Canada selects directors to oversee its public pension funds for their financial expertise and pays some six-figure salaries. In the Netherlands, board members must obtain approval from the central bank.

In the U.S., a lineup of unpaid union-backed reps, retirees and political appointees are the vanguards of a $4 trillion slice of the economy that looks after the nation’s retired public servants. They’re proving to be no match for a system that’s exploded in size and complexity.

The disparity is dragging on state and local finances and — together with headwinds that include a growing ratio of retirees to workers and lenient accounting standards — gobbling up an increasing share of government budgets. Precisely how much it’s costing Americans is hard to say. But a Bloomberg News analysis of data from CEM Benchmarking, which tracks industry performance, indicates that the price tag over the past decade could run into the hundreds of billions of dollars.

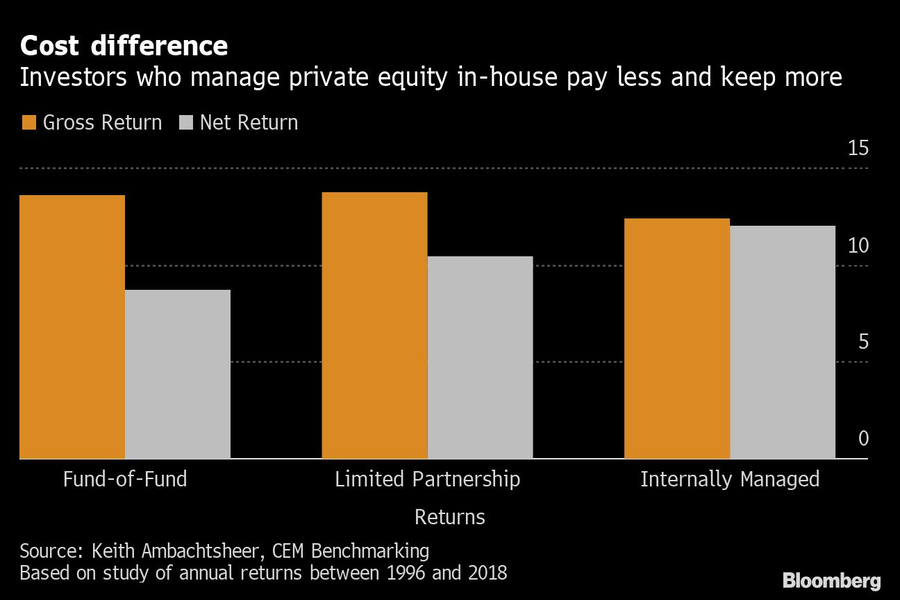

In the 10 years through 2015, a group of large Canadian funds delivered excess returns that beat a passive portfolio designed to match their liabilities by 2.2% a year. That return was 0.7% more than U.S. counterparts earned for taking greater risk above a similar index — equivalent to $280 billion in missed opportunities over a decade.

Multiple other studies have found that funds managed by boards stacked with government officials and elected representatives of public employees underperform.

As inflation and interest rates have jumped, a funding crunch is looming for America’s public pension plans. For years, the system has teetered on the edge of a crisis that’s left plans more than $1 trillion short of what they need to pay out in benefits — a gap that widened considerably during the downturn in financial markets.

Underfunded and under pressure, they’ve turned to riskier investments to boost returns, piling into private equity, hedge funds and other alternative assets. Where boards’ own expertise has fallen short, they’ve relied on investment staff and outside advisors, whose appetites for complexity add to costs and eat into returns.

“It’s the worst of all possible worlds,” said Mike Reid of CEM Benchmarking. “The U.S. would do well to reconsider its approach.”

The disconnect was on display at a 2021 investment committee meeting of the California Public Employees’ Retirement System, which provides benefits to more than 750,000 individuals. An external advisor warned board members that the boom in blank-check companies was a sign of froth in financial markets.

“I had never heard of those,” chairwoman Theresa Taylor told her fellow directors of the then-sizzling products known as SPACs, according to a transcript of the meeting.

A compliance official for the state’s franchise tax board and a former union official, Taylor — elected to represent state employees — took over as CalPERS’s president last January. She’s now a key overseer of a $448 billion investment portfolio that at the end of fiscal 2021 was $163 billion shy of what it needs to fulfill its pension promises.

A spokesman for CalPERS said in a statement that board members are thoroughly briefed by investment officials and subject matter experts before making any decisions. The 2021 SPAC discussion didn’t involve an agenda item requiring action, he added.

Taylor’s trajectory isn’t unusual. Nor is a gap between the skills directors bring to boardrooms and the challenges they face as fiduciaries for the nation’s 6,000 state and local pension plans.

Many public plans were set up in the World War II era or before, and by law their boards were filled with public servants, retirees and government officials — the communities they were built to represent.

Serving as unpaid part-timers, many assumed the roles as financial novices. And for decades, that didn’t matter much. Pension plans were rounding errors in government budgets, and boards hewed to legal lists of vanilla investments: government bonds, mortgages and common stocks.

Plans still generate most of their funding from investments, and the rapid growth of the systems has heightened the stakes. If returns fall short, the pensions’ members have to help make up the deficit, or public funds are diverted. Unlike in many other countries, it’s almost impossible to respond to funding shortfalls by cutting benefits for current members.

Systems are underfunded partly because public officials face greater pressure to fulfill today’s demands than to fund obligations 20 or 30 years away. And because hikes in taxes and contributions are unpopular, there’s an incentive to downplay the problem.

Instead, plans are investing in higher risk assets, which make up about one-third of holdings, according to data from Preqin. That allocation has more than doubled since just before the 2008 financial crisis as plans have poured $1 trillion into alternatives.

The shift presents new challenges for directors whose day jobs don’t require them to keep up with investment trends.

William Murray, a teachers’ union representative on Connecticut’s Investment Advisory Council for 18 years, said that even with training it can take new members years to get up to speed.

For a meeting last year, the treasurer’s office provided council members with a 641-page briefing book. Participants are expected to use their judgment in reviewing it, the office said through a spokeswoman.

Murray said he scans the materials and counts on members with different experiences to pick up on specific issues as part of an extensive review process.

“There’s a lot of stuff we talk about at meetings the average person doesn’t invest in,” Murray said.

Most individuals in the U.S. aren’t allowed to invest in these specialized private markets: federal securities regulators require a certain amount of wealth or financial sophistication before someone can be classified as a so-called accredited investor.

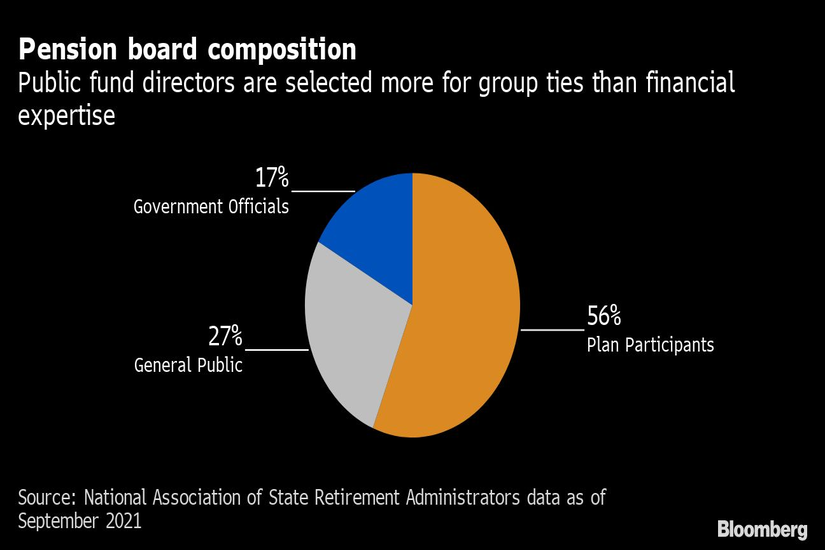

There’s no such test for the trustees who oversee public pension funds. More than half of U.S. directors are still drawn from rank-and-file employees, more than a quarter from the public and the remainder from government officials, according to the National Association of State Retirement Administrators. While some directors have strong financial credentials, others are novices.

“Part-time, lay trustees are simply no match for the agents and complexity they are expected to supervise,” said Richard Ennis, co-founder of consultancy EnnisKnupp.

Serving on a public pension board is a major commitment. Most funds convene monthly or quarterly, with meetings lasting a few hours to a few days each. But the lack of national standards means there’s no one entity keeping an eye on who’s populating boards. While there are accounting standards, they allow plans to make more aggressive assumptions about how well they’re funded than in the private sector.

Kathy Landry represents retired bus drivers, janitors and other staff on the board of the Louisiana School Employees’ Retirement System. The job requires her to attend monthly and two-day quarterly meetings, complete annual training on investing, ethics and sexual harassment and field queries from fellow retirees. She votes on how to deploy the system’s $2 billion portfolio, but that’s not what inspired her to serve.

“I’ve always been a voice for bus operators,” Landry said. A representative for the system declined to comment.

As portfolios have become more complex, directors have hired outside consultants to handle relationships with portfolio managers — some of Wall Street’s most sophisticated salespeople — and to make pre-vetted investment recommendations based on their pitches.

The costs can quickly add up. Under standard terms, investors pay 2% management fees and a performance fee of 20% of profits to general partners of alternative investment firms.

The San Diego County Employees Retirement Association hands over all of its $15 billion in assets to external managers. In the year through June 2022, it paid 80% of its $60 million in investment expenses to alternatives managers for investing just 17% of assets. A representative for the San Diego plan declined to comment.

Many pension advisors make smart recommendations: the guidance that CalPERS should stay away from SPACs, for one, was proven sound once regulators ramped up scrutiny of that market, which has all but ground to a halt. Yet it remains unclear how closely individual directors evaluate investments that get put in front of them.

“I served with one director for about 15 years and never saw him ask a question” about his system’s investments, said Herb Meiberger, a finance professor who sat on the board of the $36 billion San Francisco Employees’ Retirement System until 2017. A spokesman for the system said it takes governance and fiduciary duty very seriously, and that board members receive training to help them execute their duties.

Harvard finance professor Emil Siriwardane has researched why some U.S. plans have put more money into alternatives. It wasn’t the worst-funded or those with the most aggressive performance targets. “By a factor of eight-to-ten,” the closest correlation is the investment consultants that pension plans hire, Siriwardane found.

Canada’s detour from the American-style model began in the late 1980s, when Ontario’s government and teacher federation decided to reboot a plan that was invested in non-marketable provincial bonds. They set up the Ontario Teachers’ Pension Plan in 1990, concluding the province could save $1.2 billion over a decade by operating more like a business.

Ontario Teachers’ first board chairman was a former Bank of Canada governor and its first finance chief was a corporate finance veteran. It soon began investing directly in private markets and infrastructure, opened offices in Europe and Asia and acquired a large real estate firm. The system pays its board members close to what corporate directors make, and manages 80% of its investments internally. Those practices have put it on a solid financial base: Ontario Teachers’ says it’s been fully funded for the past nine years, with a current funding ratio of 107%.

Until the 2008 financial crisis, boards in the Netherlands — where traditional public sector pensions are common — looked a lot like those in the U.S. Then the country’s central bank was given authority to assess candidates. It looked at directors’ combined risk management, actuarial and other expertise.

Many smaller Dutch funds didn’t make the cut. The regulatory hurdles helped set off a wave of mergers that, over the past decade, has reduced the number of plans by over two-thirds. The system has sprouted professional directors who serve more than one at a time.

Few U.S. boards are following suit. Only 19 of 113 funds studied made changes to their board composition from 1990 to 2012, a paper published in The Review of Financial Studies in 2017 found.

“A lot of funds in the U.S. like the idea of transforming, want to transform, but don’t have the political fortitude to do it,” said Brad Kelly of Global Governance Advisors, a Toronto-based firm that works with U.S. and Canadian pension funds.

For most, reforming their boards would require states to amend laws and for union officials, politicians and others who control the purse strings to hand them over. There’s little incentive for that to happen.

Margaret Brown won a seat on CalPERS’s board five years ago, after its handling of her benefits during a serious illness convinced her it needed a shakeup. As a director, Brown became an outspoken critic of the system. She lost her post in 2021 after organized labor reportedly spent a half-million dollars supporting a challenger and an ally running for reelection.

“If the pension looks bad, that riles up anti-pension people” who want to replace traditional plans with 401(k)-style ones, she said. “As long as you don’t raise red flags, you’re not helping your opponents.”

The spokesman for CalPERS said that board members bring a diverse set of perspectives and backgrounds to their work, which are a vital part of ensuring the public is well represented.

Some of the biggest plans are starting to make changes. The $183 billion Teacher Retirement System of Texas in August requested funding for 25 in-house investment managers. It’s part of a cost-cutting program that has saved $321 million in fees over the past four years.

Last February, CalPERS named Nicole Musicco as its chief investment officer. An Ontario Teachers’ alumnus, she has discussed publicly the opportunity to increase direct investing in private markets, infrastructure and real estate. The changes could take a while to show benefits. “To build an in-house direct deal-doing program, that’s a 10-year journey,” she told fund officials at a September meeting.

In the meantime, public pensions’ funding challenges could encourage more to address their structural flaws. The worst-case scenarios are dire. A state-appointed receiver for Chester, a city in Pennsylvania with 33,000 residents, filed for bankruptcy in November because of a massive debt to its employee pension funds. An unfunded pension liability of more than $100 million was its biggest single unsecured debt.

“The whole system is set up to fail,” said Keith Ambachtsheer, president of KPA Advisory Services and a co-founder of CEM Benchmarking.

Former Northwestern Mutual advisors join firm for independence.

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Canada, China among nations to react to president-elect's comments.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound