Following the riot at the U.S. Capitol on Jan. 6, 2021, the political arm of the Financial Planning Association faced the same dilemma as many trade groups. It wrestled with whether to give campaign donations to lawmakers who voted against certifying the presidential election results.

The conflagration “changed everything for us as advocates operating in a political environment,” said Evelyn Zohlen, who chaired the FPA Political Action Committee during the 2022 election cycle, at the organization’s annual conference in Seattle in December.

“The fallout from Jan. 6 had profound impact on political action committees across the nation,” Zohlen, founder of Inspired Financial and a former FPA chair, said. “Many, many shuttered … [they] found it just too challenging to try to navigate the environment after Jan. 6, making the decision of which candidates should receive contributions became too big a hurdle for a lot of organizations.”

After “a lot of soul searching and navel-gazing,” the FPA decided to keep its PAC, Zohlen said. It solved the problem of choosing which lawmakers to donate to by not making contributions to anyone during the 2022 cycle.

That is a substantial departure from the way PACs usually operate. A firm or trade association PAC typically collects money from its employees or members and then donates those funds to the campaigns of legislators who can influence policy that affects them.

The FPA PAC used a political crisis to rethink its approach to politics. It amended its bylaws to allow the use of PAC contributions to hire lobbyists. That move helped the FPA PAC more effectively utilize its resources, Zohlen said.

The group has retained lobbyists who could “advocate on behalf of our members [and] profession to a far broader audience of elected officials than we probably ever could have on a one-on-one basis handing out checks to elected officials,” Zohlen said. “That really has changed the game entirely for the FPA PAC.”

She pointed to FPA’s success last year in Kentucky, where the group succeed in protecting financial planners from a tax that was imposed on 36 other professions to replace the state income tax.

“That was 100% attributable” to the group’s investment in lobbying on the issue, Zohlen said.

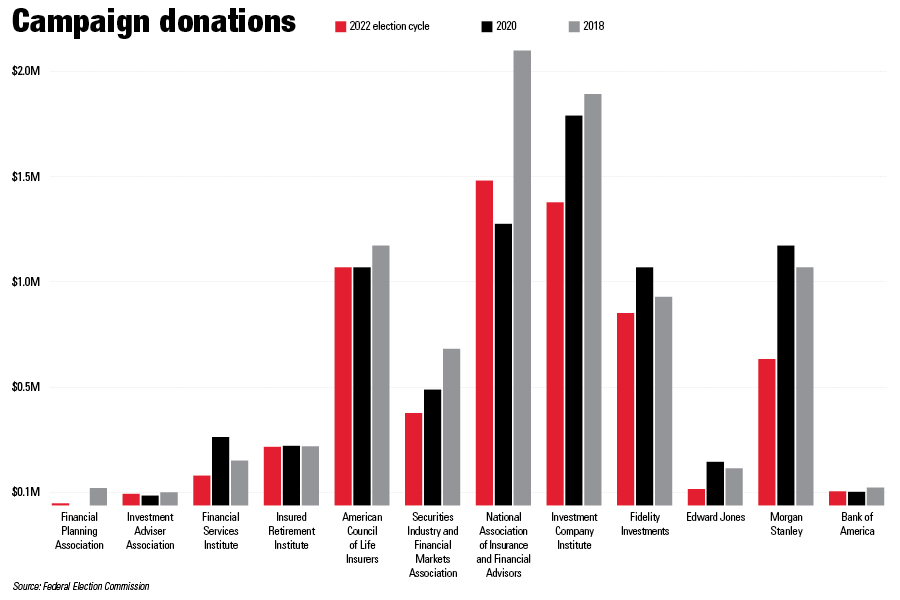

The FPA PAC is tiny compared to those of other financial industry associations. Of its approximately 19,000 members, 68 made donations to the PAC, which raised a total of $111,626 and spent $36,041 in the 2022 cycle. The organization is trying to increase the growth of its PAC to support its efforts to gain legal protection for the “financial planner” title.

Despite its small size, the FPA PAC can make an impact — like a tiny pebble in a shoe can cause a lot of irritation, Zohlen said. “We’re definitely a very little stone.”

That’s generally true for organizations representing investment advisors. They spend several thousand dollars on campaigns while major financial services trade associations — such as the Securities Industry and Financial Markets Association, the Investment Company Institute and the National Association of Insurance and Financial Advisors — spend millions.

Michael Canning is the founder of The LXR Group, a government relations consulting firm that specializes in representing pro-consumer and pro-investor groups that can tend to be the smaller lobbying forces.

“We have to do it better,” Canning said. “When you’re on the consumer and investor side, resources are very limited. You have to be selective and discriminating in how you deploy them. You have to be qualitatively better in messaging than the industry you’re up against.”

Political donations are used by trade associations of all sizes to open doors on Capitol Hill. Making a contribution in person at a lawmaker’s fundraiser is one effective way to get a message across about supporting a bill.

“It can sometimes be hard to get through staff,” Canning said. “If you can sit down and talk with a member one-on-one, it can make things happen quickly.”

The return on investment in shoe leather can be important, especially for smaller trade groups.

The Investment Adviser Association held its Adviser Advocacy Day in late September, taking 80 of its members to Capitol Hill for 91 meetings with House and Senate lawmakers and their staffs.

“We have to make sure our voice is clearly heard,” said Neil Simon, IAA vice president for government relations. “Investment advisors occupy a unique space in the financial services marketplace and have a distinct perspective on issues that are in front of lawmakers.”

One of the issues near the top of IAA’s agenda was provisions that had been tucked into the behemoth National Defense Authorization Act. They would have required investment advisors to establish anti-money laundering programs. The IAA opposed it, asserting that the measures were too broad and would have ensnared too many advisors whose business model doesn’t pose a money-laundering risk.

During its recent lame-duck session, Congress approved the NDAA but excised the AML language. Perhaps the IAA congressional outreach initiative helped.

“The AML provisions were all dropped,” Simon said. “That’s a significant achievement for IAs.”

But brokerage and insurance trade associations also can overwhelm their investment-advisor counterparts with feet on the ground in Washington.

The National Association of Insurance and Financial Advisors typically brings about 500 members to Washington for congressional meetings each May. It conducts smaller outreach later in the year as well.

With approximately 50,000 members across the nation, NAIFA can assert it has a presence in every congressional district. That reach helps it blanket Capitol Hill and get the attention of lawmakers.

“We want to make sure we never lose our ability to say that,” said Diane Boyle, NAIFA senior vice president for government relations. “It gives you the ability to go into all the offices and have conversations. We have a very robust program of engagement for our members.”

Another benefit of its breadth is that some NAIFA members move into politics themselves after their careers as insurance professionals. There are five lawmakers in Congress who are former NAIFA members. That roster includes Sen. Tim Scott, R-S.C., who who will be the highest-ranking Republican on the Senate Banking Committee beginning in January.

When NAIFA members talk to Scott and others with a background in insurance, they have a head start as they tout investor-protection features of Regulation Best Interest and the National Association of Insurance Commissioner’s best interest standard for annuity sales or argue for preserving the independent-contractor status of insurance agents.

“He understands the business. He worked in the business,” Boyle said of Scott. “That’s incredibly helpful for any industry. If you have an appreciation of the industry, it makes it easier to legislate on those issues.”

NAIFA stresses that its members help Main Street investors, a message that resonates with lawmakers. But Canning said investment-advisor groups also have a good story to tell on Capitol Hill about being on the side of investors.

“That carries more weight than a donation for a lot of [legislators],” Canning said. “But you have to be in the room to make that connection.”

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Canada, China among nations to react to president-elect's comments.

For several years, Leech allegedly favored some clients in trade allocations, at the cost of others, amounting to $600 million, according to the Department of Justice.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound