Part of the SEC’s mandate is to regulate the activities of Registered Investment Advisers (RIAs). This involves ensuring that advisors adhere to the SEC Custody Rule under the Investment Advisers Act of 1940, specifically Rule 206(4)-2.

In a nutshell, the Custody Rules define an RIA’s responsibilities in relation to the holding of their clients’ assets.

So, what is the Custody Rule? What are the SEC Custody Rule requirements? And what are the SEC Custody Rule proposals? For this article, we delve into the important aspects of custody rules and cover its proposed amendments.

The SEC custody rule applies to RIAs and how their clients’ assets are held. The rules require that:

The custody rule is one that allows RIAs to hold client assets and securities in a separate account for each client. The account must be under that client’s name or in an account under the advisor’s name. Should any funds be held by the advisor, they must be named as an agent or trustee for their clients.

In simpler terms, the custody rule requires that all investment advisers and similar entities keep client securities and funds safe while those assets are in the adviser’s possession.

An investment advisor, trader or broker must keep their client’s assets separate and apart from their own. The financial advisor cannot mix or comingle their clients’ money with theirs or tap into it for the firm’s use.

There will be other changes to the SEC custody rule that would expand its scope. One of the most significant changes would extend the rule to include a broader range of assets.

The amendments now have the following assets covered by the custody rule:

The amendments now also require qualified custodians to keep possession or control of client assets, as stipulated in a written agreement with an RIA.

The main purpose of the SEC amendments is to enhance protections for client assets while reducing burdens on advisors that have custody of those assets.

The custody rule is also designed to:

For example, a brokerage cannot use client assets to make its own investments and put that money at risk. No advisor can use client money as operating funds either, similarly putting that money at risk if the firm goes out of business.

A real-world example of this is the case of now-defunct cryptocurrency exchange FTX, where investigators found evidence of theft and comingling of assets which the custody rule prohibits. This case prompted a reevaluation of the rules on cryptocurrency and similar assets.

The proposed changes to the custody rule seem beneficial, even necessary at first glance, but this short video from the president of the Investment Advisers Association suggests otherwise. It appears that the sweeping changes to the custody rule were created without considering their impact:

An advisor is said to have custody if they hold, directly or indirectly, client funds or securities. They are also deemed to have custody if they have any authority to obtain possession of these funds or securities. The custody rule now extends to a broader range of assets.

Recent amendments to the custody rules revised the definition of custody. Custody now includes instances where an adviser’s related person has custody of client assets in connection with their advisory services. For example, if an RIA’s affiliated broker-dealer holds client assets as a qualified custodian as part of their advisory services, then the adviser is considered to have custody of those assets as well.

These amendments are part of the SEC’s Proposed Safeguarding Rules as outlined in this fact sheet.

According to the Investment Advisers Act, RIAs must use a “qualified custodian” to hold their clients’ assets. The US Securities and Exchange Commission deems the following as qualified custodians:

For Foreign Financial Institutions to qualify as custodians, they must maintain client assets separately from their own.

Regardless of the type of entity, the RIA custodian’s primary role is handling transactions. They can also handle bookkeeping and offer other specialized services.

While RIA custodians can work with investment advisory firms, they can also deal directly with individual investors. For instance, a custodian can hold assets on behalf of one or more RIAs, while also offering brokerage accounts or retirement accounts to their own clients.

Technically, no, the SEC does not directly regulate custodians. But due to the Proposed Safeguarding Rule as of early last year, additional “guardrails” may be set. These added guardrails are required of any type of financial institution that acts as a qualified custodian, across all asset classes.

Some advisers may notice that some of these requirements are consistent with standards of care that already apply to qualified custodians or have become market practice.

The Proposed Rule now requires the advisor to get “reasonable assurances” in writing from each qualified custodian. The qualified custodian will provide certain client-enumerated safeguards, which are as follows:

When discharging its custodial duties, the qualified custodian will exercise due care in accordance with reasonable standards. It will also implement appropriate measures to safeguard client assets.

Any sub-custodial, securities depository or other similar arrangement regarding the client’s assets does not excuse any of the qualified custodian’s obligations to the client.

The qualified custodian will ensure that insurance arrangements are in place to adequately protect the client, regardless of the difficulty in obtaining them for certain asset classes (like cryptocurrency assets, for example).

The qualified custodian agrees to compensate the client against the risk of loss of the client’s assets. This happens in the event of the qualified custodian’s negligence, recklessness, or willful misconduct.

The qualified custodian is obliged to hold client assets in a custodial account, distinct and separate from the qualified custodian’s proprietary assets and liabilities.

The qualified custodian will not subject client assets to any right, charge, security interest, lien, or claim for itself or for its related persons or creditors. The only exception to this rule is if the client agrees to such an arrangement.

The SEC understands that there may be unusual situations where the assets might be difficult, if not impossible, for a qualified custodian to safekeep or maintain. This can be cases where the assets are physical assets or privately offered securities.

The Proposed Rule provides an exception to maintain these client assets with a qualified custodian if:

To apply this exception, the advisor must also have a written agreement with an independent public accountant. The accountant must be informed of any purchase, sale, or transfer of beneficial ownership of these assets within one business day.

Should the independent public accountant find any discrepancy, they should notify the SEC within one business day of its discovery.

Each privately offered security or physical asset not maintained with a qualified custodian must be verified in either a surprise examination or audit.

The surprise examination is a requirement of the SEC Custody Rule 206(4)-2. The rule requires that advisers have a yearly “surprise examination” done by an independent public accountant. They may also engage the services of an accounting firm registered with the Public Company Accounting Oversight Board (PCAOB).

This examination of funds and securities must be conducted annually, on random dates chosen by the independent public accountant or accounting firm. The purpose of the surprise examination is twofold:

The surprise examination is completed by performing the following steps:

For the investment advisor to pass the audit, the report should say that they complied with Rule 206(4)-2 in all material aspects. The period of compliance covers the examination date and during the period since the last surprise examination.

Custodians and depositories both provide asset-holding services. The main difference lies in the extent of their responsibility over such assets. A depository usually has legal ownership and controlling power over the assets, while custodians typically do not.

Depositories have the added duties of performing asset management. They must maintain, issue, buy, and sell assets and securities in their care according to legal and regulatory guidelines. On the other hand, custodians only do so on the instructions of investors.

In terms of loss, depositories are largely responsible for any losses incurred from investment activities.

As for custodians, they are only expected to ensure that trades push through and are only liable for general losses, such as damage, theft, or negligence.

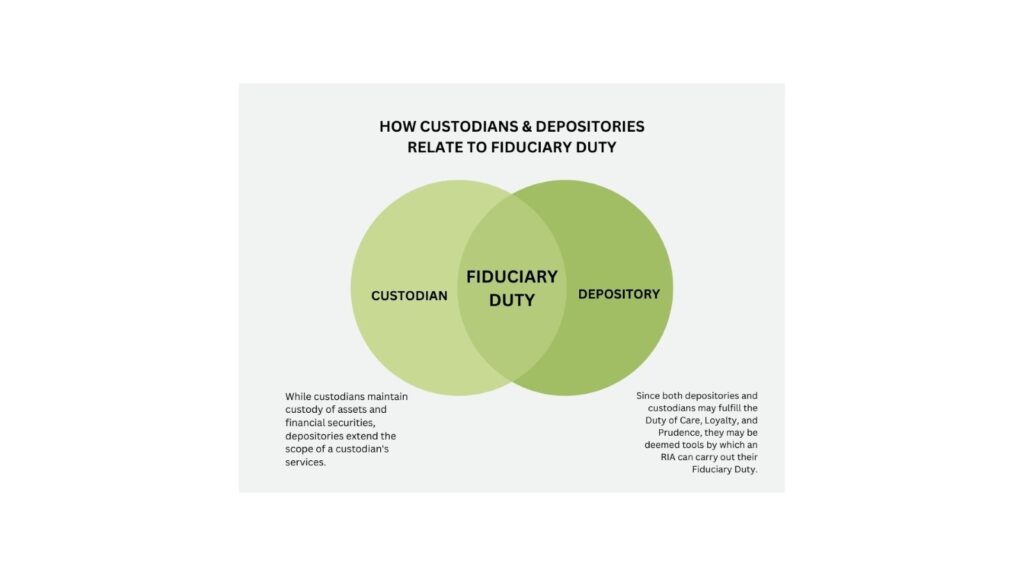

While custodians maintain custody of assets and financial securities, depositories extend the scope of a custodian's services.

A securities depository that stores financial securities allows for book-entry transfers of those assets and clearing and settlements.

What both entities have in common is that they can be used as tools for an RIA to carry out their fiduciary duties to clients.

The proposed amendments to the SEC’s custody rules were first drafted in February of 2023, but comments were reopened in May of that year. Since then, many prominent investors’ groups have voiced their opinions, claiming that the proposed amendments, if passed, may do more harm than good.

As of this writing, the Proposed Safeguarding Rules have not been officially implemented pending more reviews and discussions between the US SEC and several investors’ groups. It is unknown if these proposed rules will pass or go through a round of revisions.

Be sure to keep your eyes on this space for more RIA-related topics for a wealth of information to support you in your career.

Relationships are key to our business but advisors are often slow to engage in specific activities designed to foster them.

Whichever path you go down, act now while you're still in control.

Pro-bitcoin professionals, however, say the cryptocurrency has ushered in change.

“LPL has evolved significantly over the last decade and still wants to scale up,” says one industry executive.

Survey findings from the Nationwide Retirement Institute offers pearls of planning wisdom from 60- to 65-year-olds, as well as insights into concerns.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound