IBM surprised the employee benefits world late last year when it disclosed that it would start a new pension program for workers – but the company has been following a widespread trend for the shuttered defined-benefit plan on its books, buying group annuity contracts that move liabilities to insurance companies.

Last month, it made the second of two such pension-risk transfers to Prudential, moving about $6 billion in pension obligations to the insurer, covering the retirement accounts of roughly 32,000 people. That followed a 2022 pension-risk transfer of $16 billion in liabilities for about 100,000 account owners and their beneficiaries.

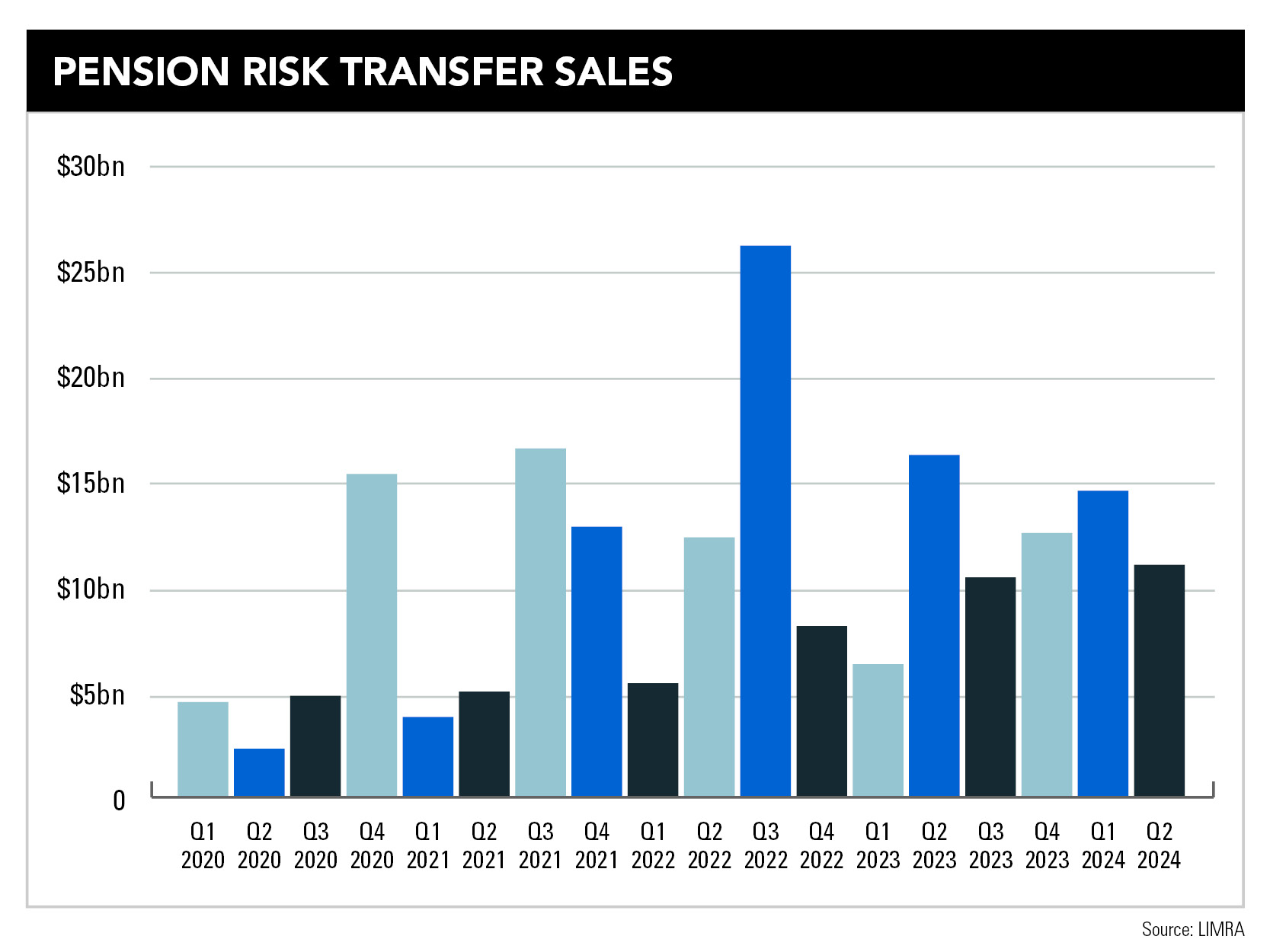

Such deals have become so common that it’s hard to keep up. During the first six months of 2024, there was a total of $26 billion in pension-risk transfer premium in the US, a 14 percent increase over figures seen in the first half of 2023, data from LIMRA show. Even as pension-risk transfer premiums were slightly down in the second quarter of 2024, those in the first quarter set a record at $14.6 billion. The most ever seen during a single quarter was in 2022, when the industry saw $26 billion in premiums, according to LIMRA.

While many major US companies have offloaded considerable amounts in pension obligations, the trend is starting to pick up more among smaller companies. Even as pension-risk transfers have existed for more than a decade, they’ve become more common in part as favorable interest rates have helped improve the funded statuses of their plans and pushed the costs of the transfers down.

“There has been a strong push to do pension-risk transfers because of the recent high rates,” said Tamiko Toland, owner of Toland Consulting and cofounder of IncomePath. Short-term interest rates are declining, but increases in long-term rates have helped favor pension-risk transfers, she said.

“The longer-term rates affect the pricing. I would imagine that even with [short-term] rates coming down, it encourages people to act.”

For pension plan sponsors that want to move their liabilities to insurers, price is always part of the equation, said Geoffrey Dietrich, executive vice president of Dietrich & Associates, a firm that consults on and designs pension-risk transfers.

“Cost is always a driving factor,” Dietrich said. “A lot of times it’s very close from a pricing standpoint. I don’t want to say that the lowest-cost provider always wins.”

That is largely due to plan sponsors having to assess the safety of the insurers they choose, as outlined by a bulletin the Department of Labor issued in 1995, following the collapse of Executive Life Insurance Company. That covers an insurer’s investment portfolios, size, capital and surplus, lines of business, and other factors.

“We won’t bring a company to the table that we don’t think is safe,” Dietrich said about annuity provider selection.

Prior to the early 2000s, pension transfers were mostly done when businesses terminated their pensions, rather than strategically moving some or all of their obligations to insurers. Pension-risk transfers, the kind that have become common today, started after General Motors made a $25 billion transfer, Dietrich noted.

Dietrich facilitated 73 pension-risk transfers last year, and anticipates more – about 85 percent of that company’s business covers such transfers. That firm works with smaller companies, rather than “upmarket” corporations that have cut deals of at least half a billion dollars with big insurers like Prudential, MetLife, and Athene, Dietrich said.

Closing defined-benefit plans is never popular with workers. Even as defined contribution plans like 401(k)s have become normal, unions have fought to retain or bring back traditional pensions. That was among demands made last year by the United Auto Workers in their strike with the big US carmakers, and the loss of Boeing’s pension a decade ago contributed to the strike currently on at that company.

When pension obligations are transferred to insurers, the workers, retirees, and beneficiaries lose the protection of the Pension Benefit Guaranty Corporation, as the group annuities are covered by state-level regulations.

And as pension-risk transfers have ramped up, so has the litigation against plan sponsors that opted for them. This year there have been several lawsuits filed against companies, most, if not all of which selected one insurance company – Athene Annuity & Life Co. – which has been the leader in sales for such transfers. The companies sued include GE, Lockheed Martin, AT&T, and Alcoa. State Street Global Advisors, which advises on pension-risk transfers, is also a defendant in the AT&T case. However, Athene is not named in any of the suits.

Plaintiffs in the cases have pointed to low surplus-to-liabilities ratios reported by Athene, relative to significantly higher ratios by other major insurers. However, Athene has surplus assets with its Bermuda affiliate, and those are not reported by its Iowa-registered office.

The lawsuits are an “entirely baseless attempt by class-action attorneys to enrich themselves at the expense of retirees,” an Athene spokesperson said in an email.

“Every pension group annuity participant whose benefits have been guaranteed by Athene has received and will receive their promised benefits in full. In each pension group annuity transaction for which Athene has been selected, there has been a robust review process carried out by a fiduciary and their independent advisers, who are experts at assessing insurer safety.”

The firm said that it is “properly reserved” and cited high credit ratings, including a recent upgrade to A+ by AM Best.

The lawsuits have drawn attention to pension-risk transfers, but they have not stopped employers from considering them, Dietrich said.

“The lawsuits out there in my opinion are without basis because there has been no harm. There’s been no loss. It’s that these guys don’t look like the other guys,” he said, of Athene’s structure and offshore affiliates. “We haven’t seen any impact on interest in doing this.”

While pension participants do lose PBGC protection, state oversight leaves insurers “heavily scrutinized,” he said.

And of interest that could continue in the business, there are roughly 20,000 single-employer defined-benefit plans in the US, not including union Taft-Hartley plans, non-ERISA church plans, and public plans, he said.

“There are still a lot of pension plans out there.”

Former Northwestern Mutual advisors join firm for independence.

Executives from LPL Financial, Cresset Partners hired for key roles.

Geopolitical tension has been managed well by the markets.

December cut is still a possiblity.

Canada, China among nations to react to president-elect's comments.

Streamline your outreach with Aidentified's AI-driven solutions

This season’s market volatility: Positioning for rate relief, income growth and the AI rebound