This month’s edition continues with new co-author (and AdviserTech guru) Craig Iskowitz, along with guest contributor Kyle Van Pelt. It kicks off with a look at Schwab’s announcement that all existing Schwab clients will receive freeaccess to a MoneyGuide financial plan that they can create for themselves using the MoneyGuide One guided experience (or work with a Schwab Intelligent Advisory CFP professional for an advisory fee as little as $30/month), which highlights the fact that financial advisers can no longer justify their financial planning value by just inputting client data into and presenting the output from comprehensive financial planning software, and instead will increasingly be required to specialize in niches, and/or demonstrate their value in the conversations they have around the planning software.

From there, the latest highlights also feature a number of other interesting adviser technology announcements, including:

Read the analysis of these announcements, as well as discussion of more trends in adviser technology, including Envestnet preparing its own direct indexing overlay tools as technology increasingly becomes the new value-add layer, Vanguard beginning to develop its own robo-platform for advisers to compete for custody, Xtiva raising $10 million to compete in the complex process of integrating adviser compensation systems in large-scale financial services enterprises, and Timeline raising $2.3 million in capital to compete in the increasingly popular realm of specialized planning tools that go beyond what generalist planning software can provide (in the case of Timeline, to facilitate retirement distribution planning in the decumulation phase!).

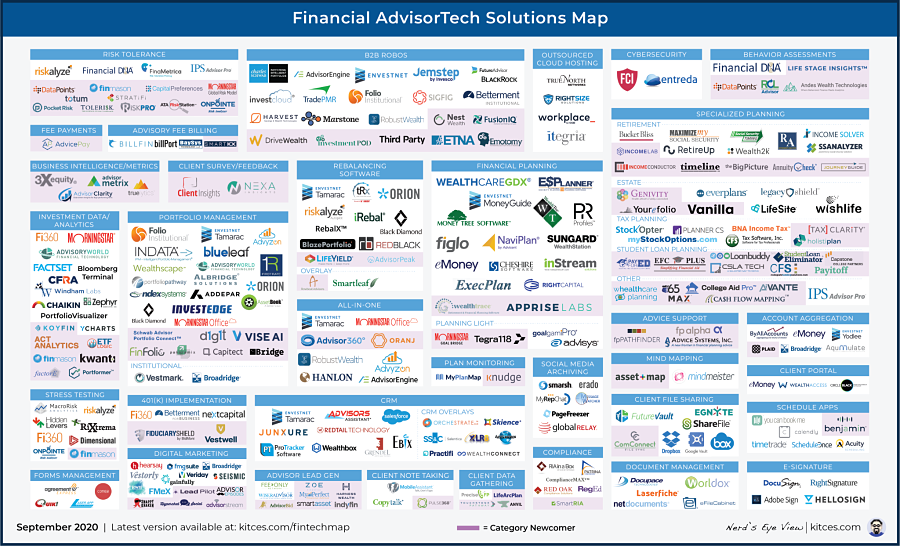

Be certain to read to the end, where we have provided an update to our popular new Financial AdviserTech Solutions Map!

I hope you’re continuing to find this column on financial adviser technology to be helpful! Please share your comments at the end and let me know what you think!

*#AdviserTech companies who want to submit their tech announcements for consideration in future issues, please submit to TechNews@kitces.com!

Schwab launches free access to MoneyGuide financial planning software for self-directed clients. In the early days of financial planning, one of the key benefits of working with a financial adviser was that they had access to sophisticated tools – known as financial planning software – that could analyze and project a client’s financial planning situation more effectively than they could possibly do on their own with graph paper, a calculator or a homegrown spreadsheet. The end result of this planning-software-as-advanced-calculator approach was that clients would pay a financial planning fee for the adviser to gather their data, input it into the software and present them with the software output (i.e., the financial plan). And in fact, our latest Kitces Research on How Financial Planners Actually Do Financial Planning finds that a plurality (49%) of financial advisers still deliver financial planning primarily by delivering the comprehensive financial planning software output to their clients. However, the reality is that in the internet age, there is an ever-growing abundance of increasingly sophisticated software available on the internet, and often available for free, because anything valuable enough for consumers to engage with around their finances can often be used by a traditional financial services firm to attract or retain prospective clients. In fact, this has been the entire growth story of Personal Capital, which developed a personal financial management solution for consumers, and gives it away for “free’ because user growth of the app forms the lead generation funnel it needs to gather what is now more than $12 billion of assets under management! The latest in the world of giving away planning software tools for “free” to attract and deepen relationships with current clients is Schwab, which announced a new offering last month that will provide direct access to financial planning software for all existing Schwab clients (though notably, only for clients, while prospects get a more generalized Financial Planning Hub with a series of simpler calculator tools). And as the adviser community quickly noticed, the software that Schwab highlights as its new Schwab Plan offering is none other than the popular MoneyGuide solution (specifically, a customized version of its MoneyGuide One product), putting into sharp relief the contrast that financial advisers are still charging an average of $2,400 for the output of comprehensive financial planning software that Schwab is now giving away to its clients entirely for free. Of course, a key distinction of the new Schwab plan is that the software is being made available directly to clients – in other words, as a self-directed solution – while financial advisers typically input data on behalf of their clients and walk them through the results. Yet the reality is that Schwab is growing its own human financial planner offering as well, with the Schwab Intelligent Portfolios Premium offering that includes access to a human CFP professional for a $25,000 minimum or as little as $300 upfront plus $30/month. Which on the one hand emphasizes that even Schwab recognizes that there’s a value to human financial advisers (and that consumers are willing to pay for human financial advisers) above and beyond what they can get from the use of self-directed technology alone. On the other hand, Schwab rolling out a free version of MoneyGuide One to all of its own clients emphasizes that increasingly the value of financial planning will no longer be in the planning software and its output (where Schwab is setting a new price point of “free”), or in inputting the data into the planning software on behalf of clients (because advisers will not be able to sustain $2,400 planning fees for doing outsourced data input for clients alone!), but in the planning conversations that emerge between the adviser and the client (for which planning software is increasingly becoming the collaborative conversation tool that helps advisers go deeper instead!). Nonetheless, when a plurality (49%) of advisers charge thousands of dollars to deliver financial planning software output as “the plan” that Schwab is now providing access to for free, Schwab’s ongoing shift into financial planning as a lead generation tool for its managed accounts, proprietary ETFs and direct-to-consumer brokerage business will continue to put pressure on independent advisers to move upmarket (beyond Schwab’s mass affluent offering) into niches (more differentiated than what Schwab can focus on given its size and need for a mass reach), or find new ways to deliver financial planning itself that focus on the collaborative experience and the conversations rather than just the output of even sophisticated planning software alone.

LPL Meeting Manager aims to tackle the biggest financial adviser time waste: meeting prep. The mantra of most financial services firms is that advisers should maximize the time they spend meeting with clients and prospects – the adviser’s essential front-office work – and either delegate, outsource or automate the rest. Yet the latest Kitces Research on “How Financial Advisors Actually Do Financial Planning” finds that in reality, the average adviser spends less than 20% of their time meeting with existing clients, but spends 24% of their time prepping for those client meetings and doing the client servicing follow-up work! Of course, the irony is that the more advisers try to increase their meeting time with clients, the more meeting preparation work that has to be done, the more post-meeting client servicing tasks there are and the worse the problem gets! Accordingly, this month independent broker-dealer LPL announced at its annual Focus conference that it is launching a new Meeting Manager tool that aims to tackle the meeting preparation blues (after having been previewed at its Focus 2019 event). At its core, LPL’s Meeting Manager is a series of meeting template tools, for everything from crafting an agenda to pulling together the client’s investment reports, and coalescing it into a single PDF document, similar to the recently launched Pulse360 for independent advisers. Of course, the reality is that advisers can already create their own PDFs of a meeting report, but according to LPL’s own research the average adviser goes into six different applications to prepare for a meeting (and one adviser went into as many as 23!). LPL is aiming to solve that by integrating all the key meeting preparation data into Meeting Manager, so advisers can prepare for the entire meeting in one place (and largely automate much of the meeting preparation process along the way). In addition, Meeting Manager has an Outlook-integrated meeting scheduler that sets up the meeting time with clients and a centralized dashboard where all members of the team can interact with and support the meeting preparation process, and it automatically verifies that the adviser has met the associated compliance requirements in communications with clients. LPL’s Meeting Manager is currently in alpha phase, with a full-scale rollout expected later this year, and the company has already announced further plans to integrate MoneyGuide financial plan updates for existing clients and AdvisoryWorld proposals for prospect meetings. The significance of tools like LPL Meeting Manager (and emerging competitors like Pulse360) is that top adviser productivity is really a game of inches, where leading advisers spend just an average of four hours/week more in client meetings than the rest, as that cumulatively amounts to 150-plus additional client meetings over the span of a year! And advisers typically spending 24% of their time – adding up to nine to 10 hours per week – handling meeting preparation and follow-up client servicing, tools that focus on the seemingly mundane efficiency opportunities around meeting preparation and client servicing actually have the potential for a very material impact on adviser productivity!

Is the AdviserTech pendulum swinging back toward proprietary as Merrill Lynch builds its own FP software?In the 1980s and 1990s, traditional wirehouses had the best adviser software because of their vast resources and willingness to use them, as well as the tremendous adviser head count over which they could amortize their development costs (relative to the tiny nascent independent adviser movement). In the early 2000s, that pendulum swung back the other way, as the independent market grew rapidly, and the independent adviser software ecosystem did too around it, in a virtuous cycle where a growing addressable market of independent advisers led to more technology tools, and more technology solutions for independent advisers attracted even more from the industry’s traditional employee channels. Eventually, even wirehouses themselves decided that it wasn’t worthwhile to spend a ton of money to build and maintain their own software stacks, and instead started partnering with the independent software vendors to deliver great experiences for their brokers. Yet as financial planning increasingly becomes the heartbeat of the client relationship, it is becoming apparent that, for the largest firms, financial planning software is too important to outsource and instead is something worth owning and building as a proprietary solution for the opportunities it can open up. In this context, natively integrated software is becoming the name of the game. Natively integrated software is what allows Uber to process credit cards, let drivers navigate riders to their destinations, and make phone calls and send text messages. Uber doesn’t build all of those underlying features from the ground up (they partner with other organizations to do that), but the workflows themselves are integrated perfectly into Uber’s proprietary app. Which is notable, because the depth of integrations (or rather, the lack thereof) is a well-documented challenge for AdviserTech solutions today, especially the most frequently adopted ones that were built 15 to 20 years ago, before APIs took the market by storm, and which have been slow to adapt. Accordingly, last year Merrill launched a tool called Advisor Insights which, similar to Morgan Stanley’s Next Best Action solution, analyzes client data and provides recommendations to advisers that they can then bring to the client as a suggested next conversation. In other words, it surfaces the next opportunity to provide quality advice or find a new solution to implement with the client. But such tools, which rely on pulling together investment, CRM and financial planning information into one central location to analyze and trigger action items, are only half-baked without native integration to the financial planning software (i.e., no matter how much account data are analyzed, how can you provide the best recommendation for a client if you aren’t hooked into the most current financial plan?). And so now, large wirehouses like Merrill Lynch (and Morgan Stanley) are leveraging the key advantage they do have – a base of employees who are all required to use the same technology suite, enabling the company to build a single integrated tool that it knows all its brokers will (and must) use -- and taking the financial planning software and the recommendation actions it generates back into their own hands. This means, in essence, that the ongoing integration woes of the independent AdviserTech ecosystem are becoming the key trigger swinging the AdviserTech pendulum away from the independents and back to the large-scale proprietary platforms.

Timeline retirement planning software raises $2.3 million seed round to better scale digital retirement drawdown software. It’s always exciting to adopt innovative new AdviserTech solutions, but using the brightest newest tech usually comes with the downside of being tethered to a potentially underfunded startup. This means that if the company runs out of money, advisers could end up out in the cold with a giant hole in their process. Advisers who are using the Timeline App no longer need to worry about this occurrence, as the young firm has just scored $2.3 million in a new funding round. Timeline App is a specialized financial planning tool focused specifically on the distribution (i.e., decumulation) side of retirement. The goal of the software is to give prospective retirees a better understanding of the sustainability of their retirement distribution strategy given the uncertainties of market volatility; in essence, Timeline is a tool to model safe withdrawal rates and other portfolio-based retirement spending strategies. The CEO of Timeline, Abraham Okusanya, was interested in the research that has been done around retirement distribution, starting with Bill Bengen’s famous safe withdrawal rate study more than 25 years ago, the two decades of additional withdrawal research since, and how to optimize it under different conditions. Accordingly, the core of Timeline App is calculating a probability of a client outliving their portfolio based on a projected withdrawal rate, which is presented as a percent probability of success. In addition, Timeline can transform longevity data into a visual story of retirement income sustainability that is relatively easy for clients to visually see and understand (as dynamic visualization is quickly becoming table stakes in retirement planning), along with the option to adjust input parameters interactively on the fly, including the impact of changing asset allocations, rebalancing, glidepaths, fees and taxes. While this added functionality might increase the difficulty of using Timeline, as Kitces Research has shown, the most highly rated financial planning software among advisers is the software that takes the longest to use and is the most customizable, because more comprehensive software is most able to adapt to the needs of the client and therefore the most effective at helping advisers to fully demonstrate their value. Timeline delivers this specialized, adviser-supportive approach via some of its unique abilities, such as a real-time monitoring capability that alerts the adviser when a client drifts off target, as well as the ability to display a series of rolling 30-year retirement periods and how much money is left at the end of each. For a startup tech company trying to change the retirement decumulation side of the advisory industry, $2.3 million still isn’t a lot of money, but what’s more important than the amount invested is who did the investing. The round was led by global wealth management technology vendor FNZ (pronounced FN-Zed for Americans), which took a minority ownership stake. The New Zealand-based company has a large customer base spread across Europe and Asia and is planning to include Timeline in its own app store. This opportunity could greatly increase Timeline’s user base beyond just what is already a sizable opportunity in the U.S. adviser marketplace, and the new capital will be used to enhance Timeline App’s enterprise capabilities to scale delivery of its retirement decumulation planning experience. Enterprise features are a gap many startups have trouble closing since they require significant resource investments to develop, including enterprise dashboards, administration tools and compliance reporting to support centralized management across a large firm’s user base. Having been focused solely on selling to individual advisers and RIAs, this additional functionality will be critical if they expect to sell to broker-dealers, RIA aggregators or other large firms. From the industry perspective, the limitations of increasingly specialized advisers using generalist financial planning software has driven the growth of specialized software tools, with 20% of firms using separate Social Security software (such as Covisum), 18% using special tax planning software (such as LifeYield), and 9% using stand-alone retirement income tools (such as Timeline App or IncomeConductor). This growing subset of advisers believes that it’s better to do one thing extremely well than to do everything in a mediocre fashion, since true retirement distribution planning is still largely a gap for established financial planning software players (even as the leading financial planning platforms, such as MoneyGuidePro, eMoneyAdvisor, RightCapital and NaviPlan, continue to add new features and functionality). We expect new apps will continue to take advantage of the trend toward making financial planning software more comprehensive and specialized, to boost advisers’ ability to express their value-add in increasingly sophisticated ways, as generalist financial planners (and the financial planning software itself) becomes increasingly accessible to consumers at a low (or zero) price point. Though in the long term, the real question is no longer whether or not advisers need to differentiate themselves in order to survive, but how many separate apps they can implement before their workflows and daily processes become too difficult to manage.

Riskalyze selects Rowboat Advisors to add “Intelligent Tax Optimization” to AutoPilot rebalancing technology. It was Benjamin Franklin who said, “In this world, nothing can be said to be certain except death and taxes.” And while no current technology can make death less painful, there are a lot of adviser software programs geared toward reducing clients’ tax burdens. In fact, at this point, almost every portfolio rebalancing engine has at least a basic level of tax awareness, including avoiding short-term capital gains, tax loss harvesting and avoiding wash sales. Yet in practice, these should now be considered mere table stakes for any portfolio management system; the next level up from tax aware is tax management, which usually includes features such as asset location (placing tax-efficient securities in taxable accounts and tax-inefficient ones in nontaxable accounts) and then tax transition (selling down low cost basis positions over multiple years to spread out the capital gains hit). The highest level of functionality, though, is tax optimization of the entire portfolio, effectively the holy grail of portfolio rebalancing. As with the quest for the actual holy grail, though, this has, historically at least, been impossible to achieve because most portfolio rebalancers are rules-based, which means that they evaluate each account based on a preset list of rules (such as “don’t generate any sell orders that result in short-term capital gains”) that run in prioritized order and only check each position once. Portfolio tax optimization, however, requires checking each account dozens or hundreds of times to determine the optimized set of orders that provide the best results among a series of possible rules and strategies that intersect one another. And portfolio optimization is what Riskalyze is aiming to deliver to clients who use its Autopilot Trading platform, to be done via its recently announced partnership with Rowboat Advisors, makers of a new generation of automated (and very tax-savvy) portfolio rebalancing software that will power Riskalyze’s “Intelligent Tax Optimization.” The distinction is that, rather than the rigid rules-based framework of traditional rebalancers, Rowboat’s portfolio tax optimizer will allow an adviser to run tax-aware trade scenarios while also setting parameters around a capital gains budget based on a client’s risk metric from Riskalyze. This kind of tax-efficient portfolio rebalancing, which includes evaluating the trade-offs between efficiency and tracking error, is only offered by a few vendors in the RIA space (another being Softpak Financial Systems). In addition, Riskalyze also announced automated tax-loss harvesting (again powered by Rowboat Advisors), which provides a recommended list of positions sorted by estimated capital losses and (hopefully) with an interface that shows the adviser how the client’s tax budget is impacted by each harvest order. Of course, advisers cannot use this software unless their custodians support selling shares out of specific tax lots, but Charles Schwab, Fidelity, TD Ameritrade and RBC currently support this, and Riskalyze is reportedly nudging LPL Financial and Pershing to offer it as well. From Riskalyze’s perspective, adding these tax alpha features is one way for the company to stand out as it continues its evolution from its risk tolerance assessment roots toward an increasingly crowded market for portfolio management software that includes at least 50 products, most of which look more and more similar as they all try to sell to the same group of independent advisers. Especially since, up until now, Riskalyze has been focusing on the lower end of the market with solutions that have fewer options and configurations, making them easier to use and manage for smaller RIAs. But with this announcement, the company is taking the next step to start moving upstream toward bigger firms, which disproportionately have the clients with larger and more complicated portfolios and tax issues. These tax-efficient tools should also be a nice complement to Riskalyze’s recent collaboration with order management system provider FIX Flyer on Connected Trading, which automates trading by eliminating the need for manual account allocations at each custodian, combines order files for different asset classes and automates block trading. When Riskalyze launched AutoPilot in 2015, it was a big step, as it was stepping out of its comfort zone of risk assessment and butting up against a new class of competitors. The good news about its Rowboat integration is that Riskalyze is differentiating its portfolio management solution with the latest tax alpha capabilities in a crowded marketplace. The bad news, though, is that there are arguably still too many portfolio management systems to survive, and Riskalyze will likely need to continue to expand its functionality to keep pace with the rest of the industry across multiple categories of wealth management technology.

Will Fidelity’s Bond Beacon satisfy advisers’ newfound desire to trade individual bonds?Fixed income has always been an integral part of portfolio construction. Traditionally, it is a way to provide stability to an investor’s portfolio. As a result, it’s often just viewed as the other part that completes the client’s less-stable-and-more-opportunities-to-invest equity allocation. Yet in reality, 2020 has been anything but stable, for both equities and the fixed income market, and the combination of rates going to zero and the news that the Fed would be buying corporate bonds in large volume both creates new opportunities to add alpha with active management of bonds and stokes fears that the Fed’s intervention will spawn inflation, causing bond rates to rise and leading advisers to be increasingly interested in strategies like bond ladders that can be held to maturity in a potentially rising interest rate environment. However, in practice actively trading bonds is a balance of art and science, due to the lack of market transparency, potentially high mark-ups and often poor liquidity. In other words, lack of real-time insight makes trading bonds directly less favorable for the typical adviser than using bond mutual funds or ETFs (which themselves are more straightforward to trade and implement, and have full-time professionals monitoring for effective execution of the funds’ underlying bond funds). Enter Bond Beacon from Fidelity, which aims to bring the real-time insight of institutional bond market desks directly into an adviser’s hands. From the adviser perspective, the appeal of Bond Beacon is relatively straightforward: more transparent information about pricing and mark-ups allows advisers to obtain better execution for their clients, reducing the cost drag of bond trading and/or allowing advisory firms to find new or more bond alpha opportunities for clients. From the Fidelity perspective, one might ask, “Why is Fidelity launching this now?” with interest rates as low as they are, and more and more advisers seeking alternatives (literally, into the alternative investments realm) to their bond allocations (spawning the recent explosive growth of platforms like CAIS and iCapital). But in the end, bonds remain an anchor to most advisers’ portfolios for some material allocation (especially given the concentration of advisers working with retirees, who tend to hold more conservative portfolios), and the mark-ups on individual bond trading are a great source of revenue for Fidelity (especially relative to the zero commission, or ZeroCom, alternative they earn when an adviser buys a bond mutual fund or ETF!). In other words, a slick new tool like Bond Beacon may help convince at least a few Fidelity advisers to eschew ZeroCom bond ETFs and mutual funds and instead engage in more fixed-income trades for Fidelity-traded bond markup revenue. (Incentives matter!) Of course, the irony is that the transparency and trading capabilities of Bond Beacon may cut the mark-up that Fidelity might have otherwise earned. Yet in today’s environment, where most sizable independent advisory firms are multicustodial, custodians wage war daily to offer better features that entice advisers to transact on their platform as opposed to their competitors! This means a lower mark-up for Fidelity, thanks to Bond Beacon, is still better than no mark-up because the advisory firm trades the bond through one of its other custodial relationships instead. (Competition matters, too!) Though ultimately, it remains to be seen whether advisers – particularly multicustodial advisers with choices on where to trade their bonds – will be willing to rely on Fidelity’s Bond Beacon, or instead opt for newer, even more independent bond trading solutions such as Bond Navigator or 280CapMarkets. On the other hand, the reality may simply be that Fidelity saw the emerging success of those platforms and others like them, and that’s why it decided it could offer a similar solution to serve its clients directly (and hope to retain more bond business) in the first place.

Apex Clearing selects Marstone as partner to launch a pay-for-custody platform.Custody is like plumbing: You don’t really think about it until it stops working. Apex Clearing is trying to shift custody to the forefront of advisers’ business minds by merging its innovative, digitally based custody functions with Marstone’s digital advice platform. By offering a combination of custody plus digital-first tools directly to registered investment advisers, it’s trying to position itself as the most digitally savvy RIA custodian that’s the talk of the town. Apex Clearing has always been lumped in with the smaller, second-tier custodians, but it differentiated itself with its fintech-friendly platform, which was designed as a latticework of application programming interfaces (APIs) that exposed the custody and middle-office services, but required firms to build their own user access layer. That was appealing to a wave of robo-advisers, and Betterment, Wealthfront, Stash, Robinhood, Acorns and more all built at least their first-generation platforms on Apex. However, when it comes to the RIA marketplace, at best only the top 10% of RIAs have a technology budget that allows them to hire developers to build such an interface on top of a digital-but-raw RIA custodian. Accordingly, Apex has pursued the other 90% of independent RIAs through an intermediary provider that creates the adviser dashboard that most other RIA custodians already offer, partnering with so-called B2B robos like RobustWealth, AdvisorEngine or InvestCloud. However, advisers have largely resisted paying an intermediary technology layer on top of an RIA custodian. Still, a tech-only solution that mostly served robo-advisers and other fintechs wasn’t the model that Apex’s CEO, Bill Capuzzi, was planning to continue with. So if RIAs won’t pay for a technology layer on top of a custodian, Capuzzi appears to be structuring partnerships that would allow Apex to be the all-in-one technology-plus-custodian solution, ostensibly in the hopes of being able to charge software-company fees for providing RIA custody (as distinguished from the Big-Four-soon-to-be-Big-Three custodial firms – Pershing, TD Ameritrade, Schwab, and Fidelity – which have no platform fees and instead make their profits on the back-end in areas like spreads on money markets, shareholder servicing and sub-TA fees on mutual funds and ETFs). To create this solution, Apex tapped Marstone, a firm that has flown under the radar for the past few years after making a splash by being one of the first digital providers to partner with Pershing in 2016 and announcing in 2018 that HSBC USA would begin white-labeling Marstone’s software for its consumer self-directed offering. Marstone also partnered with Tegra118 (formerly Fiserv Investment Services), a provider of portfolio accounting/portfolio management enterprise solutions. Apex is also not the first custodian to partner with Marstone, either; Interactive Brokers announced its integration back in January 2019 to build a fully integrated, turnkey solution (and more recently Interactive Brokers announced a tech-plus-custodian partnership with TradingFront that is intended to justify IB continuing to charge trading commissions in a ZeroCom world). In the case of Apex and Marstone, though, it is expected that they will be selling their new combined digital offering and custody solution for an outright platform/technology fee, rather than trying to generate trading commissions or otherwise giving it away as a loss leader (and making all their money on the back end) as other custodians are doing. As of yet, pricing has not been publicly announced, but with Schwab apparently doubling down on its “no minimums, no platform fees” pledge, the big question will be whether Apex can identify a combination of technology and price point that is palatable to advisers used to paying nothing for custody and limited fixed-fee costs for AdviserTech software, and whether all of these deals and products can attract enough new revenue from RIAs, broker-dealer, and other wealth management firms, given that ever more technology vendors are crowding into the space at ever-more-competitive pricing.

Apex hires Morningstar’s Tricia Rothschild to compete more aggressively for RIA custody. The current world of RIA custody falls into three broad groups: the Big Four (Schwab, Fidelity, TD Ameritrade and Pershing Advisor Solutions) that cater primarily to large and midsize RIAs; the second-tier RIA custodians like SSG and TradePMR that work with smaller advisers or have targeted niches in particular segments of the adviser community; and the B-D-affiliated RIA custodians (e.g., LPL, Raymond James, RBC, Wells Fargo) that were historically self-clearing brokerage platforms that expanded into the hybrid RIA business and are now trying to grow their RIA platforms (often by capturing their own brokers in the transition to the RIA model). The ultimate challenge is that RIA custody and clearing is a scale business – so much that virtually every RIA custodian is ultimately just a division of a larger brokerage offering, from the retail brokerage businesses of Schwab and TD Ameritrade, to the independent broker-dealer clearing businesses of Fidelity and Pershing, the brokerage self-clearing businesses of LPL and Raymond James and the overlay providers like SSG (which operates on top of the Pershing platform) and TradePMR (which leverages Wells Fargo’s First Clearing platform). That makes it especially hard for new competitors to enter the RIA custody business. In this context, the story of Apex Clearing has been a unique one – built on a more recent and modern API infrastructure, Apex Clearing was the back-end custody and clearing firm of choice for most of the first generation of robo-advisers, including Betterment, Wealthfront, FutureAdvisor, Motif, Stash, Robinhood, Acorns and more, and has used its growth with fintechs as the basis for establishing economies of scale to expand further. Yet what was arguably the greatest benefit of Apex Clearing for fintech platforms – its robust API-driven back-end that allowed robo startups to build whatever front end they wanted – has proven to be its greatest challenge in gaining adoption among independent RIAs, who don’t necessarily have the tech-savvy chops to build their own front-end interfaces. In recent years, this led to Apex trying to establish a series of strategic partnerships with other B2B robo-advisers that offered their own front-end robo onboarding tools, including AdvisorEngine (née Vanare Nest Egg), Harvest Savings & Wealth (née Trizic), InvestCloud, FolioDynamix and more. But independent RIAs have shown little interest in paying for an additional layer of robo tools on top of their RIA custodians, leading Apex to announce this summer its own “Apex Extend” front end for independent RIAs to use in a more ready out of the box format. Now Apex has announced the hire of Morningstar’s former chief product officer, Tricia Rothschild, as its new president, along with former Fidelity national sales SVP Tom Valverde as Apex’s new head of advisory, in what appears to be even more of a direct strategic focus on the independent RIA channel, leveraging Rothchild’s experience in building product for advisers and Valverde’s experience selling into the RIA channel. Ultimately, though, the challenge for Apex remains how it can effectively differentiate itself in a crowded and increasingly commoditized RIA custody business, where it doesn’t have the scale of Schwab, Fidelity or Pershing, and its biggest differentiator is the flexibility of technology APIs that the average RIA doesn’t have the means or capabilities to effectively leverage. At the least, Apex can highlight that it doesn’t have a retail business that effectively competes with its own RIAs – as is the case with Schwabitrade and Fidelity – although Apex still powers many of the leading robo-adviser competitors to independent RIAs (e.g., Betterment), and the sheer growth of Schwab, Fidelity and TD Ameritrade over the past decade suggests that in the end advisory firms are willing to trade off the implied channel conflict with the fact that those firms gain economies of scale to increase services and lower costs to advisers in the process. Still, though, with the custody business facing its own revenue challenges, as ZeroCom eliminated trading commissions just as the pandemic cut interest rates (and net interest income) drastically, the big question now is whether RIA custodians will start to charge basis points or other custody fees to the RIAs they serve. And in the end, the most straightforward way to charge basis points for custody is to build enough technology capabilities to replace other components of the adviser tech stack – effectively turning the custody business into a technology platform with custody as a loss leader – for which Apex and its tech-forward approach may be best positioned to compete. At least, if Rothschild can figure out exactly what technology product Apex should build that advisers will actually be willing to pay basis points for.

Is Vanguard competing for RIA custody with new digital advice robo tools for advisers? For most of their modern history, asset managers reached most financial advisers and their clients through mutual funds that advisers bought for their clients. Initially, mutual fund business was handled directly, but as advisers began to develop more holistic portfolios and shifted to fee-based models that might hold a wider range of mutual funds and charge a single advisory fee (instead of just receiving trails directly from mutual fund providers), mutual fund portfolios shifted from direct to brokerage-based. Brokerage platforms and RIA custodians were quite happy to facilitate the shift, since they got a piece of the action by serving as the transfer agent and earning their sub-TA fees. However, the shift from financial advisers as mutual fund salespeople to RIA fiduciaries who represent (and gatekeep for) their clients has led to another shift, where advisers can look good in front of their clients by saving them on portfolio costs, which is leading advisers to increasingly use technology to self-manage portfolios, select their own low-cost funds to build client portfolios and disintermediate mutual fund managers (and their mutual fund expense layer) in the process. The significance of this shift, from the perspective of brokerage firms and RIA custodians, is that advisers are increasingly incentivized to purchase ETFs over mutual funds, in part because ETFs don’t have the additional cost layer of sub-TA fees (which makes them even more likely to be the appealing, less expensive alternative for their clients), especially now that ETFs are free to trade (unlike mutual funds that often still have ticket charges) in the new ZeroCom world. This helps to explain why ETF providers, especially low-cost ETF providers like Vanguard and BlackRock, have increasingly been able to dominate the portfolio market share among RIAs. Yet the adviser shift from mutual funds to ETFs is also increasing tension between asset managers and RIA custodians, because the latter don’t profit from ETFs the way they did with mutual funds – due to the lack of the sub-TA fee (or any 12b-1 fees) – and therefore increasingly are going directly to asset managers and asking for payments (if not directly for shelf space platform access, then indirectly for key information like data about how advisers are using their funds, and/or for the ability to communicate with advisers through the RIA custodian). That appears to be leading some asset managers – most notably, Vanguard – to develop their own adviser solutions in an effort to either win business back from RIA custodians, or at least persuade them to relent on required platform payments (or risk having advisers shift entirely to work with the asset manager directly). Accordingly, on a recent webcast to the adviser community, Vanguard announced that it is nearing the rollout stage for a new digital advice software solution for financial advisers (having already been in live beta with two dozen advisers for the past six months), effectively threatening to turn advisers using Vanguard back into direct clients of the asset manager – akin to the fund business of the 1990s, albeit with a modern technology wrapper. Of course, the caveat is that the minimum standards of advisers for technology trading and portfolio management are very high – thus the challenge of so many B2B robo-platforms that have struggled to gain adoption – and it remains to be seen whether, or how broad, Vanguard’s offering will be (e.g., for only Vanguard ETFs or an open brokerage platform for advisers to use any ETFs, capable of allowing advisers to build their own portfolios or only choose from a preselected list of Vanguard model portfolios, etc.). Still, the underlying point remains: As the competitive pricing for brokerage pushes further and further toward zero, adviser platforms are increasingly pressured to find new sources of revenue, which is leading some to explore charging directly for custody and others like Schwab to find new sources of cross-subsidy revenue (e.g., affiliated bank cash sweeps), and may be creating a new era in which asset managers to develop their own direct-to-adviser solutions to win back the direct fund business of 20 years ago. Though whether Vanguard can pull it off – and whether any other asset manager has enough adviser adoption to even try – remains to be seen.

Envestnet enables fractional share management capabilities as direct indexing starts to gain mainstream steam. The concept of direct indexing – in which an investor doesn’t buy an index fund, but instead buys the underlying stocks that comprise the index – has been around since the early 1990s, when separate account managers like Parametric implemented the strategy on behalf of ultra-high-net-worth clients who wanted to take advantage of the tax loss harvesting opportunities of owning the individual stocks in the index (as the owner of an S&P 500 index fund can only harvest losses if the fund is down, but an investor owning the underlying 500 stocks of the S&P can harvest 122, 184, 217 or however many of the individual stocks that may be down for the year). The challenge of such direct indexing strategies, though, is that it requires a substantial portfolio to be able to buy that many individual stocks, each in the exact appropriate share quantities necessary to ensure the index itself is tightly replicated (without introducing tracking error), which is why, historically, direct indexing was only for ultra-HNW clientele. However, the 2010s witnessed the emergence of fractional shares: Certain investment platforms could facilitate investors owning fractions of an individual share that, in the past, were indivisible from whole units. And while the most common use of fractional shares was simply to allow new investors to start participating in the markets in small bits – e.g., a Robinhood or Acorns investor who wants to buy just $10 worth of Apple or Google – one of the indirect benefits of fractional shares was that it suddenly made direct indexing feasible for more mass affluent households who were only investing hundreds of thousands of dollars (and not millions) but could leverage fractional share investing to buy the exact 10.247 (or however many) shares needed to perfectly replicate the underlying holdings of an index fund. Accordingly, in late 2013, robo-adviser Wealthfront launched its Direct Indexing solution with what was originally a $500,000 and later $100,000 account minimum, effectively democratizing direct indexing for the mass affluent investor. However, the significance of direct indexing is not merely that it provides a slightly tax-savvier version of an index fund; it also potentially becomes a less costly alternative to a mutual fund or ETF, or at least a more customizable version of one (for those who want to express their factor, ESG, or other investment preferences directly in the underlying portfolio), which drastically expands the market potential, and has caused one major platform after another in recent years to launch fractional share capabilities and build out the potential for direct indexing. The appeal of direct indexing for technology providers, in particular, is that executing direct indexing both requires technology (to facilitate the large number of trades and individual shareholdings in the right allocations), and also creates the potential for technology providers to earn basis points by operating as asset managers (as even if the index providers set the index allocations, the direct-indexing technology provider has the opportunity to earn basis points to actually manage the implementation of the direct indexing solution). Accordingly, it is perhaps not surprising that Envestnet – the mother of all platform TAMPs – announced this month that it, too, is working on the capability to implement fractional share trading to expand the reach of direct indexing. In fact, the company noted in its Q2 earnings that demand for its existing (HNW) direct indexing strategies was up a whopping 23%, allowing the company to grow revenue by 5% in the quarter despite the pandemic sell-off. With fractional share capabilities, Envestnet hopes to further expand the reach of direct indexing to the average adviser’s mass affluent clients. That makes sense for Envestnet, which already operates one of the largest marketplaces of third-party managers, leaving the company well-positioned not just to facilitate direct indexing of index funds, but to facilitate direct indexing of any and every asset manager’s strategies (which Envestnet can execute in a centralized manner far more easily than each asset manager doing it themselves), and earning Envestnet its platform TAMP fee in the form of a direct indexing implementation fee (while disintermediating traditional asset managers’ mutual funds and ETFs in the process). The irony, of course, is that Envestnet is arguably more than six years late to the game of expanding direct indexing to the masses. Yet in the end, as Wealthfront demonstrated with its own lackluster success in growing direct indexing adoption, it turns out that the complexity of direct indexing may make it uniquely well suited as a solution that advisers bring to their clients to differentiate their own investment implementation process.

Xtiva raises $10 million from Recurring Capital Partners to accelerate growth of SPM platform. Adviser compensation systems have never gotten the same attention as adviser-facing tools like CRM or financial planning or home office platforms like portfolio management or billing. But compensation software (also referred to as sales performance management) is a critical component of a broker-dealer’s technology infrastructure to facilitate the payment of commissions (from dozens or hundreds of different carriers, to hundreds or thousands of different brokers). And as many broker-dealers struggle to remain relevant by reinventing their business (and revenue) models altogether, these systems are being leaned on not only to calculate compensation accurately and across an increasingly wide domain of commission- and fee-based offerings, but also to provide robust analytics and data management that can be leveraged to improve recruitment, retention and performance, and drive incentive management across different product lines. Xtiva has been among the top vendors in the space, which includes Anaplan, SAP CallidusCloud (acquired in 2018), and Broadridge Advisor Compensation Solutions (also acquired in 2018). But it doesn’t seem to be resting on its laurels, as Xtiva recently raised a $10 million investment from Texas-based Recurring Capital Partners. Two-thirds of the funds will go toward enhancing the pace of its product road map, including features to streamline OSJ operations, analytics that improve decisions on revenue and cost allocations, and organizing business intelligence. The remaining third will be used to beef up sales and marketing. The funding couldn’t come at a better time for Xtiva, as the level of complexity and diversity of the market has been growing steadily. IBDs (and now increasingly, RIA aggregators) have complex sets of needs to support different compensation models and multicustodial arrangements. In this context, it is not surprising that Xtiva also announced a new partnership with Salesforce, with Xtiva’s software now able to read and write core Salesforce objects, enabling out-of-the-box support for sending data to centralized management dashboards. Given that larger enterprise wealth management firms so often design their architecture with Salesforce as a middle layer, Salesforce support is often one of the first things they check when evaluating new technology. From the broader industry perspective, surveys have shown a fairly wide range for adviser compensation across wirehouses, national and regional broker-dealers, all of which seem to be trading a core group of hybrid advisers back and forth between them. These advisers are often swayed by firms that stay ahead of the technology curve, both in the front and middle office. Many of the larger firms are building out their own data lakes that ingest information from external systems to provide a consolidated view across the enterprise, and Xtiva needs to match the demands of competing technology offerings to support expanding its client base, which, ironically, is taking a renewed relative focus in the U.S. over other countries because big data analysis and business intelligence tools have become increasingly difficult to deploy elsewhere due to rising regulatory and data privacy issues in the EU and APAC. Fortunately for Xtiva, the number of sales management solutions customized for the advisory space remains limited. Still, though, the pressure will be on to deploy its newfound capital and actually accelerate its growth, as the downside of Xtiva’s large enterprise marketplace is a longer sales cycle, combined with a complex conversion process that gets further multiplied for larger firms that are running multiple compensation platforms as the result of mergers, often with heavy technical debt that was never consolidated (and the temptation for broker-dealer executives to continue to kick the can down the road on replacing their legacy adviser compensation systems and choosing to trade higher operations costs now to delay needed software upgrade expenses into the future). For most independent advisory firms, the scope of Xtiva’s solutions is most likely beyond their needs. But as more and more RIAs and RIA aggregators pass the $10 billion AUM mark, and as broker-dealers shift from a product-centric to an advice-centric focus and continue to consolidate, Xtiva appears to be positioning itself to ride the wave of an in-demand category of enterprise software for financial advisory firms.

InvestCloud launches end-to-end wealth management platform to compete for large-scale financial services enterprises. There is no shortage of software available for RIAs and broker-dealers to choose from when it comes to adviser technology platforms, from all-in-one solutions to best of breed combinations of stand-alone applications, to combinations of the two; the choices are seemingly endless. A new option was recently announced by West Hollywood-based InvestCloud, which is combining a number of formerly stand-alone modules into an end-to-end platform that can be configured to support either asset management or wealth management firms. InvestCloud has been adding to its portfolio of technology solutions since the company was founded in 2010. Its first product offerings were lightweight components that could readily be incorporated by other vendors into their own software, and were primarily deployed through a provider of client portal technology for asset managers called LightPort, which merged with InvestCloud in 2013. At the time of the merger, LightPort had over 700 clients, which is approximately the number that InvestCloud still has seven years later. Which means the LightPort merger made InvestCloud one of the largest providers of clients portals and dashboards, but the company has struggled to grow market share since and thus has been working hard to expand its capabilities toward the recently realized goal of an end-to-end wealth management platform dubbed InvestCloud White (where “White” is simply in keeping with its branding of different module combinations using primary color names). Its biggest client name is JP Morgan Asset Management, which not only decided to use the InvestCloud technology to build its digital investor tools, but also took an equity stake in the firm. Yet while InvestCloud has signed some small broker-dealers and investment managers to use parts of its broader platform, it is still working on breaking into the top tier of wealth management firms to deploy its full-stack portfolio management system. Still, InvestCloud has raised $54M in funding, primarily from FTV Capital and Kern Whelan Capital, and already spent $20 million of this to purchase London-based Babel Systems in 2017, which provided InvestCloud with portfolio accounting, rebalancing and trading engines. Some critics noted that at the time that the CEO of Babel System was Steve Wise, the brother of InvestCloud’s CEO John Wise. Nonetheless, the Babel purchase gave InvestCloud an international presence, with clients in the UK, Europe and APAC, along with multicurrency capabilities. However, while those international capabilities are very complex to build, they are not as highly valued by most US wealth management firms. Nonetheless, InvestCloud has fully joined the race to build a platform that can be everything to all advisory firm clients, aiming to compete with the other full-stack vendors such as Envestnet, Orion and Vestmark (although InvestCloud is probably more aligned with firms like Advisor360, Tegra118 and Charles River Development since it is a technology-only vendor with no plans to launch a TAMP offering). The challenge, however, is that the rising demand from financial advisers for better and more natively integrated technology is driving a number of these software providers to build increasingly comprehensive solutions, aiming to compete directly with the often proprietary platforms of today’s largest broker-dealers and custodians. Accordingly, InvestCloud would be well-positioned if the market shifts from monolithic all-in-one platforms to best-of-breed integrated modules that can be accessed similarly to apps from an App Store like Salesforce App Exchange, building on its success with portals, digital advice and mobile, as these channels become a higher priority for wealth management firms that have mostly ignored them until the pandemic shifted all digital interactions into high gear. Still, it remains to be seen whether InvestCloud can land a big deal with one of the top 50 broker-dealers or top 100 RIAs, given the immensely complex sales cycle and transition effort it details, and the challenges of differentiating among similarly full-featured competitors. We will be keeping our eye on the firm.

Will new accredited investor rules expand adviser crowdfunding for AdviserTech? Building new technology for financial advisers takes capital — far more than it takes to build an advisory firm itself — because a financial advice business is a service business, where the adviser can start immediately offering advice to the first client they meet, while an AdviserTech solution requires the entire software to be built before it can be used at all, which means hiring a product manager and one or several developers for what might be six to 12 months or more of building before the first paying adviser can sign up. The good news in the world of financial advisers is that the advisory business itself is a rather lucrative business, to the point that many financial advisers end up growing their businesses to the point that they can self-fund the development of their own technology in the first place, and then later recover their costs by selling the software to other advisory firms. In fact, these homegrown AdviserTech solutions – where the adviser has a business problem, builds technology to solve the problem, sells technology to other advisers who have a similar problem, and now also owns and runs a technology company – comprise a significant portion of the leading AdviserTech solutions, from Junxure to Redtail in the CRM category, Orion to Tamarac in portfolio management, iRebal, TradeWarrior and RedBlack for stand-alone rebalancing, RiskPro and Tolerisk for risk tolerance, Hyperchat Social for social media, Benjamin from Wela for client communication, and our own AdvicePay for advisory fee billing. Yet in reality, only a very small subset of advisers run firms that are large enough, and with enough free cash flow, to self-fund the entire build of an AdviserTech solution. And unfortunately, raising outside capital from traditional sources – e.g., venture capital firms – is difficult for AdviserTech solutions, given both the highly fractured adviser marketplace (which makes it very difficult to grow rapidly enough to meet venture capital investor demands) and what is still a limited total addressable market of financial advisers (where it’s certainly possible to build successful businesses worth tens or even hundreds of millions, but difficult to build the unicorn that VC firms want with a $1 billion-plus market opportunity). The alternative for startup investors is to raise equity capital one person at a time. But soliciting such investments into what is technically a private unregistered security requires working with only accredited investors, which makes it difficult for advisers to find enough prospective people to invest (especially given the prospective conflicts of interest for soliciting and rules against commingling assets with advisers’ own clients). But this month, the SEC updated its accredited investor requirements, which will still include a requirement of $200,000 of income (or $300,000 for couples) over the past two years or a net worth of $1 million (outside the primary residence), but will now also have an alternative path to qualifying as an accredited investor based on certain professional designations or credentials, including those with the Series 7 or Series 65 (or Series 82) licenses. This means the bulk of financial advisers themselves will now qualify as accredited investors, providing new AdviserTech startups with a unique pathway to be able to crowdfund from the financial adviser community itself – raising capital from the very users who would buy the software. In point of fact, the model for this approach has already been set once – as AdvicePay in 2018 crowdfunded its seed capital round directly from the adviser community (albeit from advisers who specifically met the old accredited investor definition). But with the new accredited investor rules now making virtually all financial advisers accredited simply by virtue of their Series 7 or Series 65 licenses, the pool for potential AdviserTech funding from financial advisers themselves just got a whole lot deeper!

In the meantime, we’ve updated the latest version of our Financial Adviser FinTech Solutions Map with several new companies, including highlights of the Category Newcomers in each area to highlight new fintech innovation!

So what do you think? Will Schwab’s decision to offer financial plans for free to self-directed consumers pose a threat to traditional advisers? Will Riskalyze’s new tax alpha capabilities allow it to effectively differentiate in a crowded marketplace for portfolio management? Can Envestnet scale a direct indexing solution across its entire range of TAMP strategies? And will financial advisers really become more active AdviserTech investors now that their Series 7 and 65 licenses alone make them accredited investors? Please share your thoughts in the comments below!

Special thanks to Kyle Van Pelt, who wrote the sections “Will Fidelity’s Bond Beacon satisfy advisers’ newfound desire to trade individual bonds?” and “Is the AdviserTech pendulum swinging back toward proprietary as Merrill Lynch builds its own FP software?” You can connect with Kyle via LinkedIn or follow him on Twitter at @KyleVanPelt.

Michael Kitces is head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’s Eye View. You can follow him on Twitter at @MichaelKitces.

Disclosure: Michael Kitces is a co-founder of AdvicePay and is on the advisory board of Timeline, both of which were mentioned in this article.

Craig Iskowitz is CEO and founder of Ezra Group, a management consulting firm providing advice to the financial services industry on marketing and technology strategy. You can follow him on Twitter @craigiskowitz

Former Northwestern Mutual advisors join firm for independence.

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Canada, China among nations to react to president-elect's comments.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound