Updated December 20, 2023

The population is aging, and the healthcare landscape is shifting with it.

All Americans are feeling the financial burden of long-term care. Roughly $475.1 billion is spent in the USA on long-term care each year. Those costs directly affect the lives and financial health of many seniors and their families.

With that in mind, we are going to look at funding options for long-term care in this article. We will also look at how Americans pay for long-term care and the states where the cost of long-term care is the lowest (and the highest).

Here is everything you need to know about funding options for long-term care.

Roughly half of Americans turning 65 today will require long-term care. With life expectancy rising, and the cost of care creeping up, there is a growing need to understand funding options for long-term care. That way, you will be able to choose the best one (or the best combination).

Long-term care coverage is delivered mainly through private means. Within the last five years, about 55% of expenditures from people 65 years and older are made through these private forms of payment. In that time, 2.7% of those expenditures were from insurance and the remainder from out-of-pocket expenses. About 45% of long-term care funding is from the public sector, primarily from Medicaid (as we will see further down in this article).

Public and private options have respective benefits and drawbacks concerning expense, level of long-term-care benefits and quality of care. In this section, we will clarify some confusion surrounding long-term care.

Here is a quick look at some of the more popular long-term care options:

Now, let’s break down each one to give you a better idea of funding options for long-term care.

There are a few insurance options to hedge long-term care risk. One of these is traditional long-term care insurance, as well as life insurance policies and annuities with long-term care features.

According to a recent report by Genworth, the national median cost for a private room in a nursing home is $9,034 per month. An assisted living facility costs $4,500 per month.

Traditional long-term care insurance is a stand-alone policy devoted to providing benefits for long-term care if a need arises. This insurance delivers long-term care benefits at the lowest cost and offers inflation protection.

In recent years, sales have shifted more to combined life insurance long-term care (LTC) products. These products drew $3.6 billion in new premiums in 2016, a 500% increase over the $600 million in 2007 according to Limra, an insurance industry group.

The flexibility of these policies has been popular. Policy holders get a long-term-care benefit while living but can also surrender the policy for a portion of their premium or provide heirs with a death benefit. The latter options aren’t available for traditional policies. Further, premiums and benefits are guaranteed.

Combo policies come in two types: hybrid LTC, and life insurance with LTC riders. Hybrids provide more of a long-term-care benefit and have a very small, very modest death benefit, whereas policies with LTC riders are more life-insurance focused.

One key difference is hybrids typically have an inflation-protection feature allowing a policy holder’s future LTC benefit to grow annually. The benefits are fixed in policies with riders.

Annuity products are the least-used among insurance products for providing long-term care benefits. The products deliver a lifetime income stream and increase that income in the event of a long-term care need.

“Annuities are pretty much a last resort for long-term care,” ValMark’s Jess Rorar told Investment News. Life insurance products provide more of a benefit and give more value for the money, she added.

However, in the event insurers decline someone from buying traditional LTC or combined life insurance-LTC, annuities can serve as a backup because the underwriting requirements are easier.

Most advisers have clients that end up on Medicaid. It is the reality of aging and living for a long time. The federal government assesses income and asset levels when determining individual qualifications for Medicaid. Essentially, the client must run out of money before Medicaid kicks in.

Clients often need the help of an elder-care attorney to structure their assets appropriately. For instance, there are several exceptions for assets, such as a home, that get protected from a Medicaid spend-down calculation. An attorney can help protect those to the largest extent possible.

Medicaid facilities, however, are not usually as nice as those provided by private care. That means private insurance would likely be the better option to protect one’s quality of life.

People concerned about asset flexibility and freedom, as well as those with an aversion to medical underwriting, are often candidates for self-insurance. The caveat is that it requires the appropriate wealth.

Even if you have the assets to self-fund, however, you will get a better return on your dollars if you use an insurance solution. However, you may have to hold your assets hostage to that self-insurance, since you are not usually allowed to touch them. This sometimes leads to a reduction of lifestyle when young people set assets aside in a separate account for long-term care purposes.

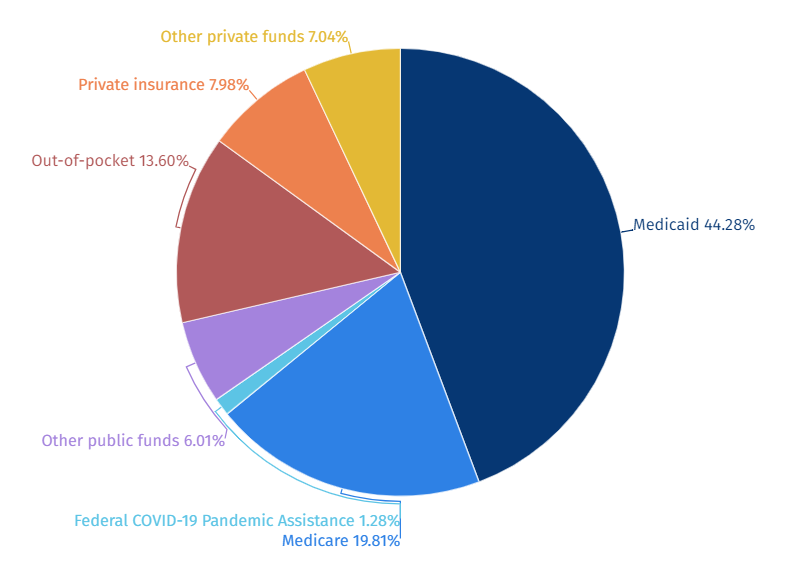

Long-term care is financed by a variety of public and private sources. According to a Congressional Research Service (CRS) data, public sources paid for 71.4% of long-term services and support (LTSS), which includes long-care spending. The two largest funders of LTSS were Medicaid and Medicare. Combined, these programs paid for 64.1% of all long-term care funding alone.

This pie chart illustrates the various programs and entities that funded LTSS in 2021.

Now that we have an idea of where long-term care funding comes from, let’s take a closer look at the two largest funders.

Medicaid is funded jointly by state and federal governments. Medicaid funds are used to pay for a number of healthcare services and LTSS, including long-term care. Funds also pay for nursing facility care, home health, personal care, and other home and community-based services.

Every state designs and administers its own specific programs, within broader federal guidelines. Medicaid is the single largest payer of LTSS in the USA.

Medicare is a federal program that pays for health services for people who are 65 years of age and older. The program also covers certain younger Americans with disabilities. Medicare covers primarily acute and post-acute care, which includes home health services and nursing.

Medicare differs from Medicaid in that it is not a primary funding source for LTSS. Post-acute Medicare benefits provide limited access to personal care services both in skilled nursing facilities and home care settings.

Long-term care—i.e., community and assisted living facilities—are essential for older people who need help with daily tasks but want to keep some independence. Long-term care facilities are the most affordable option compared to in-home care and private nursing homes. The median annual cost of long-term care facilities in the USA is $54,000.

Here is a breakdown of the states with the least costly long-term care:

Now, let’s look at the states with the most expensive long-term care.

Some people believe that their current health or disability insurance will pay for their long-term care. It is important to read the policies closely; many of these insurance policies either include limited long-term care benefits or none at all.

Most people need to find other ways of paying for long-term care. To do so, you can rely on different payment sources, such as state and federal government programs, personal funds, and private financing options.

To better understand how Americans pay for long-term care, let’s take a look at each.

If you are an older adult, you might be eligible for government healthcare benefits. Caregivers can learn more about the possible sources of financial help.

Several state and federal programs help with long-term care-related costs. Keep in mind, however, that the eligibility requirements and the benefits can change over time. And some benefits differ from state to state.

Many older adults pay for all or part of their long-term care out of pocket. This might include the use of personal savings, a retirement fund such as a pension, proceeds from the sale of a property, or income from investments.

These out-of-pocket expenses also include adult day care programs, meals, and other community-based services that enable them to live at home. Sometimes, these services are provided at a low cost, or free, by local non-profit groups and governments.

There are also several private payment options in addition to government programs and personal funds. These private payment options include reserve mortgages, long-term care insurance, and certain life insurance policies. Your age, health status, and financial situation are all factors that will determine which of these options is best for you.

Nearly half of Americans that have just turned 65 will require long-term care. The prospect poses a financial burden not only on those Americans, but their families as well. Medicaid and Medicare are government programs that are relied upon heavily.

Now that you are aware of funding options for long-term care, you can determine which will work best for you.

To find out more about funding options for long-term care, get in touch with one of the financial advisors that we highlight in our Awards & Recognition section. Here you will find the top-performing financial advisers across the USA.

Did you find these funding options for long-term care useful?

Relationships are key to our business but advisors are often slow to engage in specific activities designed to foster them.

Whichever path you go down, act now while you're still in control.

Pro-bitcoin professionals, however, say the cryptocurrency has ushered in change.

“LPL has evolved significantly over the last decade and still wants to scale up,” says one industry executive.

Survey findings from the Nationwide Retirement Institute offers pearls of planning wisdom from 60- to 65-year-olds, as well as insights into concerns.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound