Among Social Security’s many beneficiaries are spouses. These include those who have never worked outside the home and haven’t contributed to the program. In some situations, even ex-spouses may be eligible to receive retirement benefits.

In this client education guide, InvestmentNews gives you a walkthrough of the rules surrounding Social Security benefits for a nonworking spouse. We will explain the eligibility requirements and how payouts are calculated. We will also explore ways on how stay-at-home partners can maximize their spousal benefits.

If you have spent most of your life as a homemaker and are wondering if you’re eligible for retirement benefits under your spouse or ex-spouse’s Social Security, this article is for you. If you’re a financial adviser, you can share this guide with your clients who may have questions regarding Social Security spousal benefits.

Social Security is designed to provide qualified workers with a monthly income upon retirement. This benefit extends to their nonworking spouses eligible to receive payouts based on their earnings record. Spouses can claim the benefits only when their working partners have also filed for retirement.

If you’re a stay-at-home spouse, you can receive a maximum payout equivalent to 50% of your working partner’s retirement benefits. This depends on when you decide to claim the benefits. You can get the maximum amount if you wait until full retirement age (FRA) before claiming Social Security benefits. This is regardless of whether your spouse delays receiving payouts past full retirement age to increase their benefits.

There are drawbacks, however, to claiming retirement benefits too soon. Social Security benefits for a nonworking spouse are permanently reduced by 25/36 of 1% (or almost 0.70%) for each month before reaching FRA. This reduction applies if you’re reaching full retirement age within 36 months.

If you retire more than 36 months before FRA, the Social Security Administration (SSA) will slash 5/12 of 1% (about 0.42%) for the additional months.

This means that if you file upon reaching 62 years old – the earliest possible – you can end up receiving payouts just 32.5% of your working spouse’s retirement benefits.

The graph below shows how much Social Security benefits nonworking spouses can receive for each year they delay claiming retirement benefits.

There are exceptions to this rule. If you’re caring for a “qualifying child,” the SSA will not reduce your retirement benefits even if you file before reaching FRA. The department defines a qualifying dependent as those who are under 16 years old or receiving Social Security disability benefits. You and your spouse must also be the child’s biological parents.

Learn more about how Social Security benefits work in this guide.

Generally, you’re eligible to receive Social Security benefits for a nonworking spouse if:

Nonworking spouses caring for a qualifying child are often eligible to receive benefits before reaching 62 years old. In this scenario, the marriage requirement may also be waived.

But what if you’re eligible for your own Social Security benefits? You may still qualify for an additional payout if your spousal benefit amount is higher than your personal benefit. If this is the case, the SSA sends you an additional amount, so that your total benefit equals the higher amount.

A different set of eligibility requirements, however, applies if you’re divorced. Even if your marriage ended a long time ago, you can still claim Social Security spousal benefits without notifying your ex-spouse if:

Social Security benefits for a nonworking spouse aren’t affected even if the working spouse remarries. Similarly, claiming spousal benefits doesn’t have an impact on your ex-spouse’s retirement benefits. But if you decide to remarry, you can’t collect spousal benefit on your former spouse's record. The SSA also requires you to inform them of the marriage to avoid overpayment.

If you’re caring for a qualifying child, however, the same rules apply as if you’re still married.

Widows and widowers, meanwhile, can claim Social Security survivor benefits even if their spouse or former spouse dies before reaching full retirement age. They may receive up to 100% of the retirement benefits the deceased is eligible for.

You can access the SSA’s spousal benefits calculator on the agency’s website. This online tool can provide you with an estimate of how much Social Security spousal benefits you’re entitled to.

If you prefer a more hands-on approach, you can do the calculations yourself by following these steps:

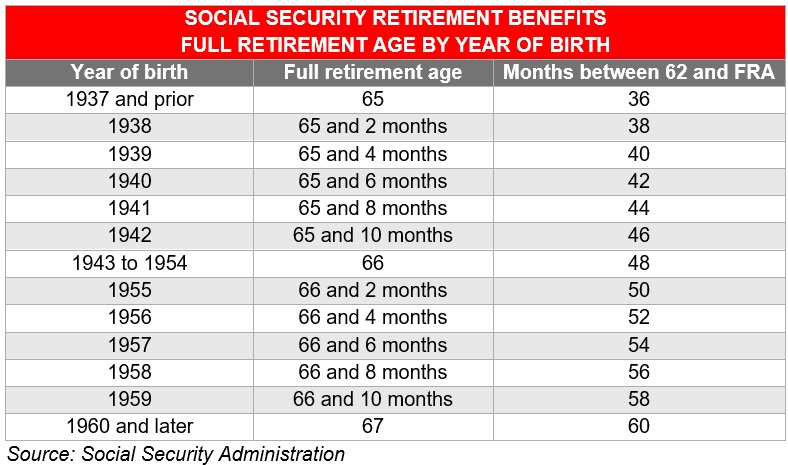

Social Security benefits for a nonworking spouse are based on the retirement benefits of the working partner at full retirement age. This is also what the SSA refers to as the primary insurance amount (PIA). FRA is between 65 and 67 years old, depending on the year a person was born.

Here’s a quick look at the FRAs – also called normal retirement age (NRA) – per year of birth, according to the SSA’s website.

SSA’s rules state that current and former spouses are entitled to Social Security spousal benefits up to 50% of the working partner’s retirement benefits if they wait until FRA.

So, if your spouse’s personal benefit is at $1,800 monthly, you can receive spousal benefits of $900 ($1,800 ÷ 2 = $900) if you don’t file before FRA.

The SSA reduces your spousal benefits if you don’t wait until full retirement age. For the first 36 months, the department will permanently deduct 0.69% from your payouts for each month before your FRA. For every month that exceeds this period, the SSA will subtract 0.42% from your spousal benefits.

So, if you claim at 62, you can end up getting only 32.5% of the spousal benefit you’re entitled to compared to what you're supposed to be receiving by FRA.

If you were set to receive $900 monthly in spousal benefits at FRA but you claim at 62, you can only collect $585.

$1,800 x 50% = $900 (spousal benefits if claiming on FRA)

$1,800 x 32.5% = $585 (spousal benefits if claiming at 62 years)

Unlike personal retirement benefits, however, spousal benefits don’t keep increasing past full retirement age.

If you qualify for Social Security retirement benefits, you may be eligible for a higher payout if your spousal benefit amount is higher than your personal benefit. As a rule, you will receive whichever is the higher amount.

Let’s say you’re eligible for a monthly personal benefit of $750 and a spousal benefit of $900. The SSA will send the higher amount, not the combined amount. It’s like adding the difference to your personal benefit payouts.

There are three ways you can file for personal and spousal Social Security benefits:

You must be within three months of your 62nd birthday to apply. If you’re applying online, be sure to tick both the retirement and family benefits boxes.

If you apply for personal retirement benefits, the SSA automatically considers whether you’re also eligible for spousal benefits. It’s important that you and your spouse factor in the timing of the application as it will trigger the personal and spousal benefits at the same time. If you qualify for both, the department sends you the larger of the two benefits.

For Social Security benefits for a nonworking spouse, you may need to provide a copy of your marriage certificate or divorce decree to be eligible. The SSA instructs applicants, however, not to send any documents unless requested.

Previously, couples could claim Social Security spousal benefits while allowing retirement benefits to grow by using the “file-and-suspend” strategy. Under this approach, the working spouse files for retirement benefits upon reaching FRA, then voluntarily suspends their retirement payouts. By doing so, the nonworking spouse continues to receive spousal benefits while the working spouse’s retirement benefits accrue.

The Bipartisan Budget Act of 2015, however, abolished this loophole. At present, when someone files for Social Security benefits, they are considered to be filing for all benefits they are entitled to receive. The SSA assumes that an applicant is filing for both retirement and spousal benefits and pays out the higher amount.

Because of this, the only way to maximize Social Security benefits for a nonworking spouse is for the working spouse to delay claiming retirement benefits until full retirement age.

No. Nonworking spouses can only claim Social Security benefits once their working spouses have claimed retirement benefits.

A nonworking spouse must be at least 62 years old to claim Social Security benefits. But there is an exception: if they have a qualifying child under their care, they can claim spousal benefits even before turning 62 years old. A qualifying dependent must be under 16 years old or receiving Social Security disability benefits.

In some cases, nonworking spouses may have previous work histories that make them eligible for their own retirement benefits. The amount they can collect depends on how much they earned, how long they worked, and when they claim Social Security. However, if their spousal benefits are higher than their retirement payouts, the SSA automatically sends them the higher amount. They can’t collect both benefits.

Visit our Retirement News Section to learn more about Social Security spousal benefits. Be sure to bookmark this page to access breaking news and the latest industry updates.

Relationships are key to our business but advisors are often slow to engage in specific activities designed to foster them.

Whichever path you go down, act now while you're still in control.

Pro-bitcoin professionals, however, say the cryptocurrency has ushered in change.

“LPL has evolved significantly over the last decade and still wants to scale up,” says one industry executive.

Survey findings from the Nationwide Retirement Institute offers pearls of planning wisdom from 60- to 65-year-olds, as well as insights into concerns.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound