifted from just finding information to finding solutions, buying products and especially services online, and using the internet to vet those offerings. In the early 2000s, this led to the rise of online review platforms, from Angie’s List to Tripadvisor to Yelp, where consumers could rate their experiences and provide reviews of the services they received.

Yet even as review services proliferated in most service industries, they have noticeably lagged among financial advisers. In part, this is simply due to the fact that in most service industries, only a small percentage of customers ever leave a review. For providers that may have hundreds of customers each year, that can still quickly reach a critical mass of reviews, but for financial advisers who may only have 75 to 100 ongoing client relationships at capacity, it can result in no more than one to three client reviews and by then, the adviser is already at capacity. Historically, advisers couldn’t do much to try to increase the rate at which reviews were left, due to the industry’s long-standing restrictions against soliciting clients for testimonials.

However, in early 2021, the SEC updated its testimonial rule for the first time in nearly 60 years, and recognizing the proliferation of third-party review sites and the way consumers use those reviews to make better decisions about service providers, opened the door for financial advisers to begin to solicit and use client testimonials. This, in turn, has sparked a number of adviser lead generation services to launch in the past 18 months that are all pledging to become the next Yelp for advisers. They are collecting and housing third-party client testimonials and providing those reviews for consumers to help them choose their own adviser, including Finance Friends (now Onesta), Wealthtender and more.

Now IndyFin, a lead generation service for advisers, has announced a new $2.2 million round of capital. It is positioning to become the Yelp for financial advisers by leveraging the new SEC testimonial rules for advisers to solicit their clients to leave reviews. IndyFin can then use the reviews to help consumers find their own new adviser with the most favorable reviews. Advisers who claim and fill out their profiles can then receive those leads directly from IndyFin, and similar to other lead generation competitors, pay a success fee to IndyFin for each new client that closes.

Notably, though, IndyFin is taking a more vetted approach to its marketplace of advisers for consumers and is highlighting the rigorous vetting that advisers will have to go through to be included in the IndyFin network. This raises the question of why advisers would solicit clients to leave reviews on IndyFin’s website if they might not pass the vetting process. If only successfully vetted advisers use IndyFin’s reviews, then ultimately it won’t have the breadth of reviews that a broad-based provider like Yelp does. While businesses can claim their Yelp profiles for additional features, any consumer can leave a review for any business on Yelp, regardless of whether the business claims the review or has been vetted by Yelp. This is what helped Yelp gain a critical mass of reviews to become a known brand.

In fact, the question of whether all advisers will steer their clients to IndyFin to leave reviews, or only those who are successfully vetted by IndyFin while other advisers refer their clients elsewhere, highlights the broader issue that in the end, review sites tend to benefit from network effects. The greater the volume of consumers leaving reviews and advisers participating, the more valuable the service is, and the more consumers leave additional reviews and the more additional advisers participate. In the end, there probably won’t be multiple Yelp-for-Advisers sites. Instead, the most likely outcome is that one will become the market leader that best gains the critical mass of consumer reviews, adviser participation, and most importantly media/consumer recognition. The coming year(s) will be a race to see which one wins.

It seems that the most likely winner may be Yelp itself. After all, as far back as 2014, the SEC acknowledged that if a consumer independently leaves a review on an independent third-party website, it was permitted under the prior testimonial rules. The regulatory concern was never about third-party review sites, but about advisers using client testimonials in their own marketing, where there was a risk that advisers might be selective in cherry-picking the best testimonials and give a distorted picture to consumers. Third-party review sites that the adviser doesn’t control never had that problem in the first place. As a result, consumers can often already find well-reviewed advisers on Yelp in their area, and the permissiveness of the new SEC testimonial rules, which make it easier for advisers to outright solicit clients to leave reviews on Yelp, may just amplify Yelp’s lead.

In addition, advisers who use Yelp benefit because, while there is a cost to claim the Yelp profile, it’s a small fraction of what lead generation services charge for each lead and/or as a success fee for each closed client. From the adviser’s perspective, Yelp already has better consumer recognition. It’s more commonly used, is more likely to have a critical mass of reviews, and is less expensive for the financial adviser to rely upon, along with advisers claiming their Google My Business profile and similarly obtaining client Google Reviews that show up in local search.)

Ultimately, the 2021 change in the SEC’s (anti-)testimonial rules that for so long had at least limited how much advisers could solicit client reviews will likely increase the frequency of clients leaving reviews and how often advisers solicit clients to do so. There’s clearly a need, desire and willingness among advisers to pay for a wide range of lead generation services. In the long run, when it comes to building adviser review sites in particular and emulating the Yelp model for financial advisers, it’s not clear whether or why any of the upstart services may be able to execute a “Yelp-for-advisers” model better than Yelp for advisers.

In the meantime, we’ve rolled out a beta version of our new AdviserTech Directory, along with making updates to the latest version of our Financial AdviserTech Solutions Map with several new companies, including highlights of the Category Newcomers in each area to highlight new FinTech innovation!

So what do you think? Can Wealthbox win business away from Redtail and Salesforce in the larger enterprise market? Will advisory firms be open to a new, more holistic, values-based approach to performance reporting for client households? Will Goldman Sachs eventually be able to break the current RIA custodian oligopoly? Do you think advisers will adopt third-party client review platforms like IndyFin, or just engage more actively with existing platforms like Yelp and Google Reviews?

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter at @MichaelKitces.

Relationships are key to our business but advisors are often slow to engage in specific activities designed to foster them.

Whichever path you go down, act now while you're still in control.

Pro-bitcoin professionals, however, say the cryptocurrency has ushered in change.

“LPL has evolved significantly over the last decade and still wants to scale up,” says one industry executive.

Survey findings from the Nationwide Retirement Institute offers pearls of planning wisdom from 60- to 65-year-olds, as well as insights into concerns.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound

{kind=link}