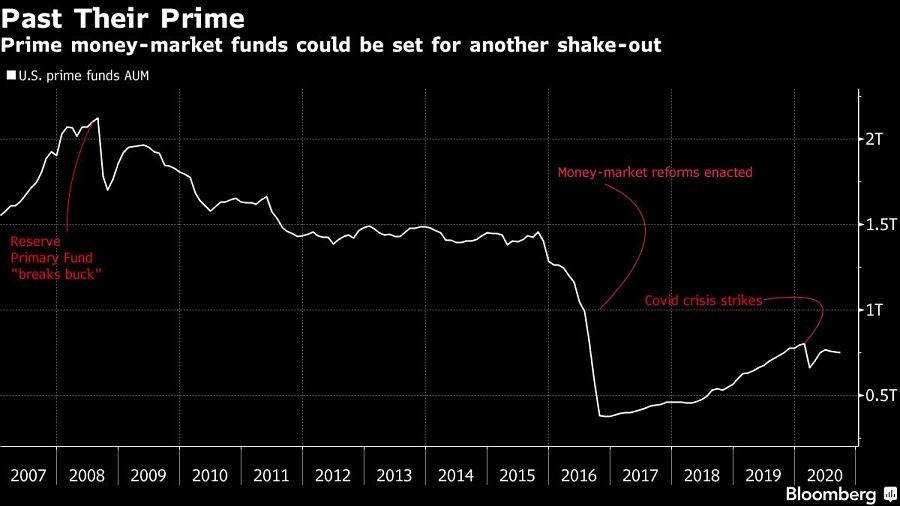

A $750 billion industry still struggling to bounce back from the last crisis is cracking under the Federal Reserve’s lower-for-longer mantra on U.S. interest rates.

Prime money-market funds -- a long-time favorite for anyone seeking a cash-like investment with a little extra yield -- are facing an existential challenge, just four years after a regulatory overhaul to restore confidence in the wake of the global financial crisis. Assets in these vehicles dropped 20% in just six weeks earlier this year, spurring talk of new reforms. But some of the industry’s leaders are opting for another solution: Shutting them down.

Vanguard Group, the world’s second-largest asset manager, is converting a $125 billion fund to buy government debt rather than the short-term corporate notes it’s invested in for decades, and Northern Trust Corp. and Fidelity Investments have recently axed funds with a similar focus altogether. The decisions entrench a prolonged decline for prime funds, and could hurt a market that thousands of companies rely on for funding.

The strategies are collateral damage from the Fed’s aggressive approach to suppressing rates for years to come. The realization that these funds, which are supposed to provide an edge over more conservative alternatives, aren’t going to get much more attractive any time soon is a grim prospect for investors who must often stomach limits on redemptions -- known as gates -- to buy them. Asset managers are in turn finding their fees increasingly difficult to justify.

“We’re anticipating a very extended period at the zero lower bound -- that’s brutal for money funds,” said BMO Capital Markets rates strategist Jon Hill. “What’s the argument for going into a prime fund, which could get gated and which is less liquid than being in Treasury bills and repo, if you’re only going to pick up a few basis points on yield?”

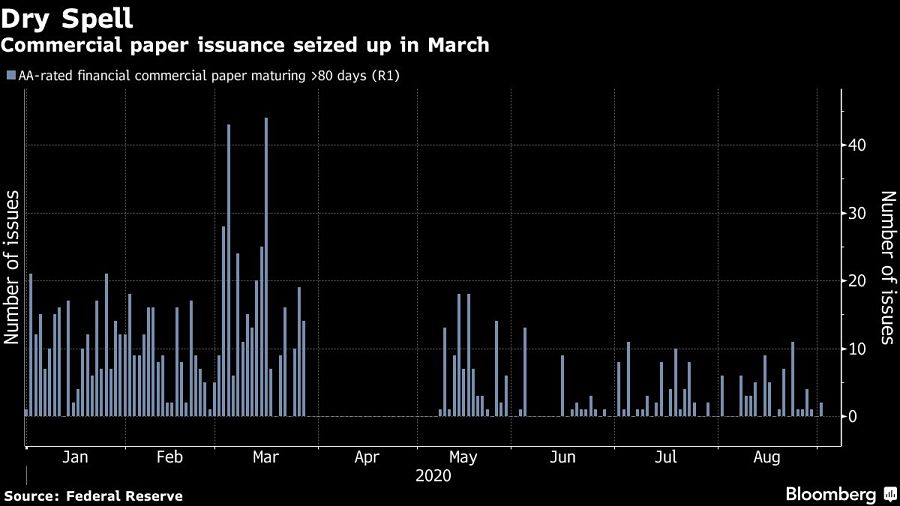

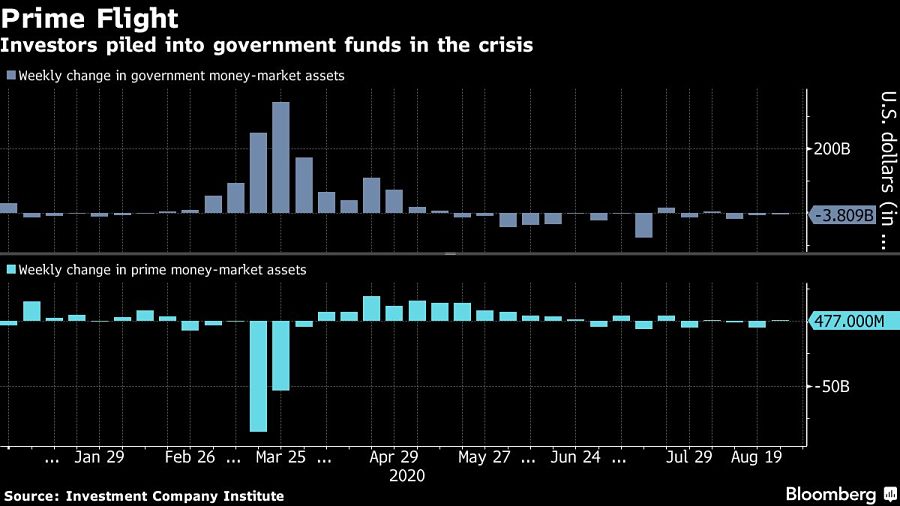

As the pandemic crushed economic activity and wracked global markets in March, prime fund investors moved money as fast as they could into government money-market funds -- considered the safest of havens because they’re limited to short-term government securities and related secured lending markets. Prime funds lost more than $150 billion of assets to withdrawals between late February and early April; as a cash-like product with credit exposure, these funds are uniquely vulnerable to runs in a crisis.

That led to paralysis in the market for so-called commercial paper -- IOUs issued by companies to meet short-term funding needs, such as payroll -- as prime funds that typically buy this debt became sellers. The knock-on effects contributed to a surge in Libor, a benchmark rate for lending between banks that underpins trillions of dollars of corporate and consumer loans, prompting the Fed to take emergency action.

For some, it was all scarily reminiscent of the cataclysm of September 2008, when an investment in Lehman Brothers paper caused a prime fund’s share price to fall below $1 and “break the buck.” That event sparked runs on money-market funds that then managed about $3.5 trillion, spilled into volatility across global markets -- and spurred sweeping reforms.

The rules, which took effect in 2016, included a separation of retail and institutional investments, the introduction of gates to prevent mass redemptions, and abolition of the traditional stable $1 pricing for shares, in favor of a floating net asset value. While the latest turmoil for money-market funds fell far short of 2008’s mayhem, the reemergence of fears around redemptions suggests another overhaul is likely.

“We expect an additional round of regulatory reform,” said Greg Fayvilevich, a senior director at Fitch Ratings. He expects regulators will focus on the liquidity fees and gates feature, as “sensitivity around that liquidity threshold has made runs on money funds more likely.” The additional costs associated with another possible round of rule changes might be among factors leading to more fund closures, he said.

Several fund managers including T. Rowe Price Group Inc. and Federated Hermes Inc. have already waived the fees they typically charge prime-fund investors in an effort to preserve income for clients, and further costs would make the business even less appealing.

BlackRock Inc. wants to create a new platform to trade commercial paper to bolster the liquidity of these holdings. That would leave prime funds less reliant on skittish secondary markets and potentially strained dealer balance sheets, according to Deborah Cunningham, chief investment officer for global liquidity markets at Federated Hermes in Pittsburgh.

Federated is among those still committed to prime funds, which have won back a chunk of institutional assets lost during the March carnage, even as many retail investors stay away. “People continue to want choice, so I think that they’re going to demand that there be choice,” Cunningham said.

Still, prime funds will likely be one choice among many rather than a default investment in years to come. Fewer funds could ultimately reduce demand for commercial paper and push rates higher, but yields are currently only a fraction of where they were before the Fed slashed its target policy rate to near zero. Retail funds shrank for a 10th straight week in the period ending last Wednesday, capping the longest stretch of outflows since 2016.

Investors may fan further out from the money markets to diversify and seek higher returns, perhaps keeping some of their money with prime and plowing less-urgent cash into short duration funds, said T. Rowe’s Joe Lynagh, who manages money market and short-term debt funds.

“There’s always a reason to hold cash, you’ve got to pay your bill next month and you really should hold it in cash,” Lynagh said. “They can invest further out along the curve, lower rate credits, things that money funds can’t invest in.”

Former Northwestern Mutual advisors join firm for independence.

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Canada, China among nations to react to president-elect's comments.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound