The March edition of the latest in financial #AdvisorTech kicks off with the news that Conquest, a Canadian financial planning software provider founded by the person who previously founded NaviPlan, has raised C$24 million of private equity capital in preparation for expanding its reach into the U.S. Conquest hopes its technology-aided ability to analyze a client’s plan and suggest “next-best decision” strategies for advisors to recommend to their clients will allow them to break into the crowded U.S. market. At best, it will still be a substantial uphill battle, given the hassle of switching from one financial planning platform to another and the fact that most advisors are generally satisfied with their current financial planning software in the first place.

From there, the latest highlights also feature a number of other interesting advisor technology announcements, including:

Read the analysis about these announcements in this month’s column, and a discussion of more trends in advisor technology, including:

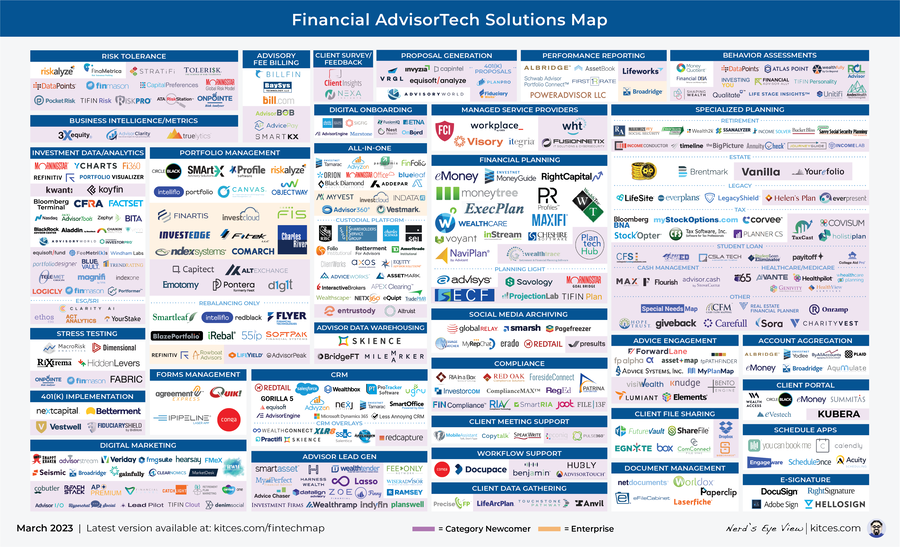

Be certain to read to the end, where we’ve provided an update to our popular “Financial AdvisorTech Solutions Map” and also added the changes to our AdvisorTech Directory.

AdvisorTech companies that want to submit their tech announcements for consideration in future issues, please send to TechNews@kitces.com.

In the initial days of financial planning software, the primary purpose of the technology was to show clients where they stood today, where they were going on their current trajectory, and the gap that existed between where they were heading and where they wanted to be. This usually provided an opportunity for advisors to sell a product — e.g., mutual funds, life insurance policies or even limited partnerships at the time — to fill that gap.

As financial advisors began to move away from product sales and more toward advice for its own sake, the tools evolved in kind. It was no longer just about demonstrating the current trajectory and the gap that the advisor and their product would fill. It was about how the client’s own real-time actions — like allocating their investments, saving for retirement and ultimately spending down their savings — would affect their financial future, and how changes in their own behavior could improve their outcomes. Reflecting this shift, financial planning software started to include tools like sliders that enabled advisors to make adjustments to plan scenarios on the fly and demonstrate the impact of certain actions. By illustrating the difference between a good and a bad trajectory, this provided a handy reminder of the value of the planner’s advice in helping the client avoid actions that would take them down the wrong path.

The other virtue of this approach was that it made financial planning significantly more engaging for clients. Now they could now see the effects of their prospective financial decisions in real time, understand the magnitude of impact that certain strategies would have, and hopefully be motivated to take action. The bad news, however, was that there was no easy way to see what the most impactful action would be. Short of testing out every possible combination of settings in the planning software, it was impossible to figure out what was the best combination of actions for optimizing a plan. So, for practical purposes, planning software worked best as a way to compare the outcome of a client’s current trajectory with a course of action that a client may have already been considering to determine its effect, or perhaps to evaluate a predetermined proposed recommendation or at most, a small handful of options but not as an engine to quickly and effectively figure out what the best recommendation should be.

Enter Conquest, which was founded by Mark Evans and launched in Canada in 2020. Evans founded one of the first and longest-standing financial planning platforms, NaviPlan, which he departed in 2011. Conquest’s key feature is what the company calls its Strategic Advice Manager, or SAM, which uses algorithms to process client data and reams of possible recommendations to suggest the client’s “next best financial decision” and remove the need for the financial planner to use trial and error to narrow down to the best strategy to recommend.

After being available only in Canada for its first three years of existence, Conquest is now preparing to expand into the U.S. market. In readying itself to do so, it recently raised C$24 million (about US$18 million) in Series A funding. Notably, BNY Mellon, which announced last fall that it would be integrating Conquest into its Pershing X tech platform, was included in the list of investors for this round, a put-your-money-where-your-mouth-is commitment that suggests Conquest may have a significant presence within Pershing X’s own emerging offering.

Innovative as it may be, though, Conquest will likely still have an uphill battle in finding much adoption in the U.S. market. The financial planning software space is a big but already crowded pond with a lot of fish. According to Kitces Research, 90% of advisors already use third-party comprehensive planning software. Most of the remaining 10% also already have a solution. It’s just proprietary to their firm or built in-house for themselves, with most of that market dominated by three main players (eMoney, MoneyGuide and RightCapital) and numerous smaller competitors jockeying for the remaining market share. This means short of new advisors joining the market for the first time, there’s very little in the way of untapped advisors who don’t already have an established financial planning software solution. Additionally, financial planning software has one of the highest satisfaction ratings of any technology category. According to the latest Kitces Research on Advisor Technology, barely more than 5% of financial advisors were even considering a software change in the next year. Almost 80% of those had already decided on the existing vendor they planned to go to. This means that not only must Conquest convince advisors that its platform is superior enough to be worth the pain of changing from one software provider to another, it must do so in an environment when most advisors are already generally happy with the provider they already have or have already decided on the known vendor they plan to pursue next.

Conquest’s main pitch to advisors appears to be about time savings. Instead of needing to drag sliders around to find the optimal action to improve the financial plan, Conquest analyzes many different data points and provides guidance to the advisor about where to focus first. By doing this, Conquest hopes to cut down the approximately 10 hours it takes for a financial advisor to do all the analysis and recommendation-crafting to prepare a financial plan, and/or provide a better and more focused real-time planning experience in front of the client.

However, it’s not clear how much time can realistically be saved during a financial plan construction process that still requires data gathering, input, preparing reports and presenting the plan to the client. The amount of time it takes for advisors to look at alternative scenarios and determine the best one — in between the input and preparation phases — is still just a small portion of the overall time it takes to create and deliver a financial plan. Furthermore, the 2022 Kitces Advisor Productivity Study found that advisors are increasingly looking not for faster and simpler planning tools but for ones that help them get deeper and more comprehensive to show value beyond what increasingly accessible consumer tools help clients do themselves. Simply put, saving time in the plan construction process is not actually a big driver of what’s leading advisors to consider and switch to new planning software.

Still, Conquest has to find some way to get a toehold in the crowded marketplace, and it seems to be making a large initial bet on its ability to do so via its go-to-market integration with the Pershing X platform. However, since Pershing X is itself a new platform seeking advisor adoption, it isn’t at all clear whether that will really be a viable way for Conquest to enter the space. Even for advisors who do adopt Pershing X, Conquest will still need to make the case for switching over from the financial planning software they were using already. In the end, the real question will remain whether a Strategic Advice Manager providing suggested recommendations to advisors so they don’t have to figure out the recommendations themselves is really compelling enough to get advisors to switch. Time will tell.

About 10 years ago, financial advisors started to apply the concept of mind mapping to financial planning. At its core, a mind map is about creating a single visualization that links together disparate concepts and ideas to create a picture of how that information connects as a whole (often, literally, a map of how the ideas bouncing around in our minds can be connected together with lines drawn to connect the key concepts). Ultimately, being able to see information collected in this more holistic way allows us to perceive it differently, and often more insightfully, than if all the individual pieces were on their own (a concept known in psychology as Gestalt).

Many industries have realized the benefits of mind mapping, and a number of tools like MindMeister, Coggle and Ayoa have come about to help professionals more quickly and easily create mind maps. In the context of financial advisors, however, mind mapping was slow to gain traction. While mind mapping is especially good at facilitating unstructured brainstorming, it isn’t necessarily as useful for following a structured, repeatable process such as that of gathering data and bringing it together to form a traditional financial plan. If advisors sat down each client with a blank whiteboard and proceeded to map out their entire financial lives, the results would look so different from one client to the next that it would be nearly impossible for the advisor to build a repeatable planning process to serve them all.

This was the case until Asset-Map was founded in 2013. Visually, it created something akin to a mind map of a client’s financial household, including investment and retirement accounts, bank accounts, real estate, debt, insurance policies, and even income and spending. However, it was fitted into a standardized template for each client that made it easier for advisors to have a structured process to gather and input information, while also creating a clear, comprehensive one-page visualization map of the client’s current financial situation.

Asset-Map also includes some basic tools for projecting and tracking progress toward client goals, so at least nominally fit it within the financial planning software category. In practice, Asset-Map’s early adopters tended to be advisors who didn’t necessarily want to go as deep into financial planning as more comprehensive software would allow, but still wanted an effective visualization of the client’s household situation in order to have more meaningful and immediate conversations about next steps and taking action. That approach has led to Asset-Map quietly accumulating a user base that it now reports to be in the thousands of advisors, aided by partnerships with organizations and vendors like FPA, Snappy Kraken and Schwab Intelligent Technologies.

In the latest indication of the steady demand for its financial visualization tools, Asset-Map announced in February that it has raised $6 million in a Series B funding round to expand its product engineering and sales and marketing teams as the company scales up for its next stage of growth. Notably, Asset-Map had previously only raised around $1.6 million of capital, meaning that much of its first decade of operations was essentially bootstrapped by its founder and a small round of early investors and supported primarily by the growth of its advisor user base paying for the software.

In other words, there has been a clear run of success for Asset-Map’s unique financial visualization offering, and more broadly for the increasingly hot category of advice engagement under which it more properly falls, as opposed to Planning Light software category to which it is sometimes ascribed. In fact, Asset-Map is arguably the leader in its emerging advice engagement category, finding a way to incorporate mind mapping in a more systematized, actionable way for advisors while keeping it clear and engaging for clients. In doing so, it has already recently spawned competing products, like Income Lab’s LifeHub and RightCapital’s Blueprint, that emulate its one-page financial visualization approach.

The new Series B capital will help Asset-Map continue to expand into more large advisor enterprises that have unique and specific customization needs from an engineering perspective, and require more sales and marketing efforts. Additionally, it will aid with Asset-Map’s international footprint. It is currently available in South Africa and the United Kingdom as well as the U.S., as notably advice engagement and financial visualizations are less reliant on individual country specifications than traditional financial planning software, which has to navigate different legal and tax environments from one locale to the next.

The question going forward, though, is where Asset-Map will fit relative to the traditional financial planning software landscape. Specifically, if more comprehensive financial planning tools encroach into its territory by adding one-page visualization on top of their existing capabilities (such as Income Lab and RightCapital have already done), will Asset-Map’s features continue to distinguish it from its competitors as a second or additional tool to use or will advisors begin to revert to a more all-in-one approach from their primary planning software platform? This raises further questions of whether Asset-Map can build a deeper moat around its financial visualizations and advice engagement that allow it to remain valuable as a stand-alone tool, whether it will need to build more comprehensive financial planning software to compete head-to-head with the legacy platforms building out their own visualization tools or if it will ultimately be acquired by another financial planning software provider that wants to integrate Asset-Map’s increasingly popular capabilities as its own.

The earliest iterations of financial planning software were built around creating “the plan.” This is a document created either with the goal of selling a financial product or convincing a prospective client to move their assets over to be managed by the advisor. In either case, the plan was typically a one-time deliverable presented at the beginning of the advisor-client relationship — at the point of sale for the product or rollover opportunity — and was rarely revisited after the initial sale.

As advisory relationships shifted from being product-focused to advice-focused, and as diversified asset-allocated portfolios became increasingly commoditized, financial planning grew to become more comprehensive to show greater value beyond the portfolio alone. It also became more ongoing to provide a greater value-add to retain clients over time. This meant that advisory firms needed more complex software to provide deeper planning capabilities and that the plans needed to be updated more regularly, e.g., on an annual or semiannual basis, to reflect the increased emphasis on monitoring, reviewing and renewing plans to retain ongoing clients.

However, in spite of the large-scale shift to more ongoing planning, the functionality of most legacy financial planning software platforms continues to be built around creating and delivering one-time plans or doing a one-time analysis to update an existing plan. With the software’s complexity, the requirements for data gathering, analysis and producing plan deliverables are such that it would be impractical to do a plan update more than once or twice per year. In reality, most clients’ financial situations don’t change frequently enough to even require a full plan update more than once per year anyway.

At the same time, many advisors are continuing to feel ever-increasing pressure to show value year-round to justify their ongoing fees. However, with most financial planning software being only really capable of annual plan updates, that leaves the question of what to do for the rest of the year. As a result, there is increasing demand for solutions that can fill these gaps, which has led to the emergence of the Advice Engagement category and tools like Elements that can fill in the time periods between new plan updates by keeping track of and providing meaningful feedback to clients regarding their financial health and other key metrics as they change and hopefully, grow, over time.

One slightly surprising new entrant into the advice engagement space is Wells Fargo, which announced this month that it has launched a new client-facing tool called LifeSync within its mobile app for clients of Wells Fargo Advisors and also its FiNet independent advisors. LifeSync combines features of traditional goal-based financial planning software like goal tracking and Monte Carlo analysis with ongoing monitoring of clients’ financial vitals. This includes net worth, portfolio performance, FICO scores and even Wells-Fargo-based credit card reward balances.

In other words, Wells Fargo, like other megafirms, is continuing to expand its focus on financial planning, but its new planning tools are less about building and delivering the plan and more about keeping clients engaged in the ongoing financial planning process as their goals change (which LifeSync occasionally prompts clients for updates on) and their financial health and progress toward their goals improve over time (which the app tracks and reports back to the client). All of which is tied into communication with the client’s advisor, since the app also reports this information back to the advisor and provides opportunities for clients to keep in touch.

For Wells Fargo specifically, launching an engagement tool like LifeSync could be seen as an attempt to boost customer loyalty after a series of high-profile scandals in its banking arm led to several years of declining advisor head counts and stagnation of assets under management. More broadly in the industry, however, it represents the continued shift toward more and deeper financial planning at even the biggest of mega wealth management firms. While LifeSync isn’t the deepest planning tool out there (does anyone really consider credit card reward points to be a vital financial metric?), it does serve to highlight that advice engagement — which has traditionally been the domain of boutique firms that offer high-touch year-round planning capabilities — can also be a viable tool for a megafirm like Wells Fargo to demonstrate the value of financial planning at scale to its many customers.

Behavioral finance is a segment of economics research that focuses on anomalies — situations where humans fail to act as the rational agents that economic models predict. These irrationalities often lead to investors making mistakes (e.g., overconcentrating their portfolios in certain asset classes or selling when markets are volatile) as a result of various behavioral biases, which leads to taking on excessive risks, achieving subpar returns or both.

To remediate these gaps, financial advisors have increasingly been seen as and have often marketed themselves as agents to counteract the common biases that lead to clients’ irrational financial behavior. To the extent that clients may struggle with these behavioral biases, financial advisors’ presumed expertise and objectivity can allow them to narrow or eliminate the behavior gap, that is, the difference between market returns and investors’ actual returns. By some estimates, the value added from behavioral coaching alone can cover many advisors’ entire fees and then some.

However, there’s much more to a person’s financial habits than a series of investment-related cognitive biases. A growing portion of the research on money and financial behavior is coming not from the economics discipline, but rather from the field of psychology. This financial psychology research explores our attitudes, values and relationships with money, how we talk about money and how we make decisions around money. And unlike behavioral finance, which has a relatively narrow range of applications around financial decision-making, financial psychology can be applied broadly to many aspects of an individual’s financial life to help them achieve a better overall sense of financial well-being.

Coincidentally, or perhaps not, given rising consumer demand for more holistic financial guidance, the growth of the field of money psychology has occurred in tandem with the rise of more comprehensive financial planning as an alternative to investment-centric financial advice. In addition to helping their clients counteract behavioral finance biases in investing, many advisors now position themselves as guides in helping their clients explore and develop their financial psychology. This covers everything from understanding clients’ money scripts and money histories, to their anxieties around financial risk and change and the money dynamics between household members. All of which can impact a client’s ability to spend within their means, save for retirement and even visualize the kind of ideal life they want to live.

With the growing recognition that a person’s beliefs and attitudes about money can have a real impact beyond their investing behavior, financial psychology has become an incredibly hot topic for financial advisors. As demand has grown for tools to give advisors insights into their clients’ money psychology and support conversations around improving clients’ behaviors to enhance their financial well-being, behavioral assessment solutions like those from DataPoints, DNA Behavior and Shaping Wealth have become integrated into many advisors’ onboarding processes.

Now Orion has stepped into the financial psychology space with the launch of a new tool called BeFi20, a 20-question assessment that builds an individualized financial persona for each client. The questionnaire can be sent to both members of a couple, to find out how financially aligned they are, understand where they may have gaps in their money attitudes and provide guidance to advisors in how to facilitate conversations around those gaps between the couple.

Interestingly, Orion framed the rollout of BeFi20 around the release of its Couples and Money Survey showing money to be a significant source of friction in couples’ relationships, particularly among millennials. Couples can experience marital strife around money issues — even when they have significant income and net worth — because they are misaligned on how to use and save their money. For instance, one spouse might be a spender while the other is a saver, or the spouses might disagree on whether to combine their finances, or one spouse might hide assets or purchases from the other. Having a tool like BeFi20 can, at least in theory, help provide a more structured way to unearth the underlying money attitudes that might lead to conflict between spouses, so advisors at the least know what they need to navigate, and ideally can help clients work through their individual and combined money issues.

The caveat, though, is that in practice these money psychology conversations can be very challenging. Spousal conflicts often revolve around deep-seated differences in money beliefs, a type of conversation that few advisors are fully trained (as psychologists and couples’ therapists) to navigate, and one where couples who really want to engage with someone about their marital issues may be more likely talk to a couple’s therapist rather than a financial advisor in the first place. In addition, the somewhat harsh reality is that advisors generally aren’t compensated for those often time-consuming conversations, either. After all, therapists might engage in weekly or monthly therapy sessions to focus solely on tackling these issues for a couple facing challenges. Financial advisors often meet no more than once or twice a year and usually have an agenda packed full of other financial planning and investment topics. This provides little space for the advisor to have much noticeable impact on working through clients’ underlying financial disagreements.

Advisors who are sensitive to this fact generally don’t rely on assessments or tools to better structure the conversation. They simply don’t open the door to the conversation to begin with, knowing they may not have the training nor the time to bring a potentially very messy couples’ issue to a meaningful conclusion. Advisors who are willing to have those conversations may be more willing to pay for — and likely already use — a more robust stand-alone assessment tool like DataPoints. The adoption of BeFi20 might be limited to advisors who see it as a prospecting tool and interesting conversation starter, but who might not want to go that deeply into exploring their clients’ financial psychology. Ironically, there’s still a risk that BeFi20 is too deep of an assessment and still delves further into couples’ marital issues than the “just getting the conversation going” advisor really wanted to go, especially if being done with a prospect.

Ultimately, the key point is that while behavioral finance has been popular as an industry buzzword, it’s still not really clear just how far beyond the investment-centric roots of behavioral finance the typical financial advisor will really be willing to tread. Even those who consider themselves comprehensive financial advisors aren’t necessarily getting paid to invest the time it takes to have a meaningful impact as a financial therapist, nor are most advisors necessarily really being hired by the clients to do so. With BeFi20, the question is whether knowing clients’ money personas at the depth that BeFi20 measures really makes it easier to resolve money-related conflicts or whether it’s inviting advisors to start a conversation that most aren’t really comfortable to start in the first place.

In the days before electronic written communication existed the way we know and live it today, compliance review for financial advisor communication was rather limited. Written client correspondence, in those days consisting of physical letters and one-to-many advertisements, would need to be archived and reviewed. Most of the actual communication with clients took place either by picking up the phone or by meeting face-to-face — for which there was no feasible way for an advisor’s compliance department to capture, much less review, each and every conversation and recommendation given to the client.

However, with the advent of email in particular, many conversations that had once taken place over the phone or in person were now happening in written form. This meant that they too needed to be archived and reviewed for compliance purposes (greatly increasing the compliance burden from the sheer volume of communication to review now). With the arrival of social media in the early 2000s, the volume of written communication increased exponentially because what previously might have been one email several paragraphs long might now be two, five or 10-plus small social media posts. The pain was further amplified given that email was generally classified as correspondence, which needed only to be archived and reviewed after it was sent. However, social media was considered to be an advertisement because it went one-to-many to prospects as well, which meant each post and snippet individually needed to be approved before it was posted.

As a result, advisors at larger firms (and particularly at the huge wirehouses like Merrill Lynch and Morgan Stanley) fell behind smaller advisory firms in social media and electronic communication. A solo advisor or small firm could easily create, approve, and archive messages since there might only be one or two advisors to monitor. In many cases, the advisor to be reviewed was also the chief compliance officer for the firm itself. For a firm with thousands of advisors there was no way to pre-review and approve an immense volume of small social media snippets at that scale. Even if each advisor posted just a handful of times per week, that would still add up to millions of social media posts each year requiring compliance sign-off. For advisors at those firms, social media activity was generally restricted to sharing a few preapproved messages. This ultimately limited those advisors’ ability to communicate as individuals — arguably the whole point of advertising on social media to begin with.

Today, video seems to be the next big wave in electronic communication. Tools like Loom and BombBomb allow advisors to quickly create and share videos with their clients for purposes ranging from answering questions in less time than it takes to write an email, to demonstrating how to use a particular technology tool and sending video newsletters in lieu of the traditional email or print version. However, a similar gap between smaller and larger advisory firms’ ability to supervise video communication for compliance began to emerge, as was seen in the past for social media, leaving it an open question as to whether bigger firms would fall behind in the video race as well.

In this context, it’s notable that Merrill Lynch, one of the largest wirehouse firms with over 13,000 advisors, has launched Video Pro, a turnkey video platform that expedites the compliance oversight process, making it possible for their advisors to create a short video, get it through compliance and have it posted all within a day — something that wouldn’t have seemed feasible given the sheer number of advisors at the firm.

The key to the scalability of Video Pro appears to be a library of preapproved content scripts that can be read verbatim or edited for a more personal touch, with an extra — but extra-expedited — compliance sign-off required for the latter. The videos, which can only be up to 50 seconds in length, can then be shot, approved by compliance and posted to LinkedIn (to which Merrill has made a big commitment as its social media platform of choice for marketing), uploaded to the advisor’s website or sent via email.

Relative to the unusually high volume of flow that can emerge when firms open the door to social media, it’s notable that large firms like Merrill are arguably better positioned to support video in particular, as the length of videos tend to be short enough to be conducive to quick review but still long enough to put together that most advisors won’t be creating them with a lot of frequency. They’re more likely to substitute for a select letter to a client or a newsletter broadcast, not the cadence of many-times-per-day social media posts.

The fact that Merrill is even attempting to build a tool for creating video content with quick compliance review counts as a feat given the struggles of large enterprise firms to deal with digital communications because of the difficulty of managing the compliance burden at scale to the lowest common denominator of advisor who might run afoul of the rules.

Notably, even many firms that are smaller than Merrill don’t yet have this ability. Though many solo and small-ensemble firms have implemented video communication using tools like Loom and BombBomb, the tools simply don’t exist yet to archive and review video content at scale as they do for written communication.

This serves to highlight a gap in compliance review solutions for video in midsize to large independent advisory enterprises. After all, a solo advisor can likely still get along by downloading each video file and saving it to a client’s folder on the cloud (and then reviewing it themselves, as the advisor who is also their own chief compliance officer), but that isn’t an acceptable solution when there are dozens or hundreds of advisors to supervise.

Unless the compliance department can manage to build an in-house platform like Merrill did, these firms might have difficulty with effectively using video in their client communications without a built-in compliance oversight function. This is a situation that may be to their detriment given how video has been shown to be an effective communication tool in the post-Covid era, and not just for younger clients. It remains to be seen where the independent compliance technology providers will go on this front, but for now it appears that despite the typical view that megafirms lag in technology, Merrill has leapfrogged the independents in the race to scale compliant video content distribution for financial advisors.

NEW CHATGPT ERA THREATENS ADVISOR SUPPORT STAFF (NOT ADVISORS THEMSELVES)

As pervasive as technology is in financial planning today, it wasn’t all that long ago that the technology available to financial advisors was fairly minimal. The first CFP graduating class in 1973 predated the first widely available personal computers. There are still advisors practicing today who can remember when planning was done with no more than an HP-12C calculator and a notepad. Many more likely built their first plans using their own handcrafted Excel spreadsheets to do basic financial projections for clients.

In the 50 years since that initial CFP cohort, the processing power of computer chips has grown by a factor of roughly 10 million. The resulting explosion in technology has completely changed the way financial advisors serve clients, run their businesses and market themselves. Yet the fundamental nature of financial advice has changed remarkably little since the early days, despite the 10,000,000X increase in computing power. At its core, it’s still about building a relationship of trust. The client must feel heard and understood before they’re willing to take the advice, must be able to vet whether the advice is credible and will often need a partner to whom they feel accountable to follow through on and implement the advice. These are all remarkably human conversation and relationship dynamics.

Which brings us to the recent emergence of ChatGPT. Artificial intelligence startup OpenAI’s text-based conversational interaction tool launched in November 2022 and has since taken the world by storm. Much of the fascination reflects the sheer novelty of ChatGPT. Here is a chatbot that can answer questions, converse and even argue with users, all while sounding plausibly human-like in its conversation (albeit with a fair amount of gawking at some of the situations where conversations with ChatGPT has still veered into unexpected, hilarious or disturbing directions).

But underneath all that there is also an undercurrent of anxiety about the implications of a future where AI technology becomes commonplace. In academia, professors worry that students will hand in ChatGPT-written term papers. Journalists fear cost-cutting media companies will replace human-written content with articles produced by AI (a fear that does appear to have some validity, although Kitces.com has no plans to debut any ChatGPT-written 5,000-word financial planning posts yet). Financial advisors may naturally wonder if, in a world where AI is sophisticated enough to give personalized feedback to a user’s financial questions, the jobs of human advisors will be in jeopardy as well. Simply put, if ChatGPT can have increasingly human-style conversations, is there a point where it will actually begin to replace advisor-client conversations?

However, to believe that AI will render financial advisors obsolete is to ignore all previous evidence that prior technological advances have served not to replace but rather to support human advisors. Consider what happened a decade ago when robo-advisors came onto the scene, offering diversified asset-allocated portfolios with rock-bottom fees and stirring up similar concerns about disrupting human financial advice. In reality, the only advisors that the robo-advisors disrupted were those who focused solely on product sales and arguably weren’t really advisors to begin with, despite their use of the title. Meanwhile, advisors who actually offered comprehensive planning thrived amid the competition from robos, largely because robo-technology also became widely integrated into advisors’ investment management platforms. This reduced the time they needed to spend on manual, repeatable portfolio management tasks and allowed them to spend more time going deeper into financial planning to provide even more value to their clients, producing a steady rise in the average revenue/client for financial advisors over the past decade.

Similarly, the advisors that AI technology will replace are likely those who aren’t providing very high-quality advice to begin with. Currently the advice that ChatGPT is capable of rendering ranges from generally accurate yet not specific enough to be actionable, to very specific but alarmingly unreliable — not a very high bar for human advisors to hurdle. This, in turn, isn’t exactly a new problem, The similarly wide range of advice found in a Google search is why search engines and the internet didn’t replace financial advisors, either, as consumers using those tools also had to determine which was a credible website that could be relied upon or not (or instead simply decide who was a credible advisor to rely upon, and let them figure out which computer-provided answers were accurate [or not).

This isn’t to say that AI tools like ChatGPT won’t have impact for financial advisors. Instead, it seems more likely that the practical applications will, similar to the rise of computers and the internet and the robo movement, be focused more on automating away an increasingly sophisticated series of otherwise manual and repeatable tasks, which can free up time for advisors to go even deeper into planning and advice in their own client conversations.

What specifically are those tasks that tools like ChatGPT could eventually automate? Being a language-based model, the first and most obvious use case is in streamlining and improving written communication with clients, and in fact this is where tech providers are already starting to integrate AI into their tools. For instance, Orion recently announced a ChatGPT integration with its Redtail Speak client texting platform, which will generate suggested responses to client inquiries via text message. Another example is Pulse360’s AI Writer tool, which can convert an advisor’s notes or suggestions into client-ready text that can be dropped into an email. There are myriad ways in which an advisor could use ChatGPT to quickly generate marketing content like blog posts and newsletters, which the advisor could tweak with their own personal flourishes but otherwise rely on the AI to do the bulk of the writing.

On a higher level, AI could also eventually be used for automating tasks involving multiple steps across different software platforms. For instance, an AI tool could conceivably capture a recording of a client meeting conducted via Zoom, then not just transcribe the words of the meeting itself, but automatically summarize the key points to be logged in the advisor’s CRM. It can flag any conversation topics potentially needing compliance review, email a meeting summary and takeaways to the client, and create and assign the appropriate follow-up tasks for other members of the advisory team — essentially automating the entire post-meeting workflow (the first parts of which technology provider Fireflies.ai is already doing).

At an even higher level, AI could be used to further streamline parts of the financial planning process itself. The steps of collecting client data, feeding that information into financial planning software and turning the software’s output (or that of multiple pieces of software, both comprehensive and for specialized planning) into a client-friendly report are begging for an AI solution to streamline and meaningfully reduce the time it takes to produce a financial plan.

What all of these improvements have in common is the potential to reduce the back-office, client service and even middle-office paraplanner support needed for advisors to do what they do. This is good for advisory firms and their owners, who will enjoy more revenue per employee productivity, but — as with previous technological developments — perhaps not so good for the firms’ support staff. Notably, while the bar may rise, there will always continue to be some layer of jobs that are more advanced than what technology can automate but are still worthwhile for advisors to delegate to others, if only because doing so allows advisors to raise themselves to higher-level tasks, too.

Ultimately, what clients value most in a human advisor are the abilities to make the client feel heard and understood, to develop a personal connection of trust with the client, and to be an accountability partner that helps clients actually implement their recommendations and change their behavior for the better. Although some research has suggested that people are capable of forming bonds with digital conversational agents, there’s a wide gulf between ChatGPT’s current capabilities and the type of emotional and decision-making support that a human advisor is able to provide.

So while there’s no danger of advisors being replaced by AI in the near future (which even ChatGPT will tell you unless that’s just what it wants us to think), advisors would be well served to stay tuned for further developments on the capabilities of AI to support advisors, automate back- and middle-office tasks, and create space for more meaningful client conversations in the years to come.

In the meantime, we’ve rolled out a beta version of our new AdvisorTech Directory, along with making updates to the latest version of our Financial AdvisorTech Solutions Map with several new companies, including highlights of the Category Newcomers in each area to highlight new fintech innovation.

So what do you think? Do Conquest’s automated next-best decision suggestions make it worth considering a switch from your current financial planning software? Would a solution like Orion’s BeFi20 help you better engage with clients who are misaligned with their spouses on matters of money psychology, or lead you to open conversational doors you don’t actually want to open with your client couples? How do you see AI shaping the way you advise and serve clients in the future?

[More on Fintech News Today]

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter @MichaelKitces.

Ben Henry-Moreland is senior financial planning nerd at Kitces.com, where he researches and writes for the Nerd’s Eye View blog. In addition to his work at Kitces.com, Ben serves clients at his RIA firm, Freelance Financial Planning.

Former Northwestern Mutual advisors join firm for independence.

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Canada, China among nations to react to president-elect's comments.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound