An influential consulting firm has warned money managers that wirehouses, long the chief target of their marketing outreach, will deliver a negligible share of new money into products like mutual funds.

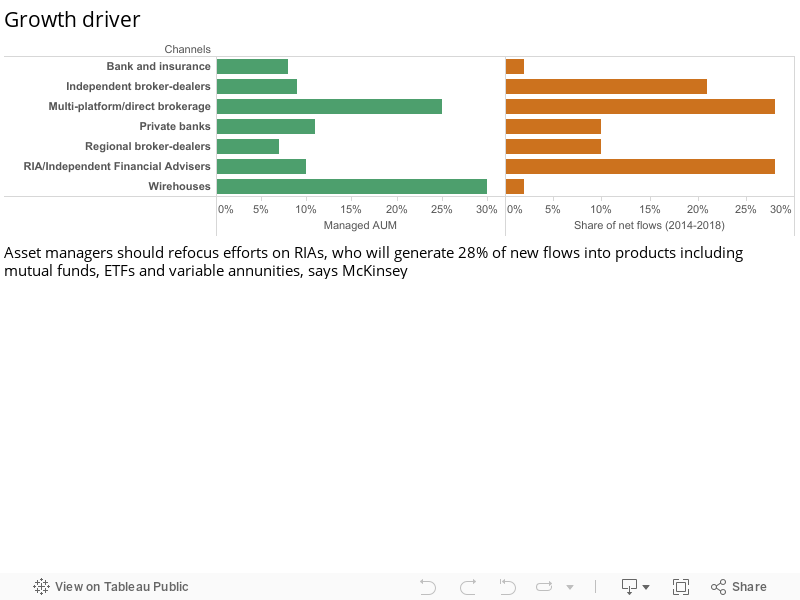

McKinsey & Co. said Wednesday it expects wirehouses — four firms that control nearly a third of managed retail assets in the U.S. — to contribute just 2% of the growth in products like managed accounts, mutual funds and variable annuities over the next four years.

Over the same period, the direct-to-investor and independent registered investment adviser channels will each contribute 28% to the new money, or net new flows, to the products, according to the New York-based consultancy. Independent broker-dealers will contribute 21% of growth, while private banks and regional broker-dealers are each projected to represent 10%.

“Asset managers are underweighting the most important channels and must rethink coverage to maximize their bang for the buck,” the report said. “Moving forward, McKinsey expects wirehouses to capture the lowest share of net new flows. As they increasingly struggle to acquire new customers, wirehouses must also contend with the growing number of advisers who are moving to independent broker-dealers or striking out on their own, lured by more generous revenue sharing and compensation.”

The consulting firm's new estimate adds kindling to a long-running debate about the vitality of the business of the firms — Morgan Stanley, Bank of America Corp., UBS AG and Wells Fargo & Co. — that employ the world's largest group of high-drawing brokers and financial advisers but have lost market share in recent years to independent competitors. Those firms have said consistently that attrition remains low and revenue high.

But the report also delivered advice to the equally thundering herd of money managers — 2,000 external wholesalers for the top 40 fund managers, according to McKinsey — that hope to court those advisers by earning a privileged spot on proprietary investment platforms like those operated by wirehouses.

The consultancy argues that investment firms have to think as much about the growth potential of platforms and products as they do about investment performance.

“Firms concentrating on investment performance and not enough on market positioning and distribution excellence tend to attract strong net flows over the short run, but are the most likely to fall out of the leadership group over the longer term,” the report said.

The consultancy did not name specific firms, but singled out American Funds, Dodge & Cox, ProFunds and John Hancock Investments as firms that fell out of the top 10 in new flows to funds in the five years ending in 2013.

Over the next several years, nearly all of the flows into funds will be into alternative investments, multi-asset class products, index-based passive investments and specialized active management strategies like international equities and unconstrained bond funds, McKinsey said. The growth of those products will continue to come at the expense of traditional core products, like actively managed U.S. stock funds, according to the consultancy.

In addition to targeting product development, the firm said asset managers need to better use data to serve advisers and investors.

“In an era when digital marketers can tailor online ads to consumers' demographic and behavioral patterns and pharmaceutical companies can track prescriptions by physicians down to the pill, asset managers are woefully behind the curve in using data and advanced analytics,” the report said.

“The idea of covering 300,000 advisers in the same way is over,” said Scott B. David, who leads retail distribution for T. Rowe Price Group Inc., the sixth-largest U.S. mutual fund house, in a June 16 interview with InvestmentNews.“We are starting to get better data to know who does portfolio management.”

For several years, Leech allegedly favored some clients in trade allocations, at the cost of others, amounting to $600 million, according to the Department of Justice.