The bond market is doubling down on the prospect of a U.S. recession after Federal Reserve Chair Jerome Powell warned of a return to bigger interest-rate hikes to cool inflation and the economy.

As swaps traders priced in around a full percentage point of Fed hikes over the next four meetings, the yield on two-year Treasury notes touched 5.08% on Wednesday, its highest level since 2007. Critically, longer-dated yields remained in check, with the 10-year rate under 4% and the yield on 30-year bonds lower.

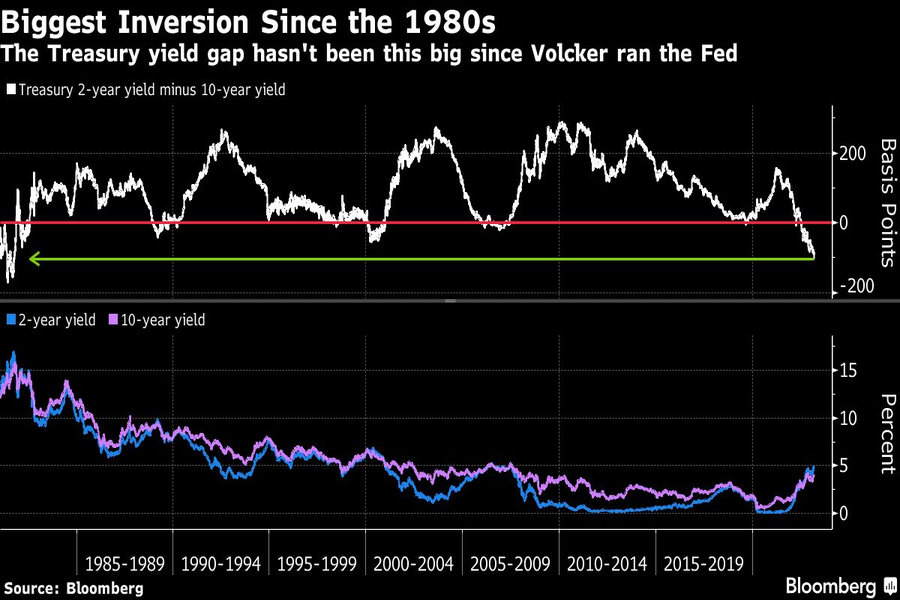

As a result, the closely-watched spread between 2- and 10-year yields this week showed a discount larger than a percentage point for the first time since 1981, when then-Fed Chair Paul Volcker was engineering hikes that broke the back of double-digit inflation at the cost of a lengthy recession. A similar dynamic is unfolding now, according to Ken Griffin, the chief executive officer and founder of hedge fund giant Citadel.

“We have the setup for a recession unfolding” as the Fed responds to inflation, Griffin said in an interview in Palm Beach, Florida.

Longer-dated Treasury yields have failed to keep pace with the surging two-year benchmark since July, creating a curve inversion that over the decades has amassed a record of anticipating recessions in the wake of aggressive Fed-tightening campaigns.

In general, such inversions preceded economic downturns by 12 to 18 months. The odds of another occurrence are intensifying after Powell’s comments indicate he is open to reverting to half-point rate hikes in response to resilient economic data. The Fed’s quarter-point hike on Feb. 1 was the smallest since the early days of the current cycle.

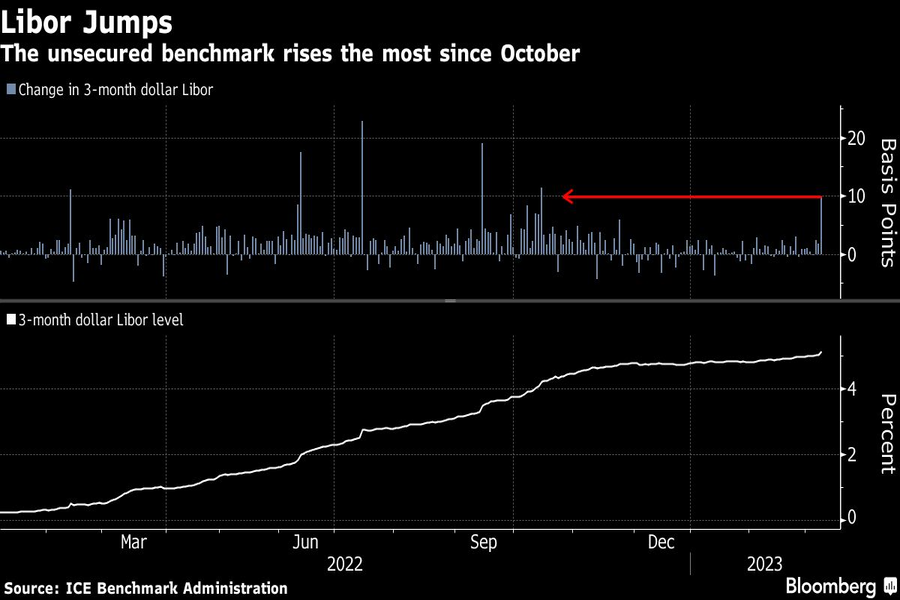

Traders upgraded the odds of a half-point rate increase on March 22 from about one-in-four to around two-in-three on Tuesday, raising the stakes for February employment data set to be released on Friday, and the consumer price index in around a week’s time. The three-month London interbank offered rate for dollars, a key benchmark, also surged on the back of front-end moves, leaping on Wednesday by nearly 10 basis points, the most since October.

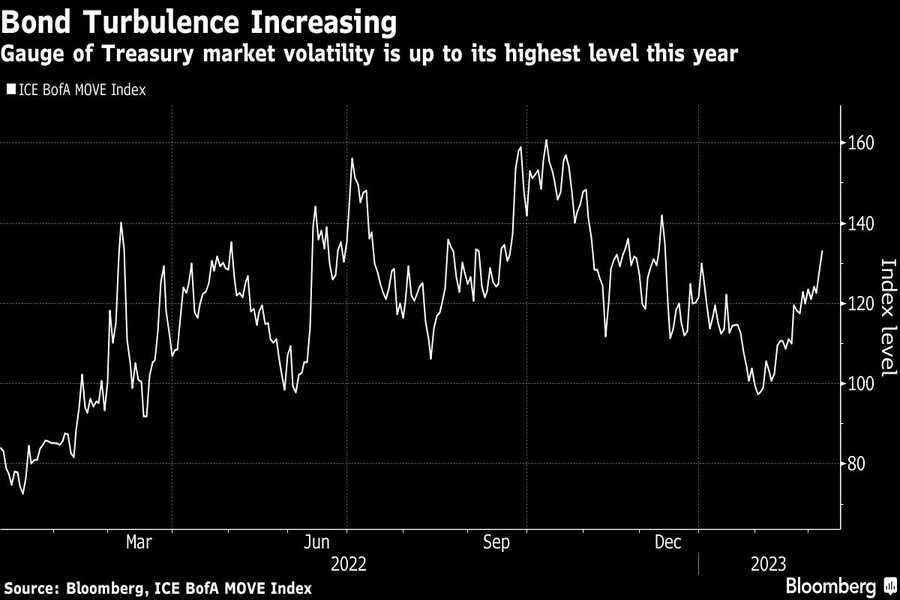

“Rate volatility will be with us until the Fed is really done,” said George Goncalves, head of U.S. macro strategy at MUFG. “Higher vol means you have to derisk and put more of a risk premia back into credit and equities.”

U.S. stocks extended the decline they’ve suffered over the past month, with the S&P 500 Index notching a 1.5% drop on Tuesday, its biggest in two weeks. It regained some ground in Wednesday trading. Hopes that the Fed might be near the end of its tightening cycle had boosted the gauge by over 6% in January.

Meanwhile the dollar, which tends to benefit from both elevated short-end interest rates and a bid for safety when times are tough, also surged higher Tuesday, with a Bloomberg gauge rising to its highest level since early January. Some of that move also reversed Wednesday.

“It is hard to deny the hawkishness of the statement and the message that markets took away,” strategists at NatWest Markets wrote in a note to clients Tuesday. Powell “firmly opened the door” for a return to 50-basis-point moves, although he emphasized the importance of upcoming data releases, which are “likely to be high vol events,” according to strategists Jan Nevruzi, John Briggs and Brian Daingerfield.

Powell told members of Congress on Tuesday that there are “two or three more very important data releases to analyze” ahead of the March deliberations, and “all of that will go into making the decision.” On Wednesday, testifying before lawmakers again, he stressed that “no decision has been made.”

The shift in messaging spurred some investors to give extra weight to the idea of the Fed even taking its rate to 6%. BlackRock Inc. and Schroders Plc are among those who are weighing in on the debate of what will happen if U.S. rates peak at that higher mark.

Also in March, Fed policymakers are set to release updated quarterly forecasts for where officials see interest rates going, also known as the dot plot. In December, the median projection was for a peak of around 5.1% and a long-run neutral rate of 2.6%.

Some investors think a recession can be averted even as growth slows. Either way, longer-dated Treasuries are viewed as a viable shelter with the Fed still raising rates.

Short-maturity yields are the “most vulnerable to repricing higher,” especially if wage growth resumes rising, favoring a half-point rate increase, said Ed Al-Hussainy, rates strategist at Columbia Threadneedle Investments. That will drive “more flattening pressure on the curve.”

Former Northwestern Mutual advisors join firm for independence.

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Canada, China among nations to react to president-elect's comments.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound